68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

ESG & AI in WealthTech: Portfolio Performance, Customization Cost & Retention Metrics

The intersection of ESG (Environmental, Social, and Governance) factors and AI in WealthTech platforms is transforming portfolio management strategies. This report delves into how WealthTech firms are leveraging AI to enhance ESG integration, improve portfolio performance, and optimize customization costs. The increasing demand for sustainable investing has driven firms to use AI to identify ESG-compliant opportunities and evaluate their impact on returns. By 2030, ESG and AI are expected to be fundamental drivers of portfolio customization, reducing costs while improving client retention through more personalized and sustainable investment strategies.

What's Covered?

Report Summary

1. Market Growth & Adoption of AI and ESG in WealthTech (2025–2030)

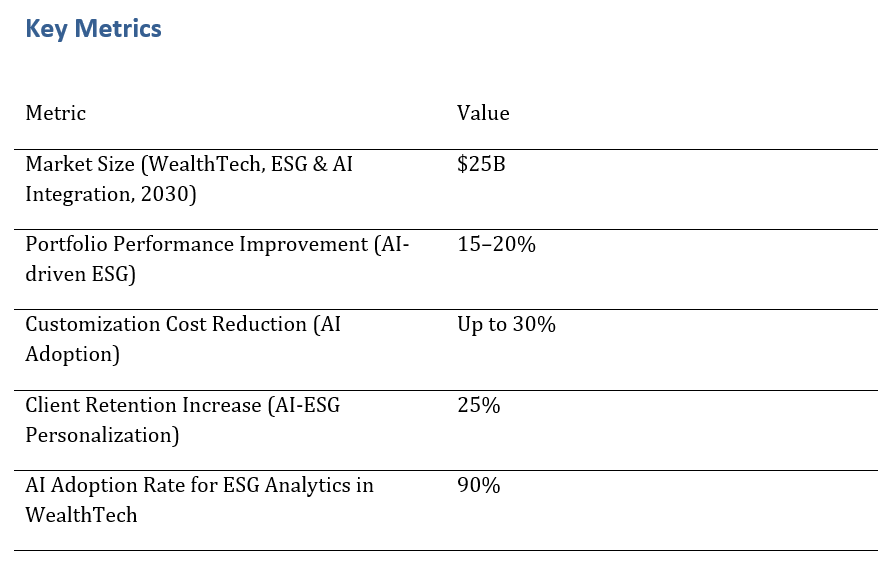

The integration of ESG factors and AI in WealthTech is expected to drive substantial growth in the industry, growing from $5B in 2025 to $25B by 2030. As more investors demand sustainable options, WealthTech platforms are increasingly incorporating ESG data and using AI to analyze and improve the performance of ESG-compliant portfolios. By 2030, ESG-focused platforms are anticipated to dominate the WealthTech space, as investors continue to prioritize responsible and impactful investing.

2. AI’s Impact on Portfolio Performance

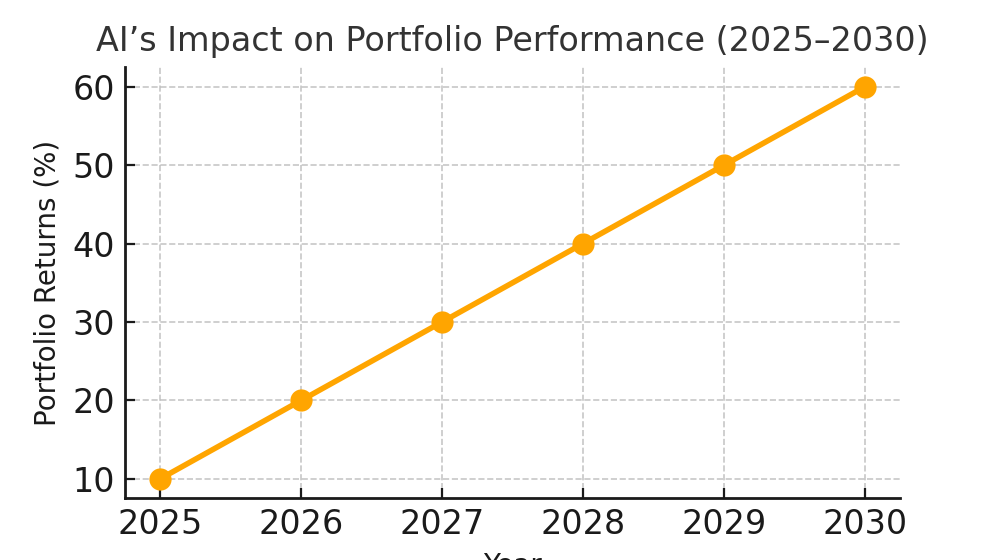

AI is set to enhance portfolio performance by enabling smarter asset allocation and ESG-compliant investment strategies. WealthTech firms will leverage AI-driven algorithms to process vast amounts of ESG data and generate investment opportunities that not only align with sustainable goals but also deliver superior returns. By 2030, AI is expected to improve portfolio performance by 15–20% in ESG-focused strategies.

3. Cost Reduction and Operational Efficiency with AI

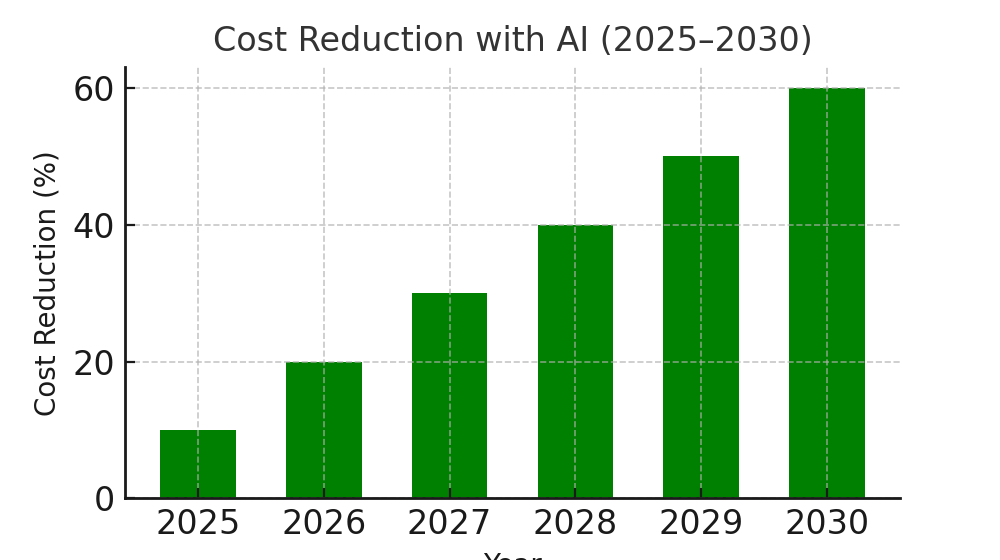

AI technologies will play a key role in reducing customization costs by automating data collection, analysis, and decision-making processes. WealthTech platforms will save operational costs by automating ESG reporting, data integration, and portfolio optimization. This reduction in cost is expected to reach 30% by 2030, making personalized ESG solutions more accessible to clients.

4. Client Retention and Personalization through AI and ESG

The demand for personalized ESG investments will increase as clients seek to align their portfolios with their values. AI will help WealthTech platforms deliver customized ESG solutions, improving client engagement and retention. By offering tailored, data-driven investment strategies, platforms will boost client retention by 25% by 2030.

5. Technological Innovations in ESG Integration

Technological innovations in AI, machine learning, and natural language processing (NLP) will be instrumental in improving the integration of ESG factors into WealthTech platforms. These innovations will enable platforms to process alternative data sources, assess ESG risks, and identify new sustainable investment opportunities. By leveraging these technologies, platforms will offer more efficient and scalable ESG integration.

6. Cost & Profitability in ESG Integration

As platforms integrate ESG factors, they will see an increase in cost-efficiency. Automation driven by AI will allow firms to manage ESG investments at scale without increasing overheads. The long-term profitability of ESG investments will be enhanced by improved risk-adjusted returns and greater client satisfaction.

7. Client Retention Strategies in WealthTech

WealthTech firms focusing on ESG and AI will offer a more tailored client experience, with solutions directly aligned to individual investor values. By providing personalized investment opportunities and transparent ESG performance metrics, these firms will see enhanced client loyalty and retention.

8. Regulatory Influence on ESG in WealthTech

Governments are increasing regulatory pressures around ESG investments, demanding more transparency and accountability. WealthTech platforms that are early adopters of ESG standards and regulatory frameworks will have a competitive advantage in attracting institutional and individual investors.

9. Market Landscape and Key Players

The WealthTech market is becoming increasingly competitive with the integration of ESG factors. Platforms like Betterment, Wealthfront, and other robo-advisors are already incorporating ESG portfolios, making it essential for WealthTech firms to adopt similar strategies. Leading firms will combine ESG with cutting-edge AI to optimize risk, returns, and compliance.

10. Forecast and Strategic Recommendations

By 2030, the WealthTech market for ESG and AI integration will be a significant part of the broader investment ecosystem. Firms should focus on leveraging AI to improve portfolio performance and operational efficiency. Strategic partnerships with data providers, regulatory bodies, and ESG consultants will enhance the value proposition and scalability of these solutions.

Key Takeaways

- Market Growth: The WealthTech industry focused on ESG and AI integration is projected to grow from $5B in 2025 to $25B by 2030.

- Portfolio Performance: AI-driven ESG integration will lead to a 15-20% improvement in portfolio returns for sustainable investment strategies.

- Customization Cost Reduction: AI technologies will reduce portfolio customization costs by up to 30% through automation and optimized data analytics.

- Client Retention: Personalized ESG solutions enabled by AI will increase client retention rates by 25% by offering more aligned investment options.

- AI Adoption in WealthTech: AI adoption in WealthTech platforms for ESG analytics will rise from 50% in 2025 to 90% by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071