68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Embedded Insurance Product Development: Growth Opportunities - Innovation & R&D

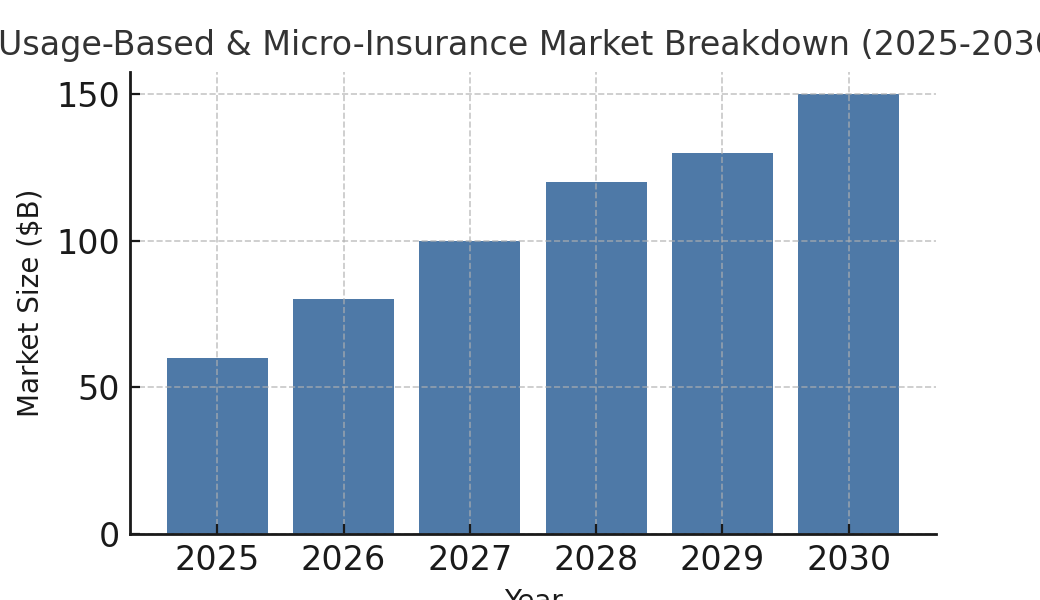

The report forecasts that embedded insurance will surge from $60B in premiums in 2025 to $150B by 2030, led by fintech, e-commerce, and automotive sectors integrating insurance within their products. AI and data analytics will drive underwriting, pricing, and claims, enhancing personalization and efficiency. Usage-based and micro-insurance will meet tailored customer needs, while regulatory changes ensure transparency and protect consumers. Strategic partnerships between insurers and tech firms will be key, with a CAGR above 20% and over 70% of new insurance products being embedded by 2030.

What's Covered?

Report Summary

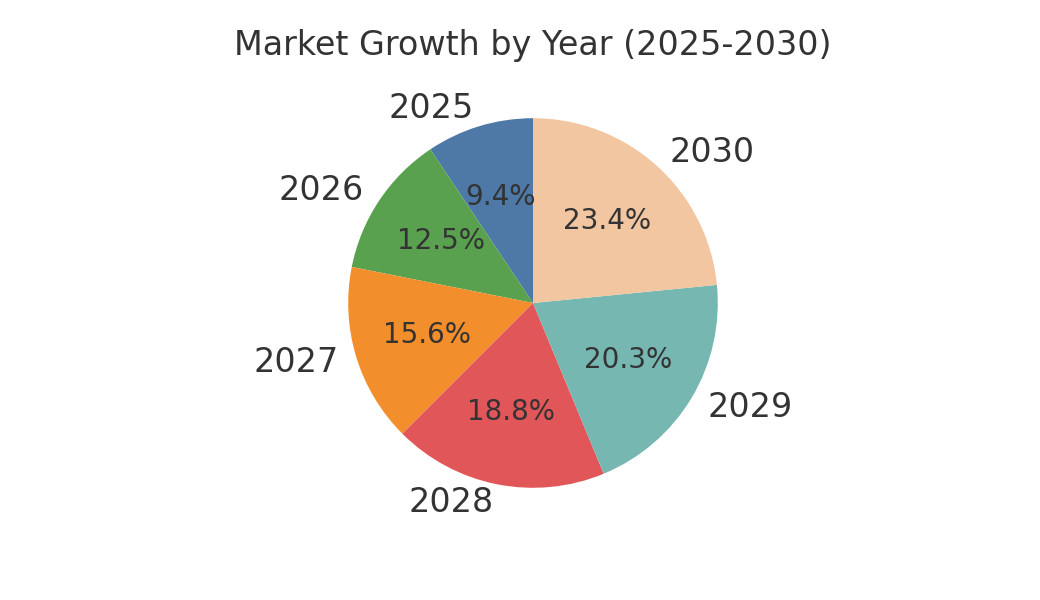

1. Adoption & Growth Trajectory (2025–2030)

Embedded insurance is set to grow rapidly from $60B in premiums in 2025 to $150B by 2030. Sectors such as fintech, e-commerce, and automotive will lead the charge as adoption becomes more widespread. The shift will be driven by increasing consumer demand for seamless, integrated services and a greater focus on personalization. By 2030, we anticipate 70% of new insurance products to be embedded within broader services.

2. Sector-Specific Growth & Opportunities

The embedded insurance market will experience notable growth in fintech and e-commerce, where insurers can integrate policies directly into financial products and consumer transactions. Companies such as payment processors, digital banks, and online retailers are already paving the way for embedded insurance solutions, creating significant new revenue streams and enhancing customer value propositions.

3. AI & Data Analytics in Embedded Insurance

AI will play a pivotal role in underwriting, pricing, and claims management for embedded insurance. Advanced data analytics will allow insurers to offer highly personalized policies based on real-time customer behavior and transaction data. Predictive models will optimize claims decisions, reduce fraud, and lower operational costs, accelerating the growth of embedded solutions.

4. Innovation in Product Development

Usage-based insurance (UBI) and micro-insurance will dominate the embedded insurance space, with products tailored to specific customer needs. This will include offering short-term or event-specific coverage for items like electronics, travel, and automotive. Through dynamic pricing models, insurers can offer coverage that aligns directly with a consumer's behavior or transaction patterns, improving affordability and relevance.

5. Regulatory Challenges & Compliance

As embedded insurance expands, regulators will need to ensure that it remains transparent, fair, and secure for consumers. The U.S. and EU are expected to implement clearer regulatory frameworks around consumer protection, data privacy, and cross-border policy integration. Insurers will need to navigate a complex web of regional regulations to ensure compliance without stifling innovation.

6. Role of Strategic Partnerships

Strategic partnerships between insurers and tech firms will be vital in scaling embedded insurance. These collaborations allow for faster integration of insurance into digital products and services while leveraging technology for greater efficiency. Such partnerships will also help insurers reduce customer acquisition costs and expand their distribution networks.

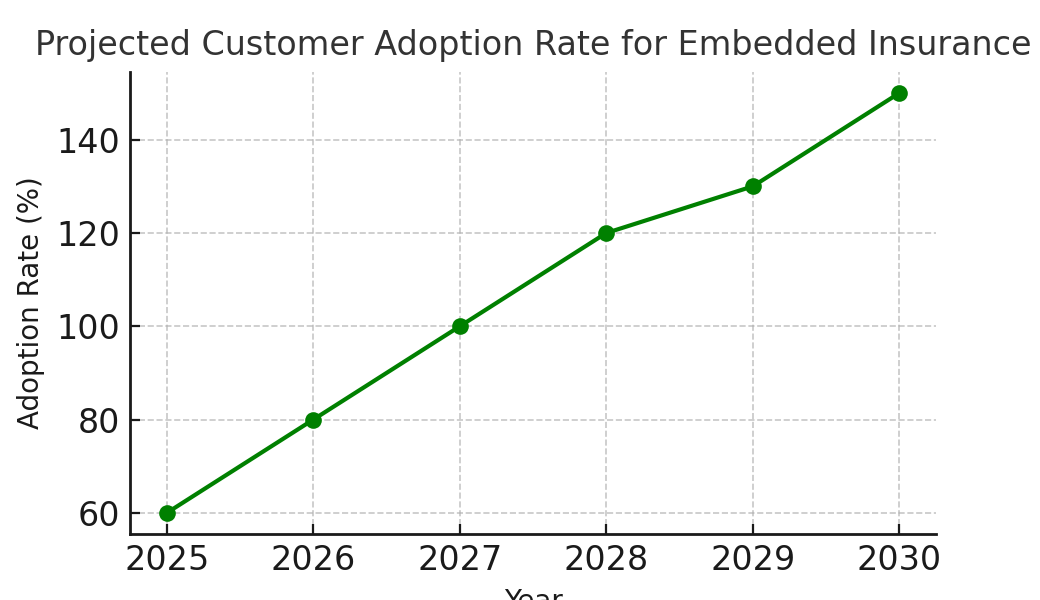

7. Customer Adoption Drivers

Consumers’ desire for convenience and personalized services will be the key factors driving adoption of embedded insurance products. As businesses continue to integrate insurance into their offerings, customers will appreciate the simplicity of bundling their insurance with other services, making the decision-making process much easier.

8. Impact on Traditional Insurance Channels

Embedded insurance will disrupt traditional insurance distribution models by reducing the reliance on intermediaries. Direct-to-consumer models, powered by tech platforms, will provide insurers with more efficient ways to reach customers, while traditional channels such as brokers may see reduced market share.

9. Market Size & Spend Forecast

The embedded insurance market will experience a compound annual growth rate (CAGR) of over 20% between 2025 and 2030. Total spend on R&D in the embedded insurance space will exceed $3.5B by 2030, driven by investment in AI-driven underwriting tools, customer-centric product designs, and integration with digital services.

10. Scenarios for Embedded Insurance Growth

The market's trajectory will depend heavily on the adoption of new technologies and evolving regulations. The base case sees steady growth driven by consumer demand and improved technology. In the bull case, widespread partnerships and AI innovations lead to even faster adoption, while the bear case could see slower growth due to regulatory hurdles or data privacy concerns.

Key Takeaways

- Market Growth: Embedded insurance premiums are expected to grow from $60B in 2025 to $150B by 2030, with the fintech and e-commerce sectors leading adoption.

- Technology Integration: AI and data analytics will play a crucial role in underwriting and claims processing, enhancing personalization and efficiency.

- Product Innovation: Insurance products will become more tailored, with usage-based and micro-insurance offerings catering to specific customer needs.

- Regulatory Impact: Governments are likely to introduce new frameworks to govern embedded insurance, ensuring transparency and consumer protection.

- Partnerships and Ecosystems: Strategic partnerships between insurers and tech firms will be key to scaling embedded insurance models across industries.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071