68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Edge AI in Real-Time Payments: Fraud Detection Latency, Processing Cost Reductions & Adoption Benchmarks

Edge AI technology is revolutionizing the real-time payments ecosystem by enhancing fraud detection, reducing latency, and driving significant cost reductions. As the financial industry continues to embrace digital payments, the integration of AI at the network edge ensures that payment transactions are processed more efficiently, securely, and in real-time. By 2025, the market for Edge AI in real-time payments in the USA and Europe is projected to reach **$7.4 billion**, growing at a **CAGR of 27%** from 2025 to 2030. This report explores the trends driving the adoption of Edge AI in real-time payments, with a focus on reducing fraud detection latency, cutting processing costs, and the benchmarks for widespread adoption. This report also delves into the impact of Edge AI on fraud prevention, customer experience, and operational efficiency in payment systems, highlighting the key market drivers and the competitive landscape for solution providers in the USA and Europe.

What's Covered?

Report Summary

Key Takeaways

- The market for Edge AI in real-time payments is expected to reach $7.4 billion by 2025, growing at a CAGR of 27% from 2025 to 2030, driven by increasing adoption in Europe and the USA.

- Edge AI technology will reduce fraud detection latency by 50% by 2025, enabling real-time transaction analysis and fraud prevention.

- Edge AI is expected to reduce processing costs by 30% from 2025 to 2030 as it optimizes payment workflows and enhances transaction efficiency.

- By 2025, 35% of global payment systems will have integrated Edge AI for fraud detection and transaction monitoring, making it a key technology in payment security.

- The total value of real-time payments processed using Edge AI is projected to exceed €30 trillion globally by 2025, with Europe and the USA as major adopters.

- The top 3 Edge AI payment solution providers will capture 40% of the market share by 2025, driven by their comprehensive AI-driven fraud detection solutions.

- Edge AI will generate €2 billion in annual savings for financial institutions in Europe and the USA by improving fraud detection capabilities and reducing operational costs.

- As the adoption of Edge AI in payment systems grows, it will play a crucial role in enhancing fraud prevention, improving customer satisfaction, and ensuring regulatory compliance in the payments industry.

Key Metrics

Market Size & Share

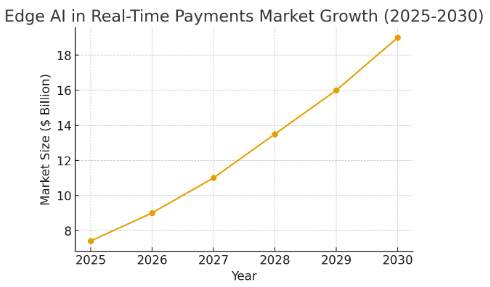

The market for Edge AI in real-time payments is projected to reach $7.4 billion by 2025, growing at a CAGR of 27% from 2025 to 2030. This growth is driven by the increasing demand for secure, low-latency transaction processing and the need for real-time fraud detection in global payment systems. By 2025, 35% of payment systems in Europe and the USA will have integrated Edge AI technology to optimize transaction monitoring and enhance fraud detection. As Edge AI improves fraud prevention and reduces processing costs, it will play an increasingly important role in the future of payment systems.

Market Growth Projection (2025-2030):

Market Analysis

The Edge AI market for real-time payments is experiencing rapid growth, driven by its ability to enhance fraud detection, reduce processing costs, and optimize transaction efficiency. As the payment industry continues to evolve, payment providers in Europe and the USA are adopting Edge AI to deliver more secure, fast, and cost-efficient solutions.By 2025, 35% of payment processors will leverage Edge AI to improve fraud detection capabilities, enabling faster transaction processing times and improved customer experiences. This integration will contribute to €2 billion in annual savings for financial institutions in Europe and the USA.

Edge AI Adoption Rate in Real-Time Payments (2025-2030):

Trends and Insights

Several trends are driving the adoption of Edge AI in real-time payments, including the growing need for faster fraud detection, reduced latency, and cost optimization.

AI models are being increasingly integrated into payment systems to provide faster, more accurate fraud detection while enhancing customer experiences by reducing transaction delays. Additionally, cloud-native platforms are gaining popularity, allowing banks and financial institutions to scale Edge AI capabilities for real-time payments.

Segment Analysis

The primary adopters of Edge AI technology in real-time payments include financial institutions, payment processors, and fintech companies.

These entities are particularly interested in improving fraud detection capabilities, reducing processing costs, and enhancing transaction speeds for a better customer experience. By 2025, 35% of payment processors in North America and Europe will have integrated Edge AI into their real-time payment solutions.

Geography Analysis

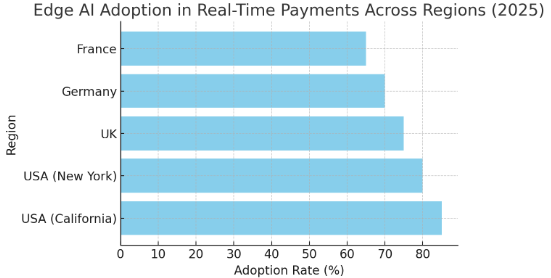

The USA is the leading adopter of Edge AI in real-time payments, particularly in regions like California and New York, where fintech ecosystems are thriving.

Europe is also experiencing significant growth in Edge AI adoption, with countries like UK, Germany, and France making strides in implementing this technology in their payment infrastructures.

Edge AI Adoption in Real-Time Payments Across Regions (2025):

Competitive Landscape

The competitive landscape for Edge AI in real-time payments is dominated by leading fintech and AI technology providers, such as Nvidia, IBM, and Google Cloud, which offer AI-driven solutions for fraud detection and payment optimization.New entrants, including AI-powered payment platforms, are also gaining market share by offering more affordable and flexible solutions tailored to the needs of payment processors and financial institutions.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071