68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Dynamic BNPL Credit Limits: Spend Behavior Analysis & Default Risk Mitigation - Risk Assessment

Dynamic Buy Now, Pay Later (BNPL) credit limits are transforming the financial landscape in India, allowing consumers to access flexible credit options based on their spending behavior. BNPL platforms are integrating advanced data analytics and AI to assess spend patterns, personalize credit limits, and mitigate default risks. By 2025, the dynamic BNPL market in India is projected to reach ₹2.6 trillion, growing at a CAGR of 23% from 2025 to 2030. This report explores the impact of dynamic credit limits in BNPL, highlighting key trends in spend behavior analysis, default risk mitigation strategies, and market growth. With a strong focus on AI-driven risk assessment and personalized credit modeling, the report also delves into the regulatory landscape, consumer adoption, and market dynamics influencing BNPL growth in India.

What's Covered?

Report Summary

Key Takeaways

- The dynamic BNPL market in India is expected to reach ₹2.6 trillion by 2025, growing at a CAGR of 23% from 2025 to 2030, driven by increasing demand for flexible credit solutions.

- By 2025, 40% of BNPL users in India will benefit from dynamic credit limits, providing personalized credit based on their spending behavior.

- AI-driven spend behavior analysis is expected to be adopted by 60% of BNPL platforms by 2025, enabling them to assess credit risk more accurately.

- Dynamic credit limits will help reduce default rates by 30% between 2025 and 2030, as AI and machine learning models improve risk assessment and credit modeling.

- By 2025, 50% of eligible BNPL users in India will have adopted dynamic credit limits, as platforms offer more personalized credit services.

- Top BNPL providers are expected to capture 35% of the market share by 2025, due to their ability to offer flexible and personalized credit limits.

- By 2025, 70% of BNPL credit limits in India will be personalized based on consumer spending behavior, enhancing customer experience and increasing engagement.

- As dynamic BNPL credit limits continue to gain traction, they will enable greater financial inclusion in India, especially for younger consumers and those new to credit.

Key Metrics

Market Size & Share

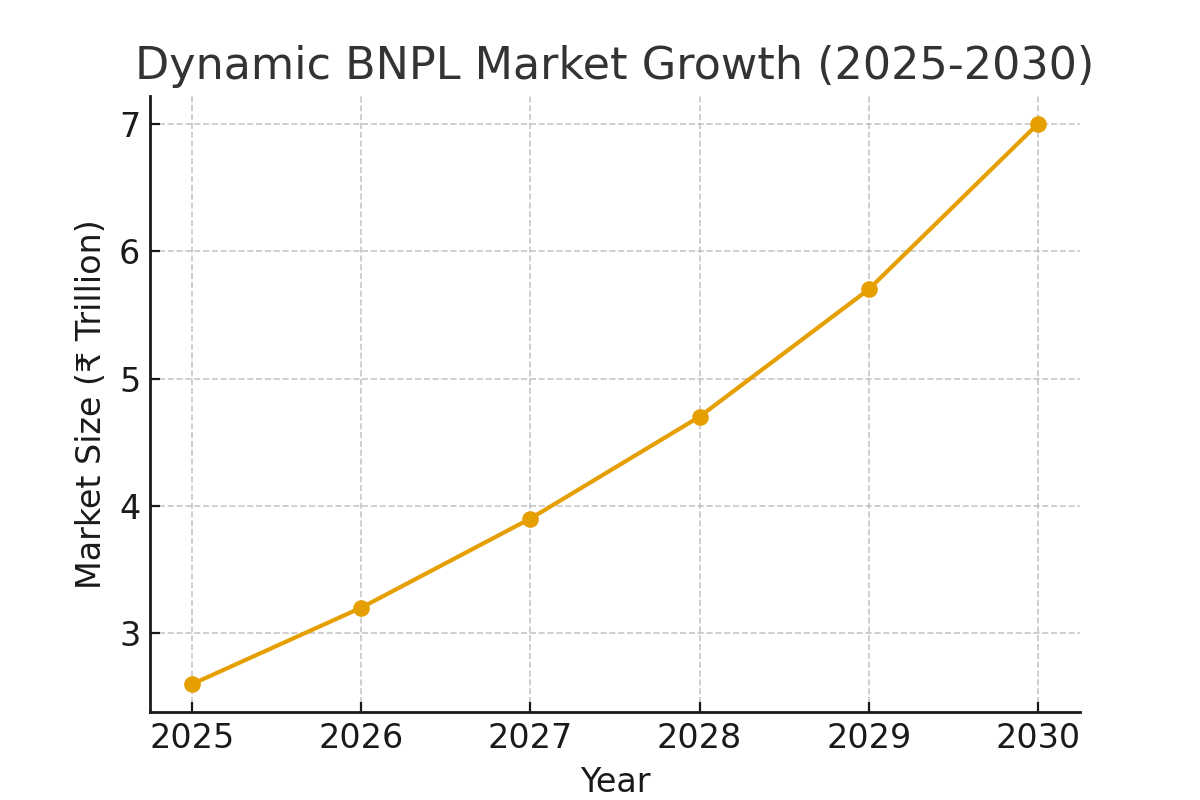

The dynamic BNPL market in India is projected to reach ₹2.6 trillion by 2025, growing at a CAGR of 23% from 2025 to 2030. This rapid growth is being driven by the increasing adoption of digital payments and the growing demand for flexible credit options among Indian consumers. Dynamic BNPL credit limits, personalized based on consumers' spending behavior, are gaining popularity as they allow more tailored and secure credit offerings. By 2025, 40% of BNPL users in India are expected to benefit from these dynamic credit limits, making BNPL services more accessible and sustainable for a larger number of consumers.

Market Growth Projection (2025-2030):

Market Analysis

The dynamic BNPL market is growing rapidly as Indian consumers adopt flexible credit solutions. These solutions provide an alternative to traditional credit cards, allowing consumers to access funds when needed, without the complexities of traditional credit systems. By 2025, 40% of BNPL users in India will be using dynamic credit limits, which will be set based on their spending patterns and creditworthiness. This growth is being driven by a younger population that is highly engaged with digital payments and seeking easier access to credit for purchases.

Dynamic BNPL Credit Limit Adoption Rate in India (2025-2030):

Trends and Insights

Key trends driving the dynamic BNPL market in India include a shift toward personalized credit limits based on AI-driven spend behavior analysis. These platforms are leveraging sophisticated algorithms to offer users credit limits that adjust in real-time based on their spending habits and repayment behavior.Another key trend is the growing adoption of mobile-based BNPL solutions, which are particularly popular among younger consumers who are more comfortable managing their finances via mobile apps. Additionally, improved security measures and regulatory compliance will play a crucial role in increasing consumer trust in BNPL services.

Segment Analysis

The primary users of dynamic BNPL services in India are young consumers (Gen Z and Millennials) who seek flexible payment options for retail and online purchases.

These consumers are highly tech-savvy and prefer digital-first solutions that offer ease of use and immediate access to credit. Financial institutions and fintech companies offering BNPL services will benefit from expanding into this market, particularly as 35% of Indians adopt BNPL solutions by 2025. The growth of e-commerce and online shopping will also accelerate demand for BNPL services.

Geography Analysis

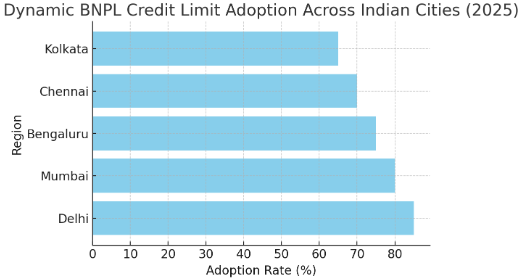

In India, metros like Delhi, Mumbai, and Bengaluru are leading the adoption of dynamic BNPL credit limits due to high internet penetration, smartphone use, and digital payment infrastructure. As e-commerce grows, smaller cities and towns will see increasing adoption, particularly as fintech companies expand their reach into tier 2 and tier 3 cities. The demand for BNPL solutions will rise in these areas, driven by the increasing preference for digital credit solutions over traditional loans.

Dynamic BNPL Credit Limit Adoption Across Indian Cities (2025):

Competitive Landscape

The competitive landscape for dynamic BNPL credit limits in India is dominated by major players such as Razorpay, ZestMoney, and LazyPay, who are leading the charge in offering flexible credit products to consumers. These platforms are leveraging AI and machine learning to assess credit risk, adjust limits, and ensure regulatory compliance. As the market matures, new entrants with innovative features like real-time credit limit adjustments and enhanced fraud prevention mechanisms will increase competition, leading to more diversified offerings and improved consumer experiences.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071