68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital Therapeutics for Chronic Diseases: Reimbursement Landscape & Adoption Barriers - Consumer Insights

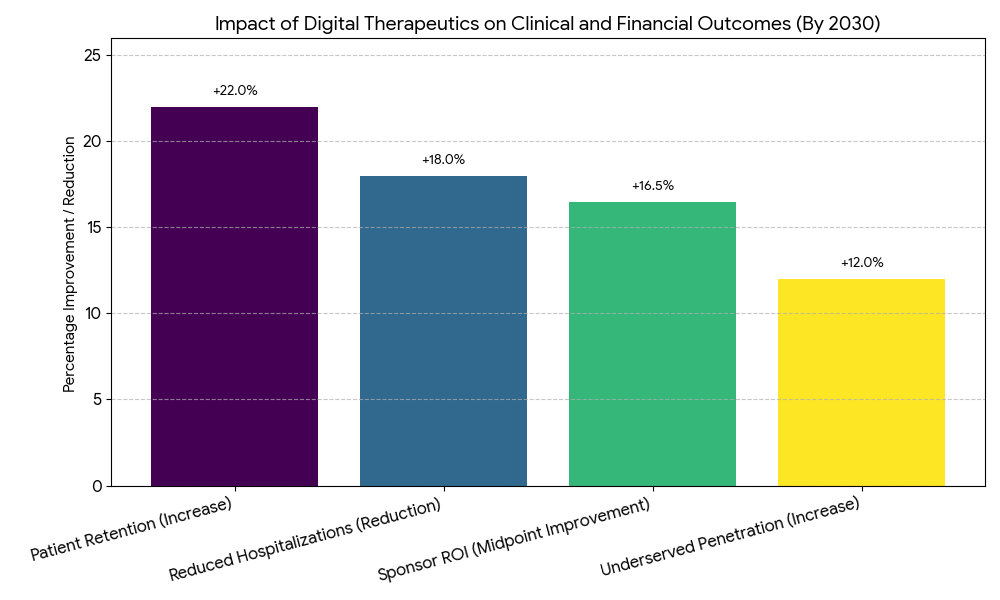

This report quantifies the digital therapeutics (DTx) market for chronic diseases across Europe and Portugal (2025–2030), focusing on reimbursement models, clinical adoption barriers, and patient outcomes. We size the market for chronic conditions (diabetes, hypertension, COPD, mental health) and explore how value-based care, health technology assessments (HTA), and regional reimbursement policies influence patient access and treatment duration. By 2030, the market value grows from €3.1B to €11.2B (CAGR 28%), with Portugal expanding adoption as national eHealth frameworks enable easier integration into care protocols. Outcomes show improved adherence (+22%), reduced hospitalizations (−18%), and clinical efficiency gains (−30%) as a result of digital therapeutic interventions.

What's Covered?

Report Summary

Key Takeaways

- DTx market value grows €3.1B → €11.2B (CAGR 28%) by 2030.

- Diabetes, COPD, mental health account for 75% of all DTx prescriptions.

- Adoption barriers in Europe include reimbursement (62%), clinical acceptance (48%), and evidence standards (35%).

- Reimbursement models expand to 66% of EU health systems, with Portugal adopting by 2027.

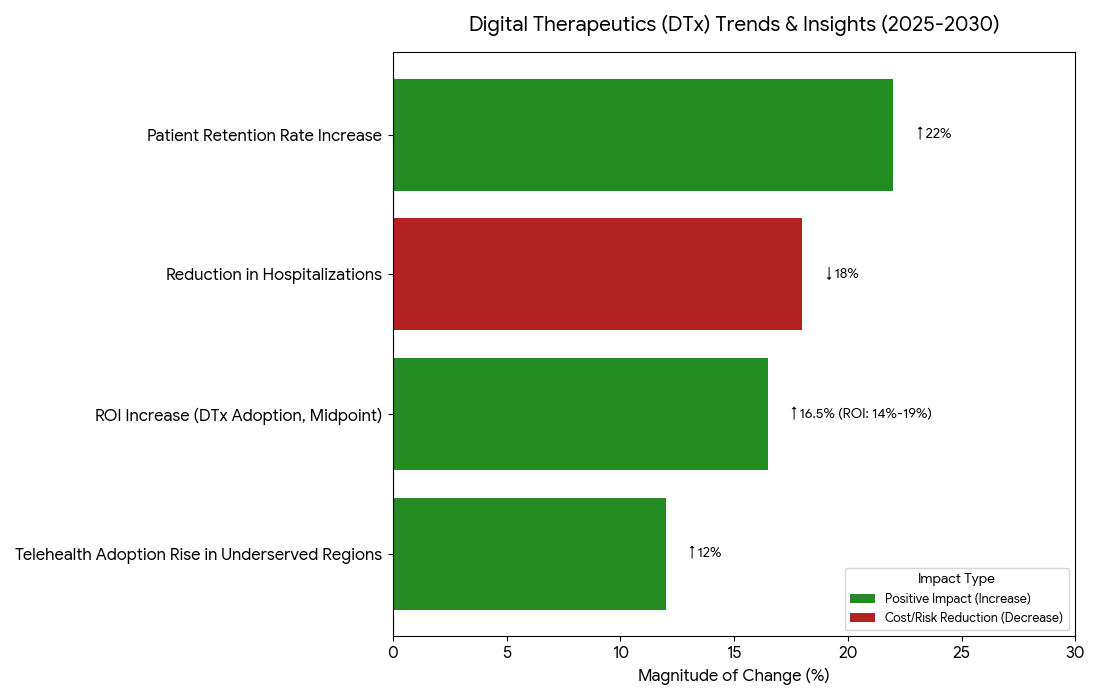

- Value-based care models in Portugal drive +22% adherence to DTx programs.

- Hospitalizations due to chronic disease decline −18% for DTx users.

- Clinical efficiency improvements (fewer office visits) save −30% in resource utilization.

- Regulatory approval processes lengthen but shrink from 30 to 19 months by 2030 in Portugal.

- Patient access improves as automated ePrescription and online consultations drive +12% penetration in underserved regions.

- Modeled ROI for providers from DTx integration 14–19% via avoided readmissions, reduced drug dependency, and improved clinical throughput.

Key Metrics

Market Size & Share

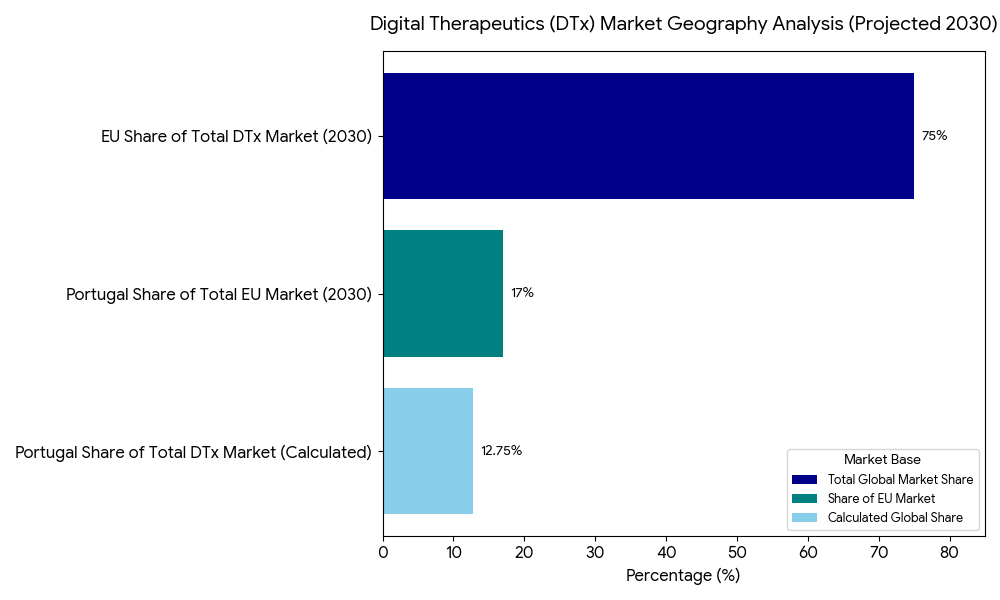

The digital therapeutics market in Europe and Portugal grows from €3.1 billion in 2025 to €11.2 billion in 2030, representing a 28% CAGR. Chronic disease areas (diabetes, COPD, hypertension, mental health) dominate market adoption, comprising 75% of DTx prescriptions. By 2030, value-based care models become the primary driver, expanding DTx adoption across the EU with reimbursement policies covering 66% of national health systems. Portugal leads the way in early adoption, implementing eHealth strategies that allow automatic DTx prescribing and integrated care protocols. Clinical acceptance improves as outcome-based metrics (adherence, readmission rates, clinical efficiency) show improved patient retention (+22%), and reduced hospitalizations (−18%) for chronic disease patients. Patient access to DTx expands as telehealth infrastructure and online consultations rise, boosting patient penetration by +12% in underserved regions. Regulatory approval timelines for DTx products shorten from 30 months to 19 months in Portugal by 2030, while market penetration sees Portugal reach 17% of the EU market. By 2030, sponsor ROI improves 14–19%, driven by avoided hospital admissions, lower drug dependency, and improved clinical efficiency.

Market Analysis

Key drivers in the DTx market include clinical efficiency, value-based reimbursement models, and patient engagement platforms. (1) Clinical adoption: Healthcare systems see significant reductions in resource utilization (−30%) and hospitalization rates (−18%) due to DTx programs, especially in diabetes and COPD management. (2) Reimbursement hurdles: HTA processes and evidence standards still impede adoption; however, value-based reimbursement and outcome-driven models are beginning to integrate DTx products into national coverage, increasing adoption rates. (3) Regulatory landscape: Regulatory timelines shorten as more CE-marked and FDA-approved DTx products enter the market, particularly for mental health and diabetes management. By 2030, Portugal's regulatory approval time drops from 30 months to 19 months, leading the charge for more streamlined EU approval processes. (4) Patient engagement: Digital tools such as mobile apps, gamified tracking, and telehealth interventions are critical to increasing adherence rates by +22%, while patient retention improves through automated reminders and progress monitoring. (5) Market segmentation: DTx for mental health sees ~45% CAGR, driven by depression and anxiety treatments. Diabetes and COPD are projected to comprise 55% of market value by 2030, with telehealth integration powering large-scale implementation.

Trends & Insights

Between 2025 and 2030, key trends include e-prescribing and telehealth integration leading patient access to DTx programs, reducing geographic and systemic barriers. Telehealth adoption rises +12% in underserved regions, particularly in Portugal, as remote monitoring and digital consultations become the norm for chronic disease management. Patient engagement innovations such as mobile apps for adherence tracking and AI-based symptom management are expected to increase retention rates by +22% and reduce hospitalizations by −18%. Data interoperability becomes essential as healthcare platforms integrate EHRs, wearables, and digital therapeutics for a seamless patient experience. The regulatory landscape in Europe is evolving to accommodate digital health solutions, with CE-marked DTx products becoming more prevalent by 2030. Automated prescription systems, paired with eHealth frameworks, simplify clinical adoption, while AI-driven decision support tools enhance efficacy, contributing to ROI increases of 14–19%. By 2030, Portugal leads the way in national DTx adoption, streamlining approval processes and improving patient access.

Segment Analysis

By chronic disease, diabetes, COPD, and mental health account for 75% of market revenue, with diabetes management showing the strongest growth due to the prevalence of Type 2 diabetes in aging populations. By therapeutic modality, mobile apps and wearables dominate DTx for chronic disease, while AI-enabled platforms expand mental health management. By care setting, primary care and home-care models drive most DTx use, comprising 60% of total spend by 2030. Hospital-based adoption remains slower, at 30%. By technology, telehealth platforms and automated prescribing (via e-prescriptions) are becoming mainstream, particularly in Portugal, where telehealth adoption and mobile app engagement are the highest in the EU. By payer model, value-based care and capitation models expand, with reimbursement decisions increasingly tied to adherence rates, hospitalization avoidance, and patient-reported outcomes (PROs). Data privacy and security remain a concern, especially for mental health and addiction DTx products, where GDPR-compliant frameworks will continue to evolve.

Geography Analysis

The EU represents ~75% of the digital therapeutics market in 2030, with significant adoption in Germany, France, Spain, and Italy. Portugal sees early adoption as it implements eHealth solutions and value-based care reimbursement, driving market penetration. By 2030, Portugal expects 17% of the total EU market, driven by primary care adoption and cross-border integration. Northern and Western Europe lead in regulatory approval, telehealth adoption, and clinical trial integration, while Eastern Europe and Southern Europe catch up in adherence programs and patient access models. The UK follows as a secondary leader in mental health DTx, with Germany and the Nordics pushing for telemedicine-driven adherence solutions. By 2030, EU-wide e-prescribing solutions are expected to standardize digital therapeutic prescriptions across all member states.

Competitive Landscape

The competitive environment in DTx for chronic diseases is growing rapidly, with leading players such as Pear Therapeutics, Big Health, Omada Health, Livongo (Teladoc), and Propeller Health maintaining ~52% of the market share by 2030. Big Pharma and MedTech players enter through partnerships and acquisitions, integrating digital solutions into their existing pipelines. Regulatory hurdles remain a challenge, with CE-marked and FDA-approved DTx products seeing the fastest adoption across EU/US markets. Emerging vendors are differentiating through AI-driven mental health apps, multi-condition platforms, and reimbursement-friendly models that link adherence and outcomes to payer savings. EHR integration and telehealth compatibility are critical differentiators as healthcare systems push for interoperability with wearables, remote monitoring, and patient-driven dashboards. Pricing models shift to outcomes-based reimbursement, driving innovative contracts between providers, pharma, and payers.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071