68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Crypto Payment Adoption in EU vs. U.S. Merchants (2025–2030): Volume Growth, Ticket Sizes & Merchant ROI

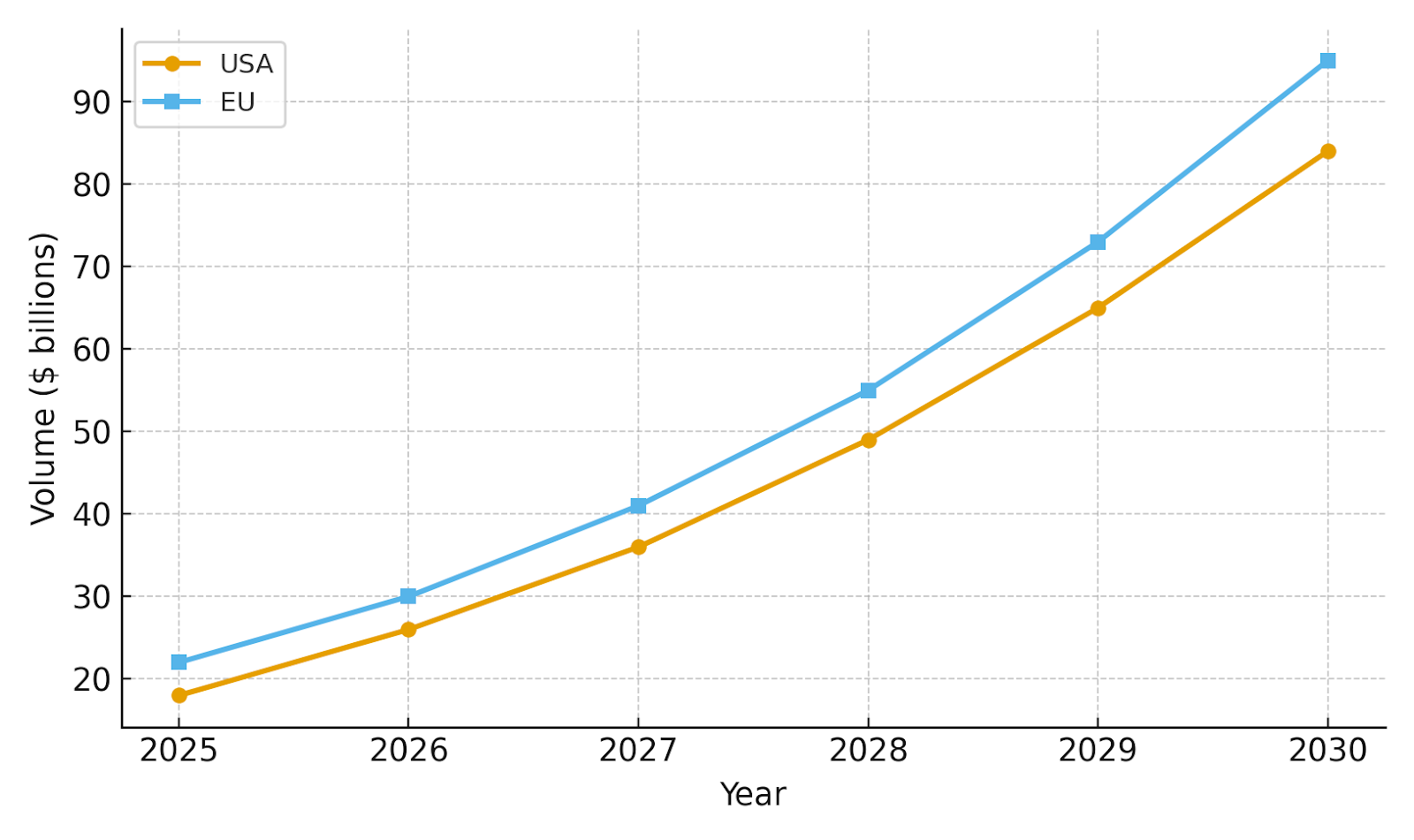

Between 2025 and 2030, U.S. merchants will shift from experimental crypto payment pilots to scalable, ROI-focused deployments, spurred by stablecoin integration, wallet-based customer authentication, and automated compliance solutions. U.S. merchant crypto volumes are projected to grow from $18 billion in 2025 to $84 billion by 2030, while EU volumes increase from $22 billion to $95 billion, thanks to more harmonized regulations like MiCA and PSD2/3. Growth drivers include better settlement speed, lower fraud, improved conversion, and dynamic multi-rail payment orchestration. By 2030, crypto will be integrated as an optional enterprise payment rail, enhancing the economics and reach of business transactions.

What's Covered?

Report Summary

Key Takeaways

- Stable coin rails and wallet SCA drive conversion and fraud gains.

- EU policy clarity hastens mainstream rollouts; U.S. relies on orchestration abstraction.

- Highest ROI cohorts: cross‑border retail, travel/leisure, digital goods/marketplaces.

- Average ticket sizes rise where B2B cross‑border and supplier payments adopt crypto.

- PSP guarantees (fraud, settlement SLAs) are decisive for enterprise adoption.

- Automation (tax, AML/CFT, accounting) converts pilots into BAU finance ops.

- ROI must beat blended MDR+FX costs and preserve UX parity with cards.

- By 2030, crypto becomes a standard optional rail, not a wholesale replacement.

Key Metrics

Market Size & Share

The comparative volume curve shows EU slightly ahead of the U.S. by 2030 in total merchant crypto GMV (illustrative $95B vs. $84B). Two forces explain the gap: (1) policy clarity under frameworks like MiCA enables PSPs to roll out crypto rails to a wider base of merchants; (2) consumer protections and harmonized disclosures encourage adoption beyond early adopters. In the U.S., growth concentrates where crypto beats cards on cost or conversion—especially in cross‑border retail and travel/leisure—while orchestration platforms stitch together compliance, tax, and treasury automation.

Share dynamics: large retailers and travel/leisure account for the majority of absolute volumes due to higher basket sizes and cross‑border corridors. Digital goods and marketplaces scale quickly from a smaller base, with creator‑economy integrations. No single PSP or wallet dominates; multi‑rail routing and vendor diversification are standard. By 2030, crypto is an optional rail in most enterprise stacks, activated when corridor economics guarantee contribution margin over card rails.

Market Analysis

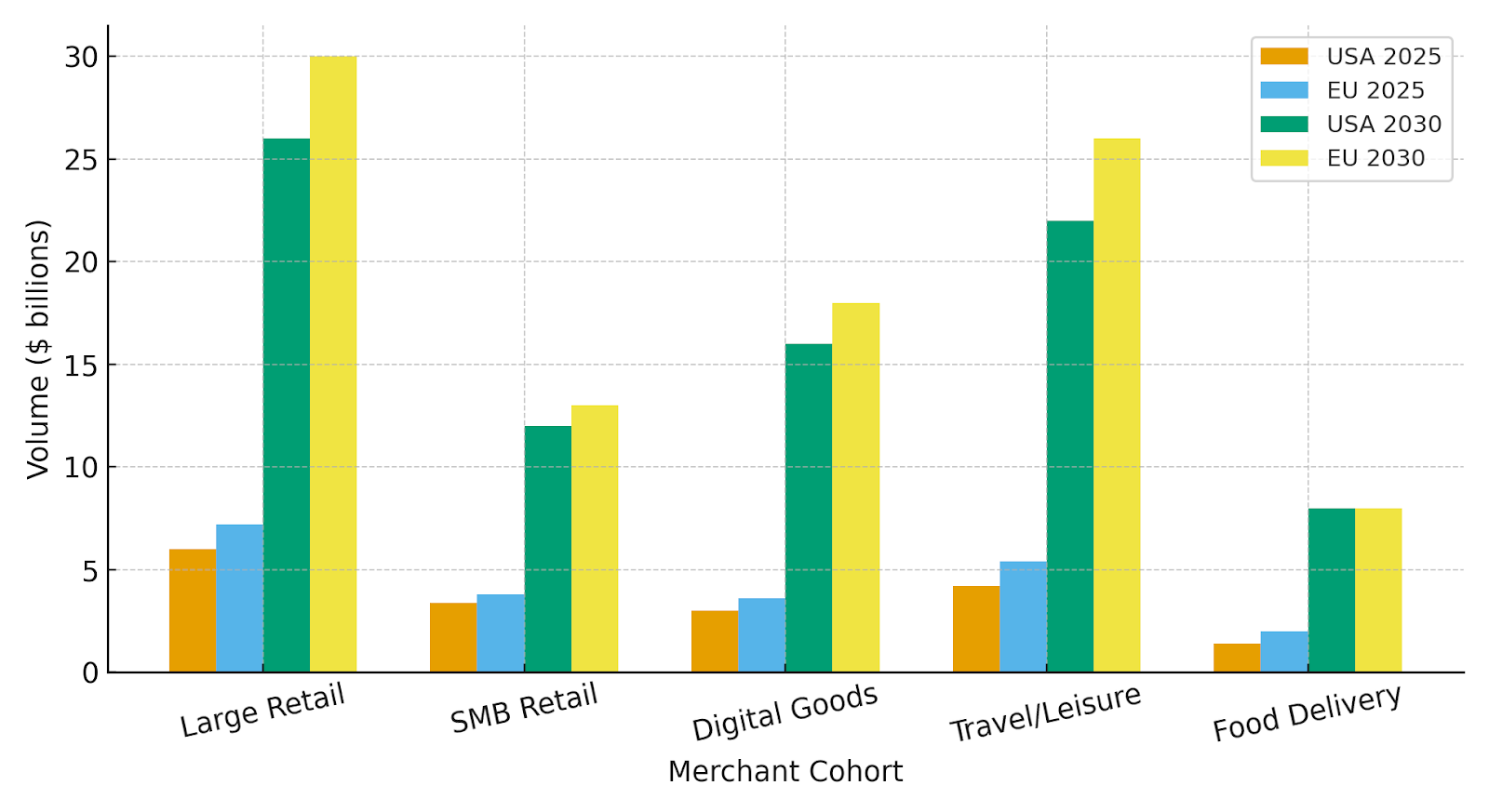

The cohort bar chart compares USA vs EU for 2025 and 2030. The EU shows broader dispersion across SMB retail and food delivery due to consumer protections and standardized disclosures, whereas the U.S. remains concentrated in higher‑ticket categories and cross‑border corridors. Digital goods and marketplaces benefit in both regions from push‑payment design and wallet SCA that reduce refund abuse and false declines.

Buying determinants are consistent across regions: (i) cost parity or improvement vs. cards (FX bypass, lower MDR, fewer chargebacks), (ii) conversion uplift via wallet SCA, (iii) operational automation (tax, AML/CFT, accounting, refund tooling), and (iv) reliable settlement SLAs and banking access. EU PSPs tend to compress fees earlier, while U.S. providers emphasize orchestration flexibility and corridor‑specific guarantees.

Geography Analysis

Within the United States, adoption is weighted to the West (~36%) and South (~31%)—reflecting tech concentration, cross‑border commerce intensity, and crypto‑native consumer segments. The Northeast (~19%) leads in enterprise experimentation and corporate treasury use cases; the Midwest (~14%) grows through PSP plugins and SMB commerce. EU‑U.S. comparative geography matters primarily in corridor planning: EU merchants rely on harmonized protections, whereas U.S. merchants depend on platform abstraction and corridor‑specific economics.

Trends & Insights

• Stablecoin resilience (reserves, attestation, banking) defines merchant confidence.

• Wallet‑native experiences (tokenized identity, SCA) improve auth and lower fraud.

• Multi‑rail checkout stacks become default; routing is governed by policy rules.

• EU’s harmonization accelerates mass‑market PSP offerings; U.S. remains platform‑driven.

• B2B cross‑border use cases lift average tickets and working‑capital benefits.

• Treasury automation (auto‑convert, ERP posting, reconciliation) converts pilots to BAU.

• Analytics instrumentation compares card vs. crypto funnels at SKU/category resolution.

• Vendor ecosystems consolidate around PSPs offering guarantees and compliance evidence.

Segment Analysis

• Large Retail: Negotiates fee floors and corridor guarantees; adopts wallet checkout; tests loyalty‑crypto blends.

• SMB Retail: Leans on PSP plugins to abstract compliance and tax; targets crypto‑native niches.

• Digital Goods/Marketplaces: Early adopters of push‑payments and escrow; reduce refund abuse.

• Travel/Leisure: Gains most from FX netting and faster settlement; high ticket sizes persist.

• Food Delivery/QSR: Small tickets but frequent; UX and loyalty tie‑ins drive adoption.

Enterprise success patterns: define corridor policies, instrument KPIs (auth, fraud, refunds, cost/tx), and automate treasury actions. EU firms scale broadly across tiers; U.S. firms scale where corridor economics are clearly superior to cards.

Competitive Landscape

The competitive field spans (1) PSPs/orchestrators adding crypto rails; (2) stablecoin issuers and regulated on/off‑ramps; (3) wallets providing merchant‑grade SCA and tokenized identity; and (4) analytics/tax/reporting tools. Differentiation hinges on conversion uplift, fee transparency vs. cards, refund/escrow tooling, ERP automation, and compliance evidence. Expect consolidation around PSPs that deliver multi‑rail routing, corridor guarantees, and standardized audit packs. EU vendors gain speed from policy clarity; U.S. vendors win via flexible orchestration and SLA‑backed economics.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071