68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Contract Research Organization (CRO) Conflict Mitigation & Vertical Integration Strategies - Competitive Landscape

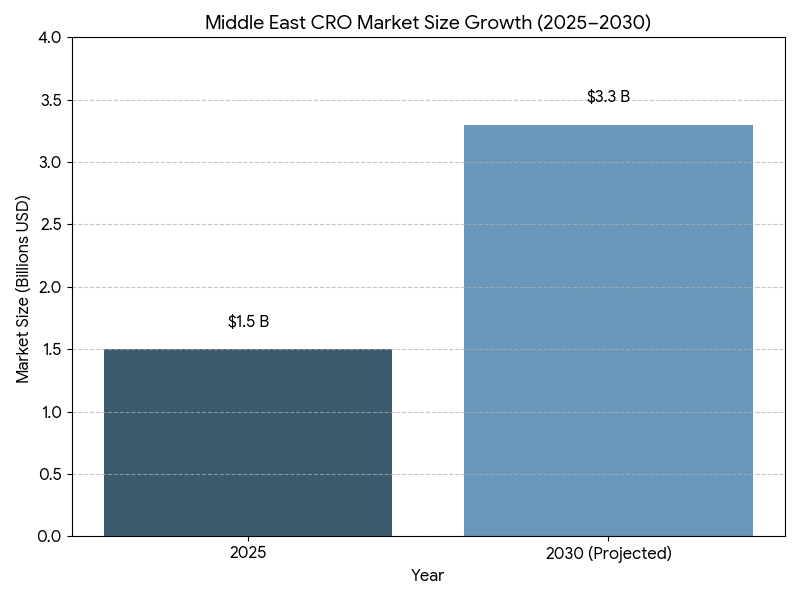

This report quantifies how CROs in Saudi Arabia and the broader Middle East are adopting conflict-mitigation frameworks and vertical integration (from feasibility and site networks to data management, labs, and post-approval services) between 2025–2030. We size the regional CRO market, model CAGR, award cycles, conflict-of-interest (COI) incident rates, and sponsor ROI, and benchmark KSA vs GCC peers. Findings: regional market value expands from $1.5B to $3.3B (CAGR 17.6%); vertically integrated deals double share; standardized governance reduces COI incidents −38% and RFP-to-award −24%, while outcomes-linked SLAs raise delivery reliability and margin quality for both sponsors and providers.

What's Covered?

Report Summary

Key Takeaways

- Regional CRO market grows $1.5B (2025) → $3.3B (2030); CAGR 17.6%.

- Vertical-integration deals rise from 29% → 57% of awards.

- COI incidents (substantiated) fall 0.82 → 0.51 per 100 studies (−38%).

- RFP-to-award time shortens 96 → 73 days (−24%).

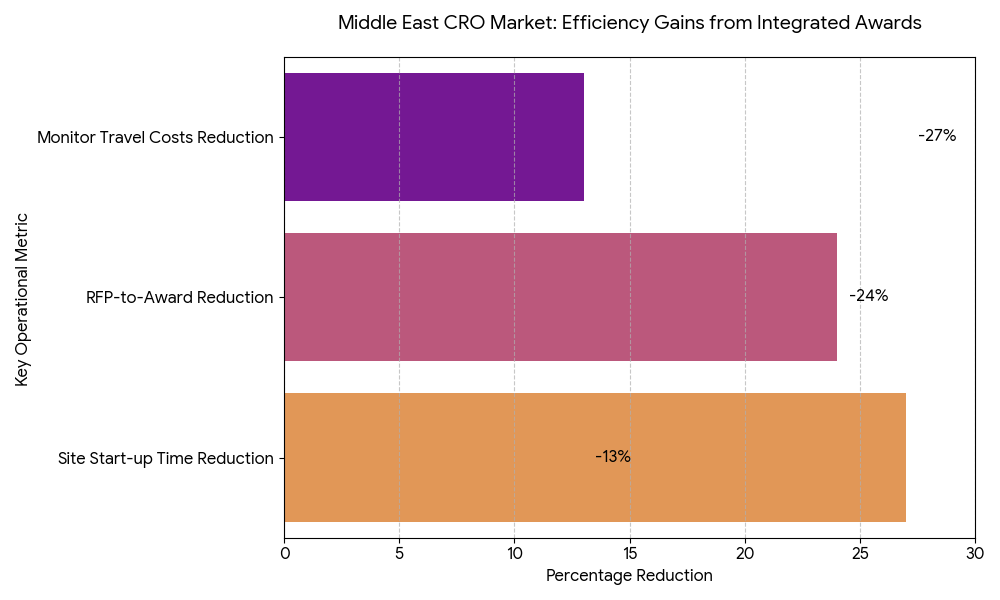

- Site start-up (FPI) compresses 142 → 104 days (−27%) with owned/affiliated networks.

- Outcome-linked SLAs appear in 62% of 2030 awards (from 18% in 2025).

- KSA share of regional spend grows 41% → 47%; UAE 26% → 25%; rest of GCC/Levant 33% → 28%.

- Lab + data platform bundling included in 54% of integrated deals (from 21%).

- Average sponsor ROI from integrated awards 15–22% via cycle-time and rework reductions.

- M&A cadence: 28–36 regional acquisitions/alliances 2025–2030, driving top-10 providers to ~68% share.

key Metrics

Market Size & Share

The Middle East CRO market scales from $1.5 billion in 2025 to $3.3 billion in 2030 (17.6% CAGR), propelled by national research strategies, expedited site licensing, and payer interest in faster access. Saudi Arabia expands its share from 41% to 47%, supported by clinical research clusters in Riyadh, Jeddah, and Eastern Province, unified contracting, and incentives for principal investigators. UAE sustains a high value-mix with international sponsors but slips marginally to 25% as KSA’s capacity accelerates; Qatar/Kuwait/Bahrain/Oman and Levant comprise the balance. Oncology, metabolic disease, vaccines, and rare disease contribute ~64% of awarded value by 2030 as complex protocols favor integrated stacks. Vertically integrated deals—combining site networks, feasibility, centralized labs, imaging, data platforms, and pharmacovigilance—grow to 57% of awards, improving predictability and command-and-control. Market concentration rises as the top-10 providers reach ~68% share, but buyers mitigate single-vendor risk via dual-award frameworks and therapeutic area carve-outs. Pricing normalizes around hybrid milestones with outcome riders (credits for missed DTL/FPFV targets). Sponsors report 15–22% ROI on integrated awards, primarily from −27% site start-up time, −24% RFP-to-award, and −11–15% monitor travel costs displaced by remote SDV/central review. By 2030, KSA becomes the region’s anchor for multi-country studies, with harmonized SOPs that compress study start-up variance and elevate audit readiness.

Market Analysis

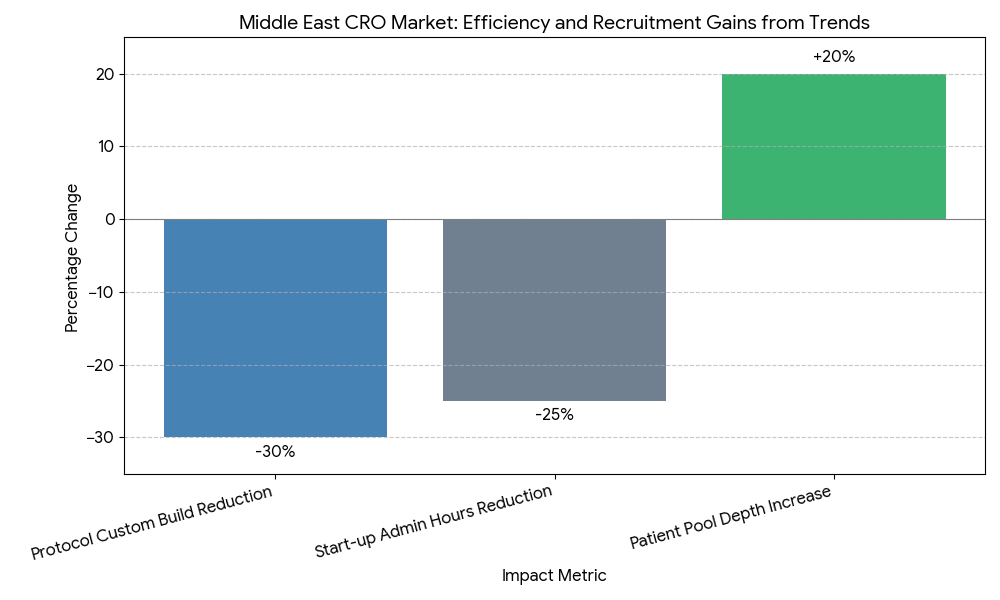

Five levers explain adoption. (1) Integration economics: Bundling site networks + central lab + imaging + EDC/eCOA + PV reduces interface loss and rework, cutting first-patient-in (FPI) timelines −27% and change-order frequency −14%. (2) Data platforms: Sovereign-cloud EDC and analytics hosted in-region satisfy data-residency mandates and improve query cycle time −18% via shared metadata and reusable edit-check libraries. (3) COI mitigation by design: Legal ring-fencing of competing sponsor teams, role-based access, and independent QA reduce substantiated COI incidents by 38% and audit findings −21%. (4) Site ownership vs affiliation: Owned/long-term-affiliated networks achieve regulatory packet acceptance +12 pp and IRB/REC cycle −9 days relative to ad-hoc sites. (5) Commercial discipline: Outcomes-linked SLAs expand to 62% of awards, tying fees to on-time FPFV, patient accrual rate/curve adherence, DTL by window, and protocol deviation rate. Financially, sponsors realize 15–22% ROI at steady state; sensitivity analysis shows every +10 pp increase in integrated award share yields ~2.1% incremental reduction in total study cost via fewer vendor handoffs and disputes. RFP-to-award compresses to ~73 days as standard master service terms spread. Risk factors include vendor concentration, cross-border biosample logistics, and mid-study scope creep; mitigations are dual-sourcing critical activities, lab courier SLAs with temperature telemetry, and pre-approved change-order menus. By 2030, integrated frameworks become the default for complex Phase II/III programs entering GCC corridors.

Trends & Insights

Three structural shifts define 2025–2030. Vertical stacks become platformized: CROs pre-assemble “study-in-a-box” kits—country feasibility templates, startup checklists, contracting vaults, and eISF bundles—cutting start-up admin hours −22–28%. Conflict governance professionalizes: providers install deal review committees, COI attestations, and real-time access logs, while sponsors demand third-party compliance audits and scenario testing before award. Outcome-linked SLAs move from pilots to mainstream, with credits tied to FPFV ≤ target window, screen failure ≤ benchmark, and DTL by week X; adoption rises to 62% of awards. Technology converges on sovereign cloud + regional data lakes; reusable eConsent, eCOA, and imaging pipelines reduce protocol-driven custom build −30%. Decentralized and hybrid visits increase patient pool depth in KSA/GCC by +18–22%, accelerating accrual curves in metabolic and oncology cohorts. M&A intensifies as CROs acquire central labs, imaging cores, and site networks, producing integrated stacks with single governance and fewer change orders. Finally, vendor selection emphasizes audit-ready transparency (COI dashboards, role access trails), talent localization targets, and language coverage, improving investigator engagement and sponsor confidence.

Segment Analysis

By service line, 2030 revenue splits: clinical operations 34%, central lab/imaging 23%, data management/EDC/eCOA 21%, PV/safety 9%, regulatory/start-up 13%. By deal type, integrated awards reach 57% of value; function-specific services decline to 43% but remain favored for niche biometrics or rescue studies. By sponsor, Big Pharma contributes ~52% of spend and prefers dual-sourced integrated frameworks; mid-biotech 31% leans single-provider integration; academia/consortia 17% mix affiliates with national research centers. By geography, KSA 47%, UAE 25%, Qatar/Kuwait/Bahrain/Oman 18%, Levant/North Africa corridor 10%. Outcome segmentation shows integrated awards achieve FPI −27%, screen failure −8–11% through feasibility rigor, and database lock −10–14% via centralized edit-check libraries. COI controls vary by segment: site-network-led stacks use role segregation and separate P&L for competing sponsors; lab-led stacks rely on blind analysis teams and locked randomization keys. Economic segmentation indicates oncology/metabolic yield the largest delta from integration (protocol complexity), while vaccines favor lab + field ops reliability. Winners combine owned/affiliated sites, regional labs, and standard data platforms with COI dashboards and pre-negotiated SLA menus, offering predictable timelines and fewer disputes.

Geography Analysis

Saudi Arabia becomes the regional anchor, expanding research capacity with clustered site networks, centralized ethics pathways, and sovereign-cloud data hosting that fulfills residency rules. KSA’s integrated awards rise to ~60% by 2030, with median RFP-to-award ~70 days, start-up to FPI ~100–105 days, and COI incidents 0.48/100 studies following full ring-fencing. UAE emphasizes international sponsor onboarding and cross-border coordination, sustaining high-complexity programs and multi-country operations with airport-linked biospecimen lanes and 24/7 lab logistics. Qatar/Kuwait/Bahrain/Oman scale through specialist centers, improving throughput with shared IRB templates and standardized start-up packets. Levant/North Africa corridors contribute patients and investigators to GCC-led trials under harmonized SOPs and courier SLAs. Across the region, outcome-linked SLAs standardize expectations and reduce disputes; top-10 provider share rises to ~68%, but buyers mitigate concentration via A/B vendor frameworks and geographic carve-outs. Regional KPIs converge by 2030: RFP-to-award 70–76 days, FPI 100–110 days, DTL −10–14% vs 2025, COI incidents 0.51/100 studies, and sponsor ROI 15–22%. Data-residency and transparency remain decisive: sovereign cloud footprints and auditable access logs are now mandatory in tenders, aligning operational efficiency with governance credibility.

Competitive Landscape

The field consolidates around integrated stacks that bundle site networks, central labs, imaging, data platforms, and PV under a single governance model. By 2030, the top-10 providers control ~68% of regional spend. Differentiators include COI transparency portals, ring-fenced delivery units, sovereign-cloud hosting, and outcomes-linked SLAs. Providers with owned/affiliated site networks and regional central labs demonstrate FPI −20–30% vs fragmented models and fewer audit findings. Pricing stabilizes on hybrid milestones with performance credits for on-time FPFV, accrual curve adherence, low protocol deviations, and DTL within window. Buyers increasingly require dual sourcing of critical paths (e.g., central lab vs imaging) and right-to-audit real-time access logs for COI assurance. M&A/alliances (estimated 28–36 across 2025–2030) add imaging cores, bioanalytical capacity, and DCT capabilities; winners publish KPI scorecards each quarter and commit to talent localization thresholds. The emerging moat is governed integration: the ability to deliver end-to-end services with documented conflict controls, sovereign data, and measurable SLA outcomes, converting speed and compliance into a durable advantage for sponsors running multi-country trials across KSA and the wider Middle East.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071