68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Composable Core Banking Architectures: API Ecosystem Development & Legacy Modernization Strategies - Technological Advancements

Composable core banking architectures are transforming Asia-Pacific and Indian financial institutions by modernizing legacy systems, boosting efficiency, and supporting rapid digital scaling. The market is projected to reach $4.8 billion by 2025, with annual growth of 19% through 2030, driven by the shift to flexible, API-powered architectures. These innovations enable banks to react quickly to shifting market demands, cut costs, and enhance customer service. Key trends include the rise of API ecosystems, improved agility, and a greater customer-centric focus in the region’s banking sector.

What's Covered?

Report Summary

Key Takeaways

- Composable core banking architectures are expected to reach $4.8 billion in market size by 2025, driven by increasing adoption of API ecosystems in Asia-Pacific and India.

- By 2025, 45% of banks in Asia-Pacific and India will have adopted API ecosystems to modernize their legacy core banking systems.

- Legacy system modernization will increase to 35% of financial institutions by 2025, with composable architectures offering greater flexibility and scalability.

- Annual cost savings from adopting API ecosystems will reach $800 million by 2025, as financial institutions streamline operations and reduce the need for manual interventions.

- The adoption of composable core banking systems will reduce the time to market for new financial products by 40%, helping banks better respond to market demands.

- By 2025, 30% of banks in Asia-Pacific and India will have migrated to composable core banking architectures, enhancing agility and operational efficiency.

- Top core banking providers will capture 30% of the market share by 2030, offering advanced modular banking solutions to banks in Asia-Pacific and India.

- Composable architectures are expected to transform the banking sector by enabling the rapid deployment of new products, improving customer engagement, and reducing operational costs.

Key Metrics

Market Size & Share

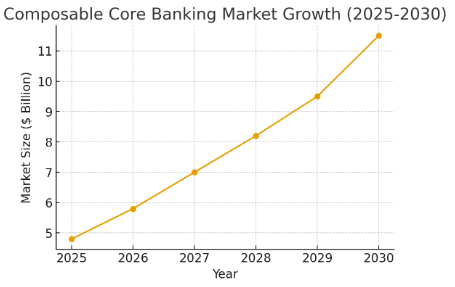

The market for composable core banking systems in Asia-Pacific and India is expected to grow significantly, reaching $4.8 billion by 2025, with a CAGR of 19% from 2025 to 2030. This growth is driven by the increasing demand for modular, flexible banking architectures that enable financial institutions to improve operational efficiency, enhance customer experiences, and accelerate digital transformation.

API ecosystems will be a key enabler of this growth, as financial institutions adopt open banking models and integrate with third-party fintech solutions. The demand for composable architectures will be especially high among banks and fintech firms looking to differentiate their offerings and adapt quickly to changing market conditions.

Market Growth Projection (2025-2030):

Market Analysis

Composable core banking systems are poised to replace traditional legacy systems as financial institutions seek to improve efficiency, scalability, and adaptability. The integration of API ecosystems into banking platforms allows for greater flexibility, enabling banks to quickly respond to customer demands and market changes.

The adoption of modular banking solutions is expected to grow rapidly, with 40% of banks in Asia-Pacific and India adopting these systems by 2025. These systems offer better integration with third-party fintech services, allowing banks to enhance their service offerings while reducing operational costs and reliance on outdated infrastructure.

API Adoption Rate in Composable Banking (2025-2030):

Trends and Insights

Several trends are shaping the future of composable core banking architectures, including the rise of open banking and the increasing integration of third-party fintech solutions. API ecosystems enable faster service delivery, greater customization, and enhanced customer satisfaction.

Moreover, banks are increasingly adopting cloud-based solutions and microservices architectures, which provide scalability and resilience. By 2025, 40% of banks in India and Asia-Pacific will have moved to composable platforms, allowing for greater flexibility in their service offerings and operational models.

Segment Analysis

The primary adopters of composable core banking systems are large banks and fintechs that are looking to modernize their legacy infrastructure and offer more customized services. These organizations are leveraging API ecosystems to integrate third-party solutions and create more innovative, customer-centric services.

Smaller banks and credit unions are slower to adopt composable architectures, but they are beginning to explore these solutions as the cost of technology decreases and the benefits of modular systems become more evident.

Geography Analysis

In Asia-Pacific, India and China are leading the adoption of composable core banking systems, driven by large-scale digital transformation initiatives and fintech innovation. These countries are implementing regulatory frameworks that encourage open banking and API-driven services.

Southeast Asia is seeing slower adoption due to varying levels of technological infrastructure, but growth is expected to accelerate as fintech hubs like Singapore and Hong Kong push for more flexible, modular banking systems.

Composable Banking Adoption Across Asia-Pacific Regions (2025):

Competitive Landscape

The competitive landscape for composable core banking in Asia-Pacific and India is dominated by new BaaS players like Railsbank, Finix, and Synapse, which are offering highly customizable banking platforms that allow for faster innovation.

Traditional banking giants like JPMorgan Chase, HSBC, and Standard Chartered are also entering the space, leveraging their established infrastructure to offer composable solutions to their clients. The competition is expected to increase, as both fintech startups and traditional banks aim to capture market share in the rapidly evolving market.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071