68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Cold Chain Revolution: Last-Mile Innovations for Perishable Goods in ANZ Markets

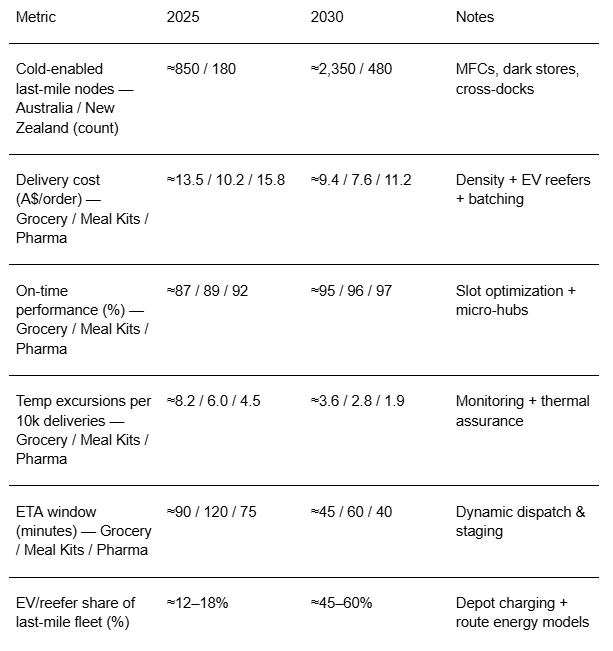

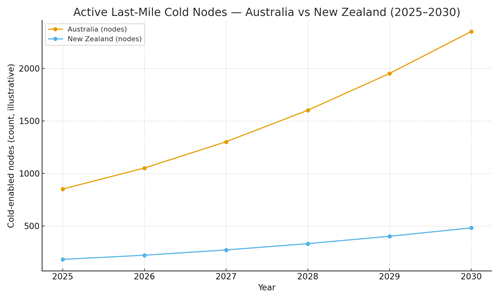

From 2025 to 2030, last‑mile logistics for perishables in ANZ shifts from route‑dense vans and ice packs to data‑driven, temperature‑assured micro‑fulfillment networks. Australia leads with metropolitan dark stores and grocer‑operated micro‑fulfillment centers (MFCs), while New Zealand scales compact nodes aligned to export corridors and population clusters. Winning operators converge robotics‑ready staging, dynamic dispatch, and thermal assurance: pre‑conditioned totes, phase‑change materials, active monitoring, and auto‑exception handling that reroutes or recalls at‑risk orders. Illustratively, cold‑enabled last‑mile nodes in Australia increase from ~850 to ~2,350 between 2025 and 2030; New Zealand grows from ~180 to ~480.

What's Covered?

Report Summary

Key Takeaways

1. Micro‑hubs reduce ETA windows and extend passive cold‑hold viability.

2. Phase‑change materials and pre‑conditioned totes lower energy and excursion risk.

3. EV reefers + dynamic routing cut cost per order and carbon intensity.

4. HACCP‑grade monitoring from dock to door enables automated recalls/reroutes.

5. Meal‑kit and pharma flows benefit from predictable batching and high SLA discipline.

6. Slot pricing & promises must reflect demand density and cold‑hold constraints.

7. Outcome contracts should index to cost/order, on‑time %, and excursions/10k.

8. Change management: train riders/drivers on thermal discipline and exception playbooks.

Key Metrics

Market Size & Share

Demand for rapid, temperature‑assured delivery expands with online grocery penetration, meal‑kit adoption, and direct‑to‑patient pharma. In this illustrative outlook, cold‑enabled last‑mile nodes in Australia grow from ~850 to ~2,350 between 2025 and 2030; New Zealand rises from ~180 to ~480. Share consolidates around metropolitan micro‑hubs (NSW/VIC/QLD) that shrink ETA windows and support passive cold holds. Operators combining grocer MFCs with third‑party dark stores gain density and lower unit costs.

By 2030, market leaders tie micro‑hub placement to demand heatmaps and cold‑hold time models. Their moat is orchestration: aligning inventory, dispatch, and thermal assurance to minimize excursions while keeping cost per order competitive. The rest of ANZ scales through regional nodes linked to export corridors and suburban clusters.

Market Analysis

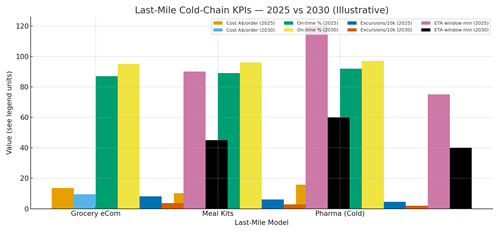

Unit economics improve as density rises and cold assurance becomes programmatic. In this outlook, delivery cost per order falls ~25–35% with micro‑hubs, dynamic batching, and EV reefers; on‑time performance improves ~5–8 pp; temperature excursions drop ~40–60% with continuous monitoring and phase‑change totes; and ETA windows halve through slot optimization. Cost stack: labor/driver time, vehicle energy/lease, packaging/totes, and hub opex. Value stack: fewer refunds/claims, higher repeat rates, and brand trust in pharma and meal‑kit verticals.

Risks: kerbside access constraints, charge scheduling for EVs, thermal discipline at hand‑off, and SLA fragmentation across carriers. Mitigations: city engagement for loading windows, depot charging with opportunity top‑ups, driver training and checklists, and unified SLA dashboards across carriers. Finance will require monthly views on cost/order, on‑time %, excursions/10k, and refund rates.

Trends & Insights (2025–2030)

• Micro‑hubs colocated with MFCs/dark stores compress pick‑to‑dispatch times and enable passive cold holds.

• Phase‑change materials and insulated totes replace single‑use ice packs; pre‑conditioning is scheduled.

• EV reefers and route energy models enable quiet, low‑carbon urban delivery.

• Dock‑to‑door temperature telemetry with exception bots automates recalls and reroutes.

• Slot pricing balances demand with fleet capacity; promises adjust by weather and traffic.

• Pharma direct‑to‑patient flows professionalize packaging, custody logs, and returns.

• Meal‑kit batching and subscription predictability drive pick density and reduce spoilage.

• Shared micro‑hubs extend coverage for smaller brands without the capex burden.

Segment Analysis (Grocery, Meal Kits, Pharma)

• Grocery e‑commerce: high SKU variety; slot‑based delivery; strongest gains from micro‑hubs and EV reefers.

• Meal kits: predictable batching; passive totes and route planning minimize excursions; packaging redesign cuts waste.

• Pharma (cold): strict SLAs; active monitoring and custody logs; reverse logistics for packs and returns.

Buyer guidance: tailor cold solution to distance and category; pre‑condition totes; optimize slot pricing; and codify hand‑off checklists to maintain thermal integrity.

Geography Analysis (ANZ)

Readiness is highest in NSW and VIC due to urban density and carrier capacity; QLD SE benefits from rapid growth and cluster density; WA and SA favor metro corridors with strong food safety regimes; TAS and New Zealand regions focus on export alignment and quality assurance. The stacked criteria urban density, EV/reefer fleet infrastructure, MFC/dark‑store penetration, regulatory/food safety, and carrier capacity indicate where production SLAs can be met first for last‑mile perishables.

Implications: prioritize micro‑hub rollouts in high‑readiness metros; build depot charging and thermal staging; and deploy unified SLA dashboards across carriers and cities.

Competitive Landscape (Platforms & Operating Models)

Stacks converge on: (i) micro‑hub orchestration (inventory, staging, dispatch); (ii) fleet & energy (EV reefers, depot charging, route energy models); (iii) thermal assurance (totes, phase‑change, monitoring); (iv) SLA analytics and exception bots; and (v) compliance (HACCP, food safety, pharma). Differentiators: density management, thermal discipline, energy routing, and SLA auditability. Integrators bundle dark store/MFC ops with carrier networks; brands retain control planes for promise windows and refunds. Contracts trend toward outcome pricing tied to cost per order, on‑time %, excursions/10k, and refunds validated by telemetry and audit trails.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071