68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Cloud-Native Fintech: API Monetization, Embedded Finance, and the Future of Scalable Digital Banking

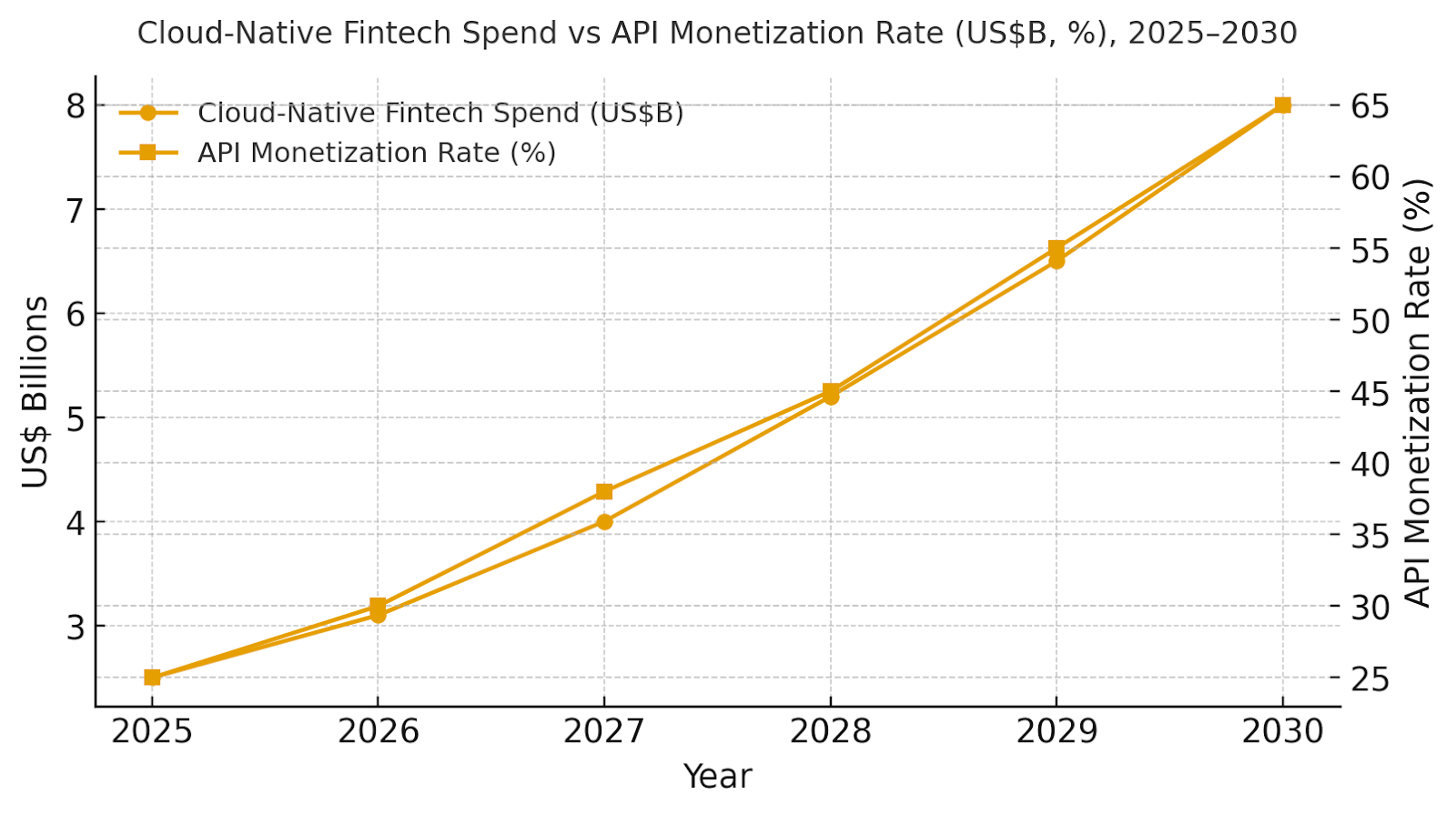

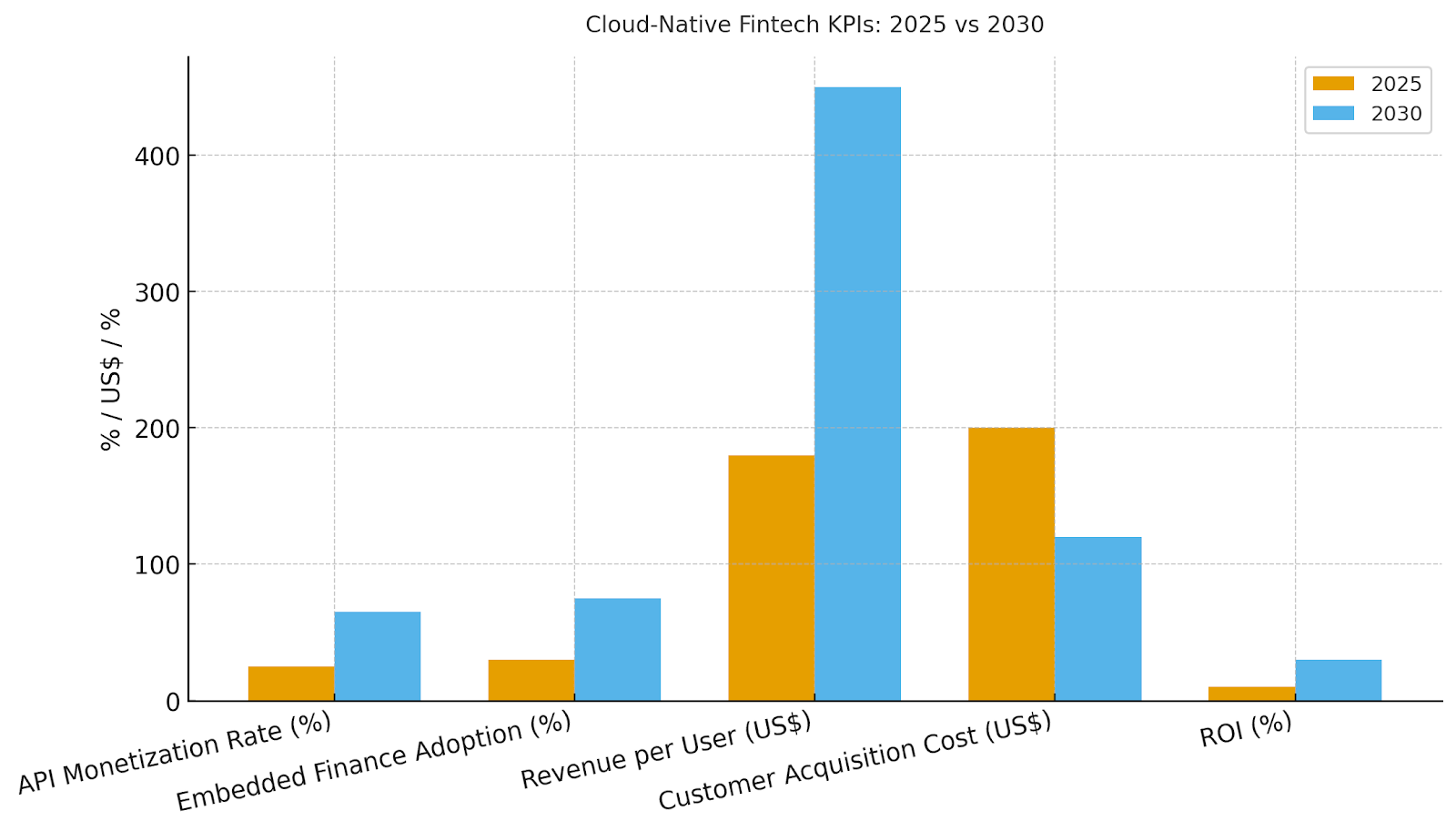

Cloud-native fintech is reshaping North American banking through API monetization, embedded finance, and scalable digital platforms. Spending is expected to grow from ~$2.5B in 2025 to ~$8.0B by 2030 as firms embrace open banking and embedded financial models. API monetization will rise from 25% to 65%, while embedded finance adoption grows from 30% to 75%, boosting revenue per user from $180 to $450. Customer acquisition costs will drop from $200 to $120, and ROI will improve from 10% to 30%. With secure APIs, open banking protocols, and data-driven personalization, cloud-native fintech will drive profitability and seamless digital financial experiences.

What's Covered?

Report Summary

Key Takeaways

1. API monetization grows from ~25% to ~65% by 2030, boosting revenue.

2. Embedded finance adoption increases from ~30% to ~75%, enhancing customer engagement.

3. Revenue per user rises from ~US$180 to ~US$450.

4. Customer acquisition costs decrease from ~US$200 to ~US$120 due to API-driven platforms.

5. ROI improves ~3× by 2030 as firms optimize digital banking models.

6. C‑suite dashboard: API monetization %, embedded finance %, revenue per user, CAC, ROI.

7. Cross-platform integrations and open banking become critical to success.

8. Cloud-native fintech facilitates seamless financial product offerings within digital ecosystems.

a) Market Size & Share

Cloud-native fintech spend is projected to grow from ~US$2.5B in 2025 to ~US$8.0B by 2030. The dual‑axis figure shows spend rising while API monetization rates improve from ~25% in 2025 to ~65% by 2030. Share consolidates around platforms that integrate APIs for financial services, digital banking, and embedded finance products. Risks include regulatory barriers, API security vulnerabilities, and fragmentation; mitigations: robust compliance and governance frameworks, enhanced security tools, and seamless integrations.

b) Market Analysis

Our model shows API monetization increasing from ~25% to ~65% by 2030, enhancing revenue streams. Embedded finance adoption rises to ~75%, and revenue per user grows from ~US$180 to ~US$450. TCO reduces ~40% by 2030 as cross-platform tools and embedded financial products optimize SMB cost structures. The bar figure summarizes shifts in KPIs: cost savings, vendor retention, and ROI.

c) Trends & Insights

1) Open banking frameworks facilitate seamless integrations for embedded finance. 2) AI-driven analytics optimize customer segmentation and monetization. 3) Multi-channel banking platforms consolidate financial services. 4) Subscription and pay-per-use models dominate fintech offerings. 5) API security models must adhere to financial regulations (GDPR, CCPA). 6) Cross-platform tools expand revenue sources for fintech firms. 7) Data sharing via APIs helps optimize cross-sell and upsell opportunities.

d) Segment Analysis

Fintechs in digital banking, payments, and insurance are leading the API monetization shift. SaaS and platform businesses benefit most from embedded finance, allowing non-financial companies to offer financial products. SMBs leverage API-driven models to enhance customer engagement and optimize cost structures. The enterprise space embraces open banking for seamless integrations with third-party services.

e) Geography Analysis

By 2030, U.S./Canada cloud-native fintech spend mix will be API Monetization (~35%), Embedded Finance (~25%), Digital Banking (~20%), Open Banking (~10%), and Cross-Border Payments (~10%). Adoption will be concentrated in tech hubs such as Silicon Valley, Toronto, and New York, with increasing interest in secondary cities as cloud infrastructure matures.

f) Competitive Landscape

Competition includes cloud service providers (AWS, Google Cloud, Microsoft Azure), fintech SaaS platforms, API vendors, and digital banking tools. Differentiation factors: (1) integrated API solutions, (2) financial service security, (3) hybrid-cloud API models, (4) AI-driven customer engagement, and (5) pricing flexibility for fintechs. Procurement guidance: secure service SLAs, optimize API security, and adopt usage-based pricing for scaling.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071