68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Circular Retail Fit-Outs: Modular Design Principles & Carbon Accounting in Fast Fashion

From 2025 to 2030, fast‑fashion retailers in Asia anchored by India shift store build programs from bespoke fit‑outs to modular, circular systems with verified carbon accounting. The architectural stack moves to kit‑of‑parts gondolas, plug‑and‑play MEP, demountable flooring, and standardized fascias that can be reconfigured and reused. Procurement pivots from one‑off capex to product‑as‑a‑service (PaaS) with take‑back, while carbon accounting evolves from estimated bills of materials to supplier‑specific EPDs and audited embodied‑carbon ledgers at m² level. Illustratively, stores with modular/circular fit‑outs in India rise from ~280 in 2025 to ~1,380 by 2030; the rest of Asia scales from ~620 to ~2,350.

What's Covered?

Report Summary

Key Takeaways

1. A standardized kit‑of‑parts unlocks reuse at scale across formats, seasons, and relocations.

2. Carbon accounting must shift to supplier‑specific EPDs and m²‑level ledgers, not generic factors.

3. PaaS and take‑back contracts align incentives for reuse, repair, and reverse logistics.

4. Quick‑connect MEP and demountable flooring compress install time and mall downtime.

5. Digital IDs per module enable redeployment, maintenance SLAs, and warranty governance.

6. Low‑carbon material swaps drive the embodied‑carbon curve downward without sacrificing durability.

7. Design circular‑first: plan disassembly, standard spans, universal fasteners from day one.

8. Outcome‑based vendor fees indexed to reuse %, kgCO₂e/m², and install time scale adoption.

Key Metrics

Market Size & Share

Adoption follows standardized kits and verifiable carbon metrics. In this illustrative outlook, India scales from ~280 modular/circular stores in 2025 to ~1,380 by 2030, while the rest of Asia expands from ~620 to ~2,350. Share concentrates in retailers with centralized engineering and multi‑year supplier frameworks; mall operators accelerate adoption by valuing quick‑install modules that limit downtime.

By 2030, platforms bundling design libraries, supplier‑specific EPDs, module IDs, and carbon MRV lead share capture. India benefits from a deep shopfitting supply base and refurbishment hubs near logistics nodes.

Market Analysis

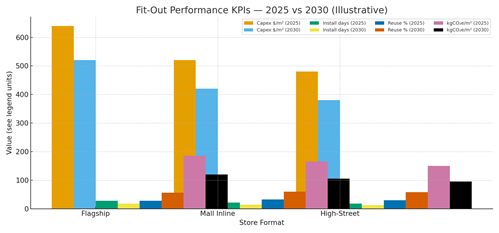

Economics hinge on reuse, quick‑connects, and low‑carbon materials. In this outlook, capex per m² declines ~18–25%; install time drops ~30–40%; reusable content doubles; and embodied carbon falls ~35–40% as modules and EPD‑backed materials replace high‑carbon equivalents. Cost stack spans manufacturing, logistics/refurb, installation, and downtime. Value stack: faster openings, lower embodied carbon, and residual module value via PaaS.

Risks include QA drift in local materials, lease restrictions on demountables, inconsistent EPD quality, and reverse‑logistics gaps. Mitigations: supplier audits, landlord quick‑connect templates, standardized spans/fasteners, and refurbishment partners with test/cert protocols. Finance will require ledgers for m² carbon, reuse %, and module utilization to validate ROI.

Trends & Insights (2025–2030)

• Mature kit‑of‑parts libraries with interchangeable gondolas, fascias, lighting rails.

• Product‑as‑a‑service with deposits ensures take‑back and redeployment.

• Carbon ledgers integrate supplier‑specific EPDs for m² reporting.

• Digital IDs (QR/RFID) track service history and warranty per module.

• Quick‑connect MEP becomes landlord‑standard, shrinking downtime.

• Engineered wood/recycled metals swap in for gypsum/virgin steel where code allows.

• Refurbishment hubs re‑certify modules for secondary use.

• Outcome‑based contracts tie fees to reuse %, kgCO₂e/m², and install time.

Segment Analysis (Formats & Lifecycles)

• Flagships: complex designs; modular sub‑assemblies & premium finishes; reuse governed by strict QA.

• Mall Inline: standardized spans; strong candidates for PaaS and quick‑connect MEP.

• High‑Street: frequent refreshes; rugged modules and easy redeploy yield highest ROI.

Lifecycle guidance: plan for disassembly, repair kits, refurbishment checkpoints; track module utilization and residual value; and set thresholds for reuse vs remanufacture vs recycle.

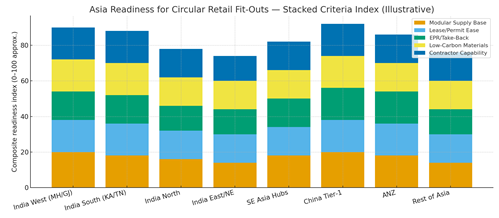

Geography Analysis (Asia & India)

Readiness clusters in India West (MH/GJ) and South (KA/TN) with dense supply chains; North grows with mall pipelines; East/NE needs logistics and refurb hubs. SE Asia hubs and China Tier‑1 combine material access with permitting speed; ANZ sets compliance benchmarks. The stacked criteria—modular supply base, lease/permit ease, EPR/take‑back norms, low‑carbon materials, contractor capability indicate where production SLAs can be met first.

Implications: prioritize high‑readiness clusters; sign PaaS/take‑back contracts with deposits; place refurb hubs near logistics nodes; and standardize carbon and QA reporting for scale.

Competitive Landscape (Vendors & Operating Models)

Stacks converge on: (i) design libraries & standards; (ii) module manufacturing with EPD‑backed materials; (iii) digital IDs & carbon ledgers; (iv) refurb hubs; and (v) PaaS/take‑back contracting. Differentiators: reuse % at scale, install speed, embodied‑carbon intensity, QA consistency, and MRV quality. System integrators bundle design, supply, install, refurb under SLAs; retailers retain a control plane for standards and carbon accounting. Contracts trend toward outcome pricing indexed to reuse %, kgCO₂e/m², install time, and uptime validated via audited ledgers and inspections.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071