68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Circular Fashion Tech Hubs: Chemical Recycling Systems & EPR Compliance in European Apparel

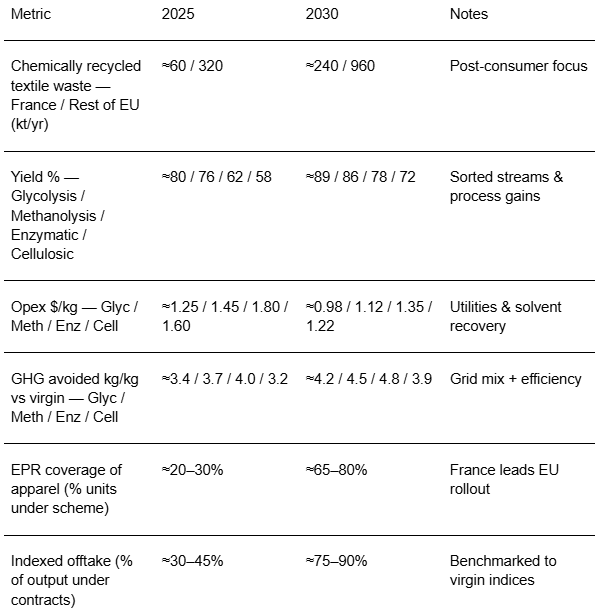

From 2025 to 2030, Europe’s circular fashion push shifts from pilot lines to scaled chemical recycling hubs integrated with Extended Producer Responsibility (EPR) systems. France emerges as a flagship market: national EPR frameworks accelerate formal collection, standardized sorting, and indexed offtake contracts between recyclers, mills, and brands. Tech portfolios converge on PET depolymerization (glycolysis, methanolysis), enzymatic PET for low‑temperature flows, and cellulosic dissolution routes for poly‑cotton blends. Winning operators separate feedstock aggregation from plant operations and lock multi‑year, indexed offtake tied to virgin benchmarks. Illustratively, chemically recycled post‑consumer textile tonnage rises in France from ~60 kt (2025) to ~240 kt (2030), and across the rest of Europe from ~320 kt to ~960 kt.

What's Covered?

Report Summary

Key Takeaways

1. Tech hubs thrive where EPR aligns feedstock quality, plant utilization, and brand offtake.

2. Run a portfolio: PET depoly (glycolysis/methanolysis), enzymatic PET for low‑temp streams, and cellulosic dissolution for blends.

3. Indexed, multi‑year offtake contracts de‑risk finance and stabilize pricing vs virgin volatility.

4. Mass‑balance + MRV for GHG are mandatory for brand claims and green finance eligibility.

5. Utilities integration (heat, water, solvent loops) is as material to opex as chemistry choice.

6. France is a launchpad: dense brands, strong EPR, and logistics make steady‑state utilization achievable.

7. Worker safety and solvent management are gating: ZDHC/REACH alignment is non‑negotiable.

8. Outcome‑based vendor fees indexed to tons processed, yield, and recycled content delivery will scale programs.

Key Metrics

Market Size & Share

France and leading EU markets translate EPR coverage into predictable feedstock for chemical recycling hubs. In this illustrative outlook, France’s chemically recycled post‑consumer tonnage grows from ~60 kt in 2025 to ~240 kt in 2030; the rest of Europe from ~320 kt to ~960 kt. Share accrues to hubs that combine dense collection (EPR schemes, retailer take‑back), upgraded MRFs, and short‑haul logistics to plants. Operators with multi‑tenant lines and strong offtake to mills/brands gain utilization and price stability.

By 2030, market leadership skews toward platforms bundling feedstock aggregation, modular chemistry trains, and MRV‑ready mass‑balance. France’s advantage: early EPR maturity, brand density, and transport links that compress cycle times from collection to processing.

Market Analysis

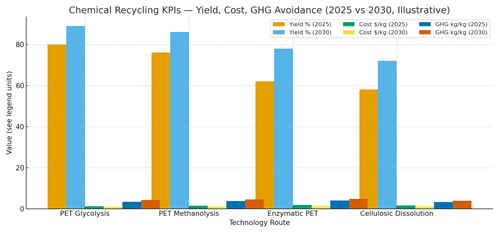

Performance deltas are driven by feedstock quality and utilities integration. In this outlook, PET depolymerization yields rise to ~86–89% with cleaner streams and optimized catalysts; enzymatic PET approaches ~78% on sorted flows; and cellulosic dissolution for blends improves to ~72% with solvent recovery and pulp stabilization. Opex falls 15–30% through heat integration, solvent loops, and higher capacity factors; GHG avoidance rises across all routes vs virgin. Cost stack is dominated by feedstock logistics (25–35%), energy/chemicals (30–40%), and labor/overheads (10–15%). Value creation comes from recycled content claims, EPR compliance credits, and long‑term offtake premiums tied to quality.

Risks: contamination, solvent management, energy price volatility, and MRV credibility. Mitigations: standardized sorting specs and incentives; closed‑loop solvents and ZDHC/REACH compliance; PPAs or hedges; and third‑party‑audited mass‑balance/GHG factors. Finance teams will require monthly dashboards for yield, opex, uptime, and offtake utilization to validate payback.

Trends & Insights (2025–2030)

• EPR expansion raises collection quality and volumes; bag/tag digitalization improves traceability and payments.

• Modular chemistry trains allow PET, enzymatic, and cellulosic lines to flex with feedstock mixes.

• MRV for mass‑balance and GHG becomes a financing requirement; auditors standardize factor libraries.

• Utilities integration (heat/water/solvent) is a core differentiator for opex and permits.

• Brand offtake shifts to indexed contracts with quality gates; premiums reflect virgin volatility.

• Informal collection interfaces are codified via PROs with safety and fair‑pay provisions.

• EU eco‑design and DPP (product passports) tie recycling evidence to SKU‑level claims and resale.

• Outcome‑based contracts link fees to tons processed, yield, and recycled content delivery.

Segment Analysis (Feedstock & Output)

• PET‑dominant streams: target depolymerization to PTA/MEG/BHET; feed rPET pellets/filament.

• Low‑temp flows: enzymatic PET for delicate or color‑sensitive inputs; lower energy intensity.

• Poly‑cotton blends: cellulosic dissolution to pulp for viscose/lyocell; PET recovered to rPET.

• Dark/contaminated: pre‑treatment and, if needed, downcycling/energy recovery under strict emissions.

Buyer guidance: map feedstock to tech routes; deploy modular lines; secure indexed offtake; and instrument MRV from day one for brand claims and financing.

Geography Analysis (Europe & France)

Readiness hotspots include France, Germany, and Italy each combining brand density, logistics, and policy momentum. Spain and Benelux ramp with EPR maturation and port access; Nordics lead in utilities integration and compliance; CEE scales with industrial parks and labor availability; UK/Ireland maintain strong brand offtake. The stacked criteria feedstock access, installed/planned plants, EPR/policy readiness, utilities/permitting, and brand offtake indicate where production SLAs can be met first for chemical recycling hubs.

Implications: stage build‑outs where EPR and plant pipelines are robust (France/DE/IT); secure PPAs or hedges; standardize sorting specs; and publish audit‑ready MRV to unlock finance.

Competitive Landscape (Platforms & Operating Models)

Stacks converge on: (i) feedstock aggregation via PROs and retailer take‑back; (ii) tiered sorting and pre‑treatments; (iii) modular chemical lines (glycolysis, methanolysis, enzymatic, cellulosic) with shared utilities; (iv) MRV/mass‑balance platforms; and (v) indexed offtake contracting. Differentiators: yield on mixed streams, solvent/water safety, utilities integration, and audit‑ready MRV. System integrators bundle city collection upgrades; plant operators optimize multi‑tenant capacity; brands underwrite offtake with indexed contracts. Contracts trend toward outcome pricing tied to tons processed, yield, recycled content delivery, and GHG factors—under ZDHC/REACH compliance and third‑party audits.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071