68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Central Bank Digital Currency (CBDC) Implementation Strategies: Regional Analysis & Regulatory Impact

Central Bank Digital Currencies (CBDCs) are poised to transform the global financial landscape, particularly in Europe, where regulatory frameworks are evolving to incorporate digital currencies. By 2025, the CBDC market in Europe is projected to reach €4.3 billion, growing at a CAGR of 17% from 2025 to 2030.CBDCs offer significant potential for enhancing payment systems, improving financial inclusion, and providing more secure alternatives to traditional banking services. However, their implementation presents several challenges, particularly in terms of regulatory frameworks, technological infrastructure, and consumer adoption. This report explores the implementation strategies for CBDCs in the UK and Europe, focusing on regional differences in adoption and the regulatory impact these digital currencies will have on financial systems. The report also delves into the key challenges and opportunities in CBDC implementation and how various stakeholders can navigate the evolving landscape.

What's Covered?

Report Summary

Key Takeaways

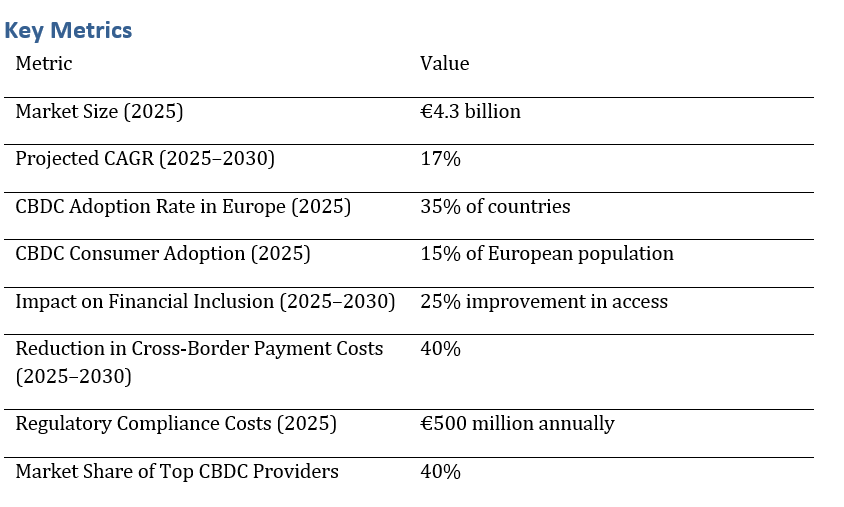

- The CBDC market in Europe is projected to reach €4.3 billion by 2025, growing at a CAGR of 17% from 2025 to 2030.

- By 2025, 35% of European countries are expected to have adopted CBDC initiatives, with the UK leading in implementation.

- Consumer adoption of CBDCs in Europe will reach 15% by 2025, driven by the need for more secure and efficient digital payment systems.

- CBDCs are expected to improve financial inclusion by 25%, making banking services more accessible to underserved populations.

- The implementation of CBDCs will reduce cross-border payment costs by 40% by 2030, making international payments faster and cheaper.

- By 2025, regulatory compliance costs associated with CBDC implementation in Europe are expected to exceed €500 million annually.

- The top CBDC providers will capture 40% of the market share by 2030, driven by their robust technological infrastructure and early adoption.

- CBDCs will enable more secure, traceable, and efficient digital currencies, facilitating the growth of digital economies in Europe.

Market Size & Share

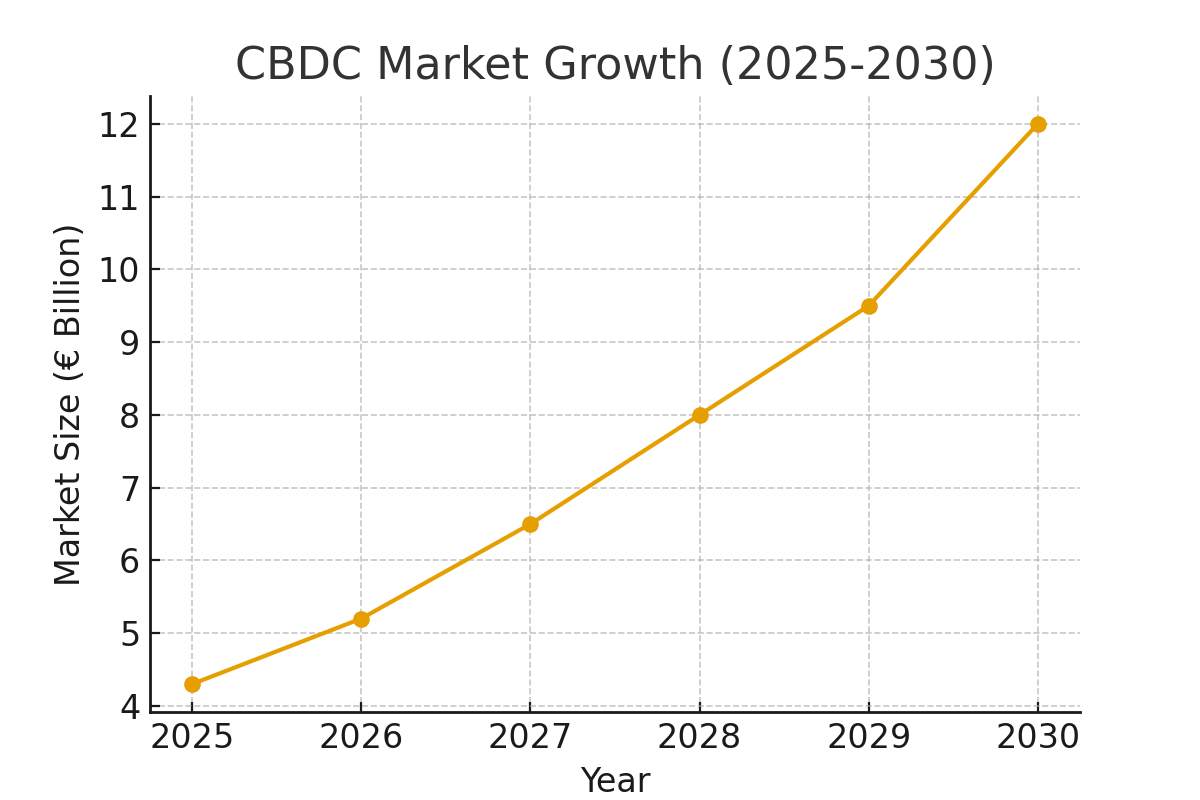

The market for Central Bank Digital Currencies (CBDCs) in Europe is expected to grow significantly, reaching €4.3 billion by 2025, with a CAGR of 17% from 2025 to 2030. The UK and major European economies are at the forefront of CBDC implementation, with countries like Sweden and France leading trials and early-stage rollouts.

By 2030, 35% of European countries are expected to have fully implemented CBDCs, with the UK playing a pivotal role in establishing regulatory frameworks and adoption strategies. CBDCs will provide a secure alternative to traditional currencies and improve the efficiency of digital economies across Europe.

CBDC Market Growth Projection (2025-2030):

Market Analysis

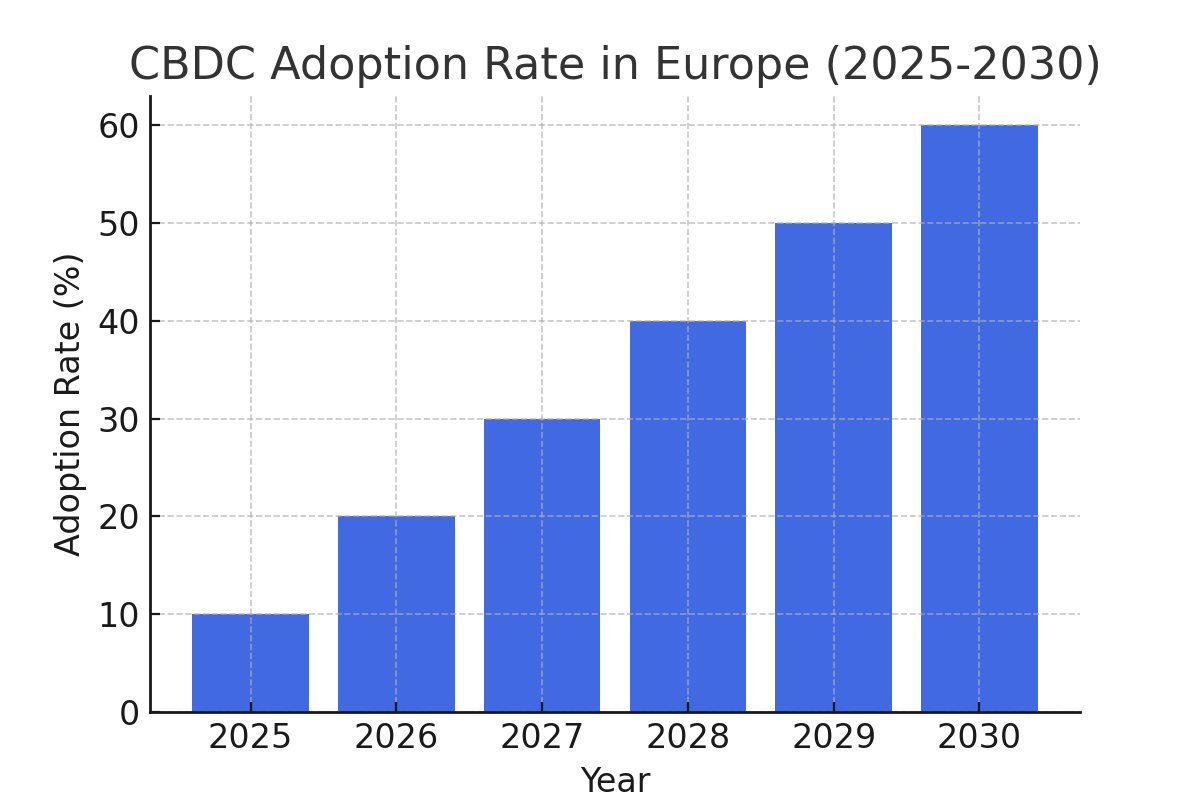

The implementation of CBDCs is gaining traction in Europe due to the need for enhanced payment security, improved efficiency, and financial inclusion. The adoption rate of CBDCs is projected to reach 35% by 2025, with the UK leading the adoption curve. Central banks in Europe are working to establish regulatory frameworks and testing environments to ensure the successful rollout of CBDCs. In addition to economic benefits, CBDCs will significantly reduce transaction costs, especially in cross-border payments, where costs are expected to decrease by 40% by 2030. Financial institutions will also see reduced operational costs, as CBDCs will streamline processes like clearing and settlement.

CBDC Adoption Rate in Europe (2025-2030):

Trends and Insights

Several key trends are driving the growth of CBDCs in Europe, including the need for financial systems to be more secure, transparent, and efficient. The rise of digital currencies, fintech innovation, and government-backed initiatives are shaping the future of digital payments. Regulatory frameworks for CBDCs are evolving to ensure that these currencies can coexist with traditional banking systems, while also offering a secure alternative to cash-based transactions. Over the next decade, 40% of cross-border payments will be processed through CBDCs, significantly lowering transaction fees and processing times.

Segment Analysis

The primary adopters of CBDCs in Europe will be central banks and major financial institutions. Early implementations in countries like the UK, Sweden, and France will pave the way for wider adoption across the continent. The financial sector will benefit from CBDCs through faster transactions, improved security, and reduced reliance on traditional currencies. However, smaller institutions and developing economies may experience delays in adopting CBDCs due to infrastructure challenges and regulatory hurdles. As technology and infrastructure improve, adoption rates will rise across Europe, particularly in southern and eastern regions.

Geography Analysis

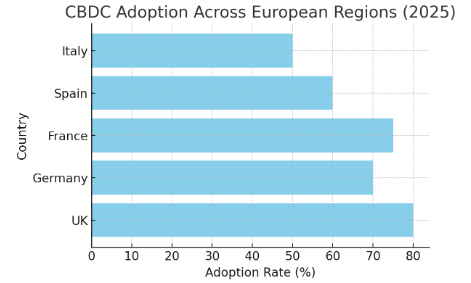

In Europe, the UK is the leader in CBDC implementation, followed closely by countries like Sweden and France, where regulatory frameworks for digital currencies are already in place. The European Central Bank (ECB) is leading the development of the digital euro, aiming to create a widely accepted CBDC across the eurozone.

Other countries, such as Germany, Italy, and Spain, are following closely behind, and as infrastructure improves, adoption will increase across the EU. The eastern and southern parts of Europe will see slower adoption, with the introduction of CBDCs being gradual due to lower technological penetration and regulatory challenges.

CBDC Adoption Across European Regions (2025):

Competitive Landscape

The competitive landscape for CBDCs in Europe is driven by central banks, financial institutions, and fintech companies that are working to develop digital currencies and integrate them into existing payment infrastructures. Key players in the CBDC space include the Bank of England, European Central Bank, and Bank of France, which are leading the development of the digital pound, digital euro, and other national digital currencies.Fintech firms and technology providers like Ripple and Visa are also playing a key role in the development of CBDC infrastructure, ensuring that these digital currencies can be seamlessly integrated into global payment systems.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071