68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

BNPL Regulatory Compliance in India: RBI Guidelines & Tier-3 City Penetration Strategies

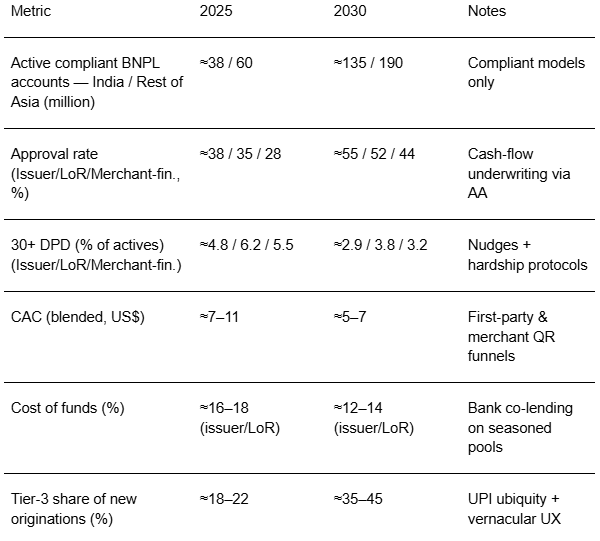

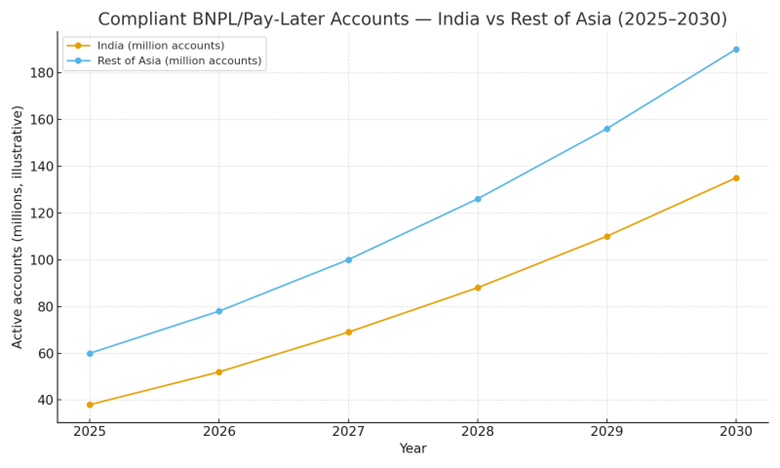

From 2025 to 2030, India’s BNPL market evolves from growth-at-all-costs to prudentially compliant, partner-led models aligned with RBI expectations. The operating stack consolidates around four pillars: (1) compliant onboarding (CKYC/eKYC, Aadhar/OTP with consent, bureau checks, and Account Aggregator cash-flow underwriting); (2) lender-of-record structures with transparent risk retention and capital rules; (3) repayments over UPI/autopay with clear chargeback and disclosures; and (4) governance—fair lending, data minimization, and collections codes of conduct. Issuer-led pay-later variants on card rails expand as interchange economics stabilize, while merchant-financed invoice BNPL grows in durable goods and online travel where ticket sizes justify costs. Illustratively, active compliant BNPL accounts in India rise from ~38m (2025) to ~135m by 2030, with the rest of Asia growing from ~60m to ~190m.

What's Covered?

Report Summary

Key Takeaways

1. RBI‑aligned lender‑of‑record and issuer‑led structures dominate; FLDG and PPI usage must follow caps and disclosure norms.

2. Cashflow underwriting via Account Aggregator materially lifts approval while containing risk.

3. UPI autopay + repayment nudges reduce delinquency; hardship/settlement protocols protect NPA optics.

4. Data minimization, consent, and purpose‑limitation are essential delete what you don’t need.

5. Tier‑3 growth depends on vernacular UX, assisted onboarding, and offline merchant QR funnels.

6. Collections must be local and ethical—no harassment; rely on digital reminders and structured field ops.

7. Co‑lending and securitization for seasoned books compress cost of funds and stabilize unit economics.

8. Finance‑grade dashboards with causal tests (geo/A‑B) are required to unlock bank partnerships.

Key Metrics

Market Size & Share

BNPL’s addressable base expands as compliant models replace aggressive, fee‑heavy variants. In this illustrative outlook, active compliant accounts in India grow from ~38m (2025) to ~135m (2030), while the rest of Asia rises from ~60m to ~190m. India’s share increases in categories where UPI at checkout and embedded BNPL in marketplaces lower friction for small‑ticket purchases. Share concentrates among providers that pair bank balance‑sheet partners with strong risk controls and merchant integrations that expose installment options contextually across PDP/checkout and QR flows.

By 2030, issuer‑led and bank‑partnered LoR constructs dominate volume; merchant‑financed BNPL scales in durables/travel where gross margins can fund discounts. Providers with 1) product‑graph‑level merchant data, 2) AA‑enabled cash‑flow views, and 3) transparent disclosures capture a disproportionate share of Tier‑3 growth.

Market Analysis

Unit economics improve as governance hardens. In this outlook, approval rates rise 12–17 pp across models with cash‑flow insights; 30+ DPD drops 2–3 pp with UPI autopay and standardized nudges; CAC falls via first‑party channels (bank apps, OEM partners); and cost of funds compresses as banks co‑lend into seasoned pools. Cost drivers include AA integrations, bureau pulls, consent orchestration, collections ops, and dispute resolution. Benefits include higher quality originations, lower fraud, and more stable credit losses—enabling expansion into Tier‑3 without sacrificing risk appetite.

Risks: policy slippage on disclosures or FLDG, data‑privacy violations, over‑reliance on device signals, and aggressive collections. Mitigations: policy engines mapped to RBI rules, consent logs, model monitoring, and ethical collections with audit trails. Finance will demand cohort views (vintage curves, roll rates) and causal tests before committing capital at scale.

Trends & Insights (2025–2030)

• Account Aggregator becomes default for cash‑flow underwriting; thin‑file consumers gain via consented data.

• Embedded BNPL in marketplaces and OEM flows replaces standalone apps; merchant QR funnels grow in Tier‑3.

• UPI autopay and repayment reminders become table stakes; collections shift to respectful, localized ops.

• Privacy‑by‑design: purpose limitation, retention caps, encryption, and user dashboards for consent revocation.

• Co‑lending frameworks and seasoned-pool securitizations lower cost of funds and diversify capital.

• Analytics standardize on finance‑grade cohorts: vintages, roll rates, ECL, and AA‑driven approval lift.

• Vernacular UX and WhatsApp onboarding drive adoption beyond metros; assisted journeys reduce drop‑offs.

• Outcome‑based vendor contracts tie fees to approval lift, DPD reduction, and CAC efficiency.

Segment Analysis (Categories & Ticket Sizes)

• Fashion/Beauty (low‑ticket, high frequency): approval led by device + AA cash‑flow; strongest Tier‑3 adoption via QR.

• Electronics (mid‑ticket): issuer‑led and LoR BNPL; OEM partnerships enable instant EMI; risk screened by bureau + AA.

• Travel (mid/high‑ticket): merchant‑financed installments, higher margins; requires robust cancellations/refunds policy.

• Durables/Furniture (high‑ticket): longer tenors, tighter KYC, field verification in Tier‑3.

Buyer guidance: align model to ticket size and margins; codify disclosures; optimize repayment rails; and track cohorts.

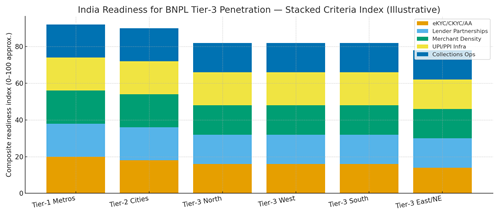

Geography Analysis (India — Tier‑3 Focus)

Readiness is highest in metros and Tier‑2 today but Tier‑3 potential is significant where UPI penetration and merchant QR are ubiquitous. North and West Tier‑3 clusters benefit from commerce corridors and NBFC presence; South shows strong repayment discipline and digital adoption; East/NE requires deeper agent networks and vernacular support. The stacked criteria eKYC/CKYC/AA enablement, lender partnerships, merchant density, UPI/PPI infrastructure, and collections operations—indicate where production SLAs can be met first.

Implications: phase penetration by readiness; deploy assisted onboarding and WhatsApp flows; localize collections; and run geo/A‑B on credit policy to balance approval and risk.

Competitive Landscape (Operating Models & Partners)

Winning stacks integrate: (i) onboarding & consent (CKYC/eKYC + AA); (ii) underwriting (AA + bureau + device); (iii) rails (UPI autopay/cards/PPIs) with dispute handling; (iv) collections/CRM with ethics guardrails; and (v) finance‑grade analytics for cohorts and ECL. Differentiators: bank/NBFC depth, merchant integrations, policy engines mapped to RBI, cost of funds, and Tier‑3 distribution. System integrators serve onboarding and collections; lenders provide balance sheets, fintechs orchestrate UX and analytics. Contracts trend toward outcome pricing indexed to approval lift, DPD reductions, CAC, and portfolio yield subject to compliance audits and consent telemetry.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071