68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Blockchain in CPG Supply Chains: Traceability Solutions & Regulatory Compliance Frameworks

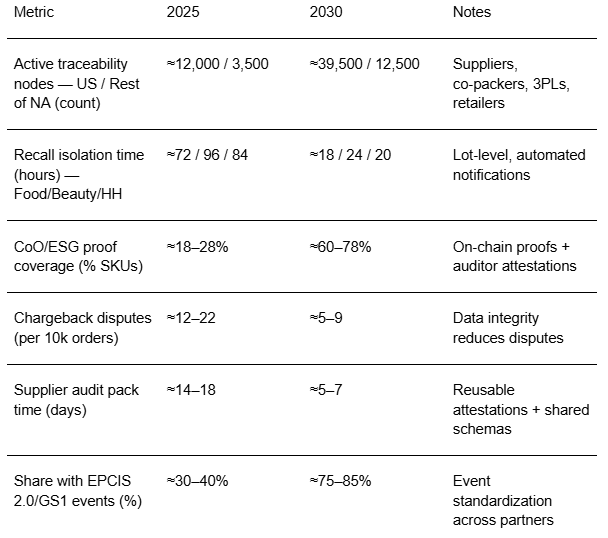

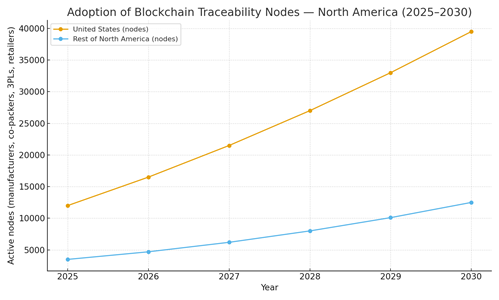

Between 2025 and 2030, blockchain evolves from pilot provenance projects into production‑grade traceability rails across North American CPG. The winning architectures are pragmatic: permissioned ledgers or verifiable data registries that anchor cryptographic proofs of origin, custody, temperature, and sustainability—while raw operational data lives off‑chain in systems of record. Smart‑contract logic enforces data completeness (lot, batch, CoA), SLA thresholds (cold‑chain excursions), and third‑party attestations (organic, fair‑trade), issuing tokens or badges that flow through EDI/ASNs to retail. Quantitatively, this illustrative outlook shows active US traceability nodes growing from ~12k in 2025 to ~39.5k by 2030; the rest of North America from ~3.5k to ~12.5k.

What's Covered?

Report Summary

Key Takeaways

1. Value compounds with partner density—prioritize top suppliers and 3PLs for phase‑1 onboarding.

2. Anchor proofs on‑chain; keep bulk data off‑chain—optimize for privacy, cost, and performance.

3. EPCIS 2.0 + GS1 IDs unify events; avoid bespoke schemas that stall network effects.

4. IoT telemetry (temp/shock) hashed to chain enables SLA enforcement and insurance benefits.

5. Selective disclosure/zero‑knowledge proofs protect sensitive supplier data while proving compliance.

6. Map controls to FSMA 204, UFLPA, EPR, California SB‑343—automate evidence collection.

7. Dispute resolution improves with tamper‑evident histories and signed hand‑offs.

8. Outcome‑based contracts indexed to recall time, dispute rate, and audit cycle time win budget.

Key Metrics

Market Size & Share

Network scale defines market share in traceability. In this illustrative view, active US nodes expand from ~12k in 2025 to ~39.5k by 2030, while the rest of North America grows from ~3.5k to ~12.5k as retailers mandate EPCIS 2.0 event exchange and suppliers standardize IDs and lot coding. Food & Beverage leads adoption under FSMA 204 recordkeeping and cold‑chain risk; Beauty follows driven by claims and ingredient provenance; Household categories add gradually through 3PL consolidation. Vendors that bundle data connectors, identity (DIDs), and rules engines for recalls and attestations capture share as they shorten partner onboarding cycles.

By 2030, the market consolidates around permissioned networks with verifiable receipts and bridges to public registries for consumer‑facing trust marks. The moat becomes referenceable partners, schema depth, and performance at scale not speculative tokens. Buyers prioritize providers that interoperate with WMS/ERP and retailer portals while exposing granular evidence to regulators and auditors.

Market Analysis

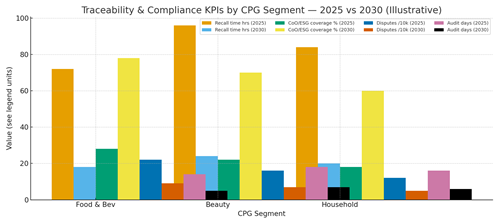

Traceability ROI shows up in recall speed, dispute reduction, and audit efficiency. In this outlook, lot isolation shrinks from days to hours as EPCIS events and IoT telemetry surface excursions promptly. CoO/ESG proofs expand to majority SKU coverage, enabling marketing claims with auditable evidence. Disputes per 10k orders fall by ~50–60% as custody and label data become tamper‑evident. Audit packs compress to a week thanks to reusable attestations and shared schemas. Cost drivers include partner integration, IoT sensors, and identity/key management; benefits include avoided recall losses, lower chargebacks, fewer deductions, and stronger brand trust.

Risks: supplier resistance and data‑sharing concerns; inconsistent event quality; IoT calibration drift; and privacy exposure. Mitigations: selective disclosure with cryptographic proofs; data contracts and conformance tests; device QA and calibration logs; and least‑privilege access tied to roles. Finance requires a baseline of recall costs and dispute rates to validate payback over 18–30 months.

Trends & Insights (2025–2030)

• EPCIS 2.0 adoption standardizes event semantics across partners, unlocking cross‑network analytics.

• Verifiable credentials and DIDs let suppliers prove compliance without revealing sensitive pricing or recipes.

• Zero‑knowledge proofs (ZKPs) emerge for UFLPA and CO2 content attestations with selective disclosure.

• IoT‑anchored cold‑chain data (temp, humidity, shock) reduces insurance premiums and recalls.

• Consumer trust marks link public registries to on‑pack QR, surfacing batch‑level provenance.

• Data clean rooms enable retailer‑brand collaboration on demand/quality signals without raw data sharing.

• SMB onboarding accelerates via light clients, email‑to‑EPCIS, and managed integration services.

• Outcome‑based contracts index fees to recall time cuts, dispute reductions, and audit‑cycle compression.

Segment Analysis

• Food & Beverage: FSMA 204 drives lot‑level traceability and cold‑chain telemetry; high ROI from recall risk reduction.

• Beauty & Personal Care: ingredient provenance and claims substantiation (vegan, cruelty‑free); packaging EPR data.

• Household & Durables: gradual adoption through 3PL integrations; focus on authenticity and warranty workflows.

• Private Label: retailer‑led mandates accelerate onboarding; unified schemas across suppliers cut audit time.

Buyer guidance: start with high‑risk/high‑volume SKUs; lock EPCIS/GS1 alignment; pilot ZK proof workflows for sensitive attestations; and instrument finance‑grade telemetry for recall time, disputes, and audit hours.

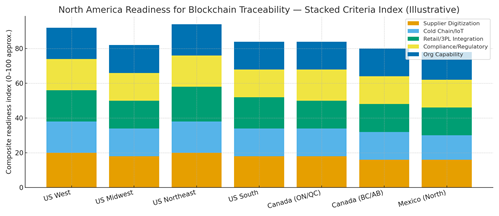

Geography Analysis (North America)

Readiness clusters in the US Northeast and West, where retailer mandates, supplier digitization, and IoT cold‑chain coverage are strongest; the South and Midwest accelerate via manufacturing corridors and 3PL hubs. Ontario/Quebec benefit from governance and retailer networks; Western Canada and Northern Mexico expand through cross‑border food flows. The stacked criteria supplier digitization, cold chain/IoT, retail/3PL integration, compliance/regulatory, and organizational capability—indicate where production SLAs can be met first.

Implications: stage deployments in high‑readiness regions; negotiate data contracts with top suppliers/3PLs; implement selective disclosure and ZKPs early for sensitive attestations; and codify audit trails to satisfy regulators and retailer portals.

Competitive Landscape (Platforms & Operating Models)

Stacks converge on five layers: (i) data capture/connectors (ERP/WMS/PLM/EDI), (ii) event standardization (EPCIS 2.0/GS1), (iii) ledger/registry with verifiable receipts, (iv) compliance & rules engines for recalls/attestations, and (v) analytics and trust‑mark portals. Differentiators: partner network density, EPCIS conformance tooling, ZKP support, IoT integrations, and auditability. System integrators bundle onboarding and managed services for SMBs; enterprises retain control planes and deploy multi‑ledger or registry bridges. Contracting trends favor outcome‑indexed fees tied to recall hours saved, disputes avoided, and audit time reduced, with SLAs on data integrity, latency, and availability.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071