68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Blockchain for Drug Traceability: Anti-Counterfeiting Solutions & ROI Analysis - Technological Advancements

This report quantifies blockchain-enabled pharmaceutical traceability across Saudi Arabia and the Middle East (2025–2030), focusing on anti-counterfeiting outcomes, compliance, and ROI. We model end-to-end serialization (GTIN/SGTIN/aggregations), mobile verification at point of dispense, and cold-chain integrity via IoT oracles. Benchmarks include counterfeit incidence reduction, recall cycle times, scan events per pack, dispenser adoption, and payback periods. Findings show blockchain networks deliver measurable risk reduction, operational savings, and revenue protection, enabling ministries, MAHs, wholesalers, and pharmacies to meet regulatory mandates while improving public trust.

What's Covered?

Report Summary

Key Takeaways

- MEA blockchain traceability spend grows $140M (2025) → $520M (2030); CAGR 30%.

- Counterfeit incidence in targeted SKUs falls 55–70% within 24 months of go-live.

- Regulatory compliance (serialization + verification) reaches 88% of Rx volume by 2030.

- Recall time-to-notify drops from 48h → 9h (−81%); time-to-complete 12 days → 3.5 days (−71%).

- Cold-chain excursions per 1,000 shipments fall 40% with IoT → blockchain provenance.

- Pharmacy/dispenser participation reaches 75% of outlets; patient scan adoption 22–28%.

- Chargeback/returns disputes reduced 45% via shared ledger evidence.

- Revenue protection equals 0.6–1.0% of in-market sales for high-risk categories.

- Operating cost per serialized pack falls 34% post-year-2 through automation.

- Typical ROI 18–26%; payback 18–30 months, best for biologics/vaccines.

Key ,Metrics

Market Size & Share

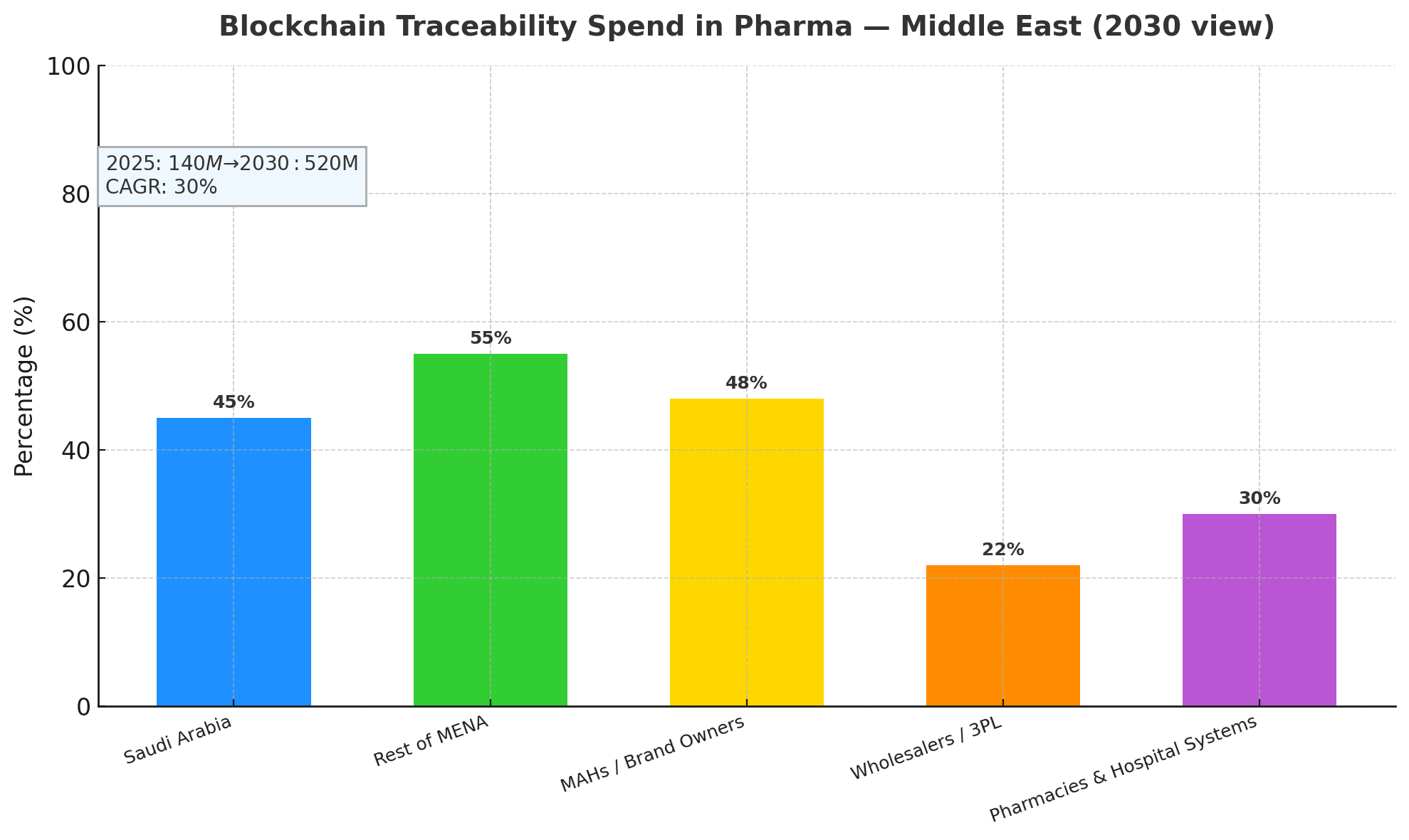

Between 2025 and 2030, Saudi Arabia and the Middle East will scale blockchain traceability spend from $140M to $520M (CAGR 30%), anchored by national serialization mandates, tender requirements, and payer pressure to curb falsified medicines. Saudi Arabia will represent roughly 45% of regional spend by 2030, with the remaining 55% across UAE, Qatar, Kuwait, Oman, Bahrain, and early adopters in Jordan and Egypt for export lanes. On value capture, MAHs/brand owners account for ~48% of solution spend (line upgrades, L3/L4 integration, network fees), wholesalers/3PLs ~22% (aggregation, warehouse verification, reverse-logistics), and pharmacies/hospital systems ~30% (POS verification, mobile scanning, patient engagement). In high-risk categories—biologics, oncology, specialty injectables—counterfeit incidence declines 55–70% within 24 months as authentication and channel visibility increase. Recall cycle time compresses (notify 48h → 9h, complete 12 days → 3.5 days), reducing patient exposure and write-offs. Cold-chain excursions reduce 40% when IoT sensors (temperature, shock, light) stream events to the ledger and trigger exception workflows. By 2030, 88% of Rx volume is expected to be traceability-compliant, with 75% dispenser participation and 22–28% patient scan adoption at dispense. Operating cost per serialized pack falls 34% after year-2 via automated EPCIS events and exception handling. Aggregate ROI 18–26% stems from revenue protection (0.6–1.0% of sales), lower recall/logistics costs, and dispute avoidance, making blockchain networks a regional standard for pharmaceutical assurance.

Market Analysis

Adoption economics in the Middle East hinge on five levers. (1) Compliance & enforcement: Ministries set phased thresholds for unit-level verification at wholesaler and pharmacy, driving 88% Rx coverage by 2030. (2) Network effects: As dispenser participation hits 75%, duplicate serial detection and diversion analytics improve, cutting counterfeit incidence 55–70% in targeted SKUs. (3) Automation: Integrating L3/L4/L5 (site/enterprise/network) reduces manual EPCIS reconciliation; OpEx/pack −34% by year-2 as exception queues shrink. (4) Cold-chain proofs: IoT data to smart contracts automates quarantine/release, lowering excursions 40% and recall wastage 18–22%. (5) Commercial disputes: A single source of truth trims chargeback/returns disputes −45%, with average dispute cycle time falling 21 days → 8 days. Typical CapEx for a mid-size MAH: $1.8–2.6M (line printers/cameras, aggregators, L3 server, connectors), plus annual network fees $250–500k depending on volumes; wholesalers invest $0.6–1.1M for aggregation, handheld verifiers, and WMS adapters; a 1,000-outlet chain invests $0.9–1.4M in POS scanners, app enablement, and staff upskilling. Benefit stack: revenue protection 0.6–1.0% of sales in high-risk SKUs, recall cost −45%, returns write-off −20%, admin labor −18%, premium tender wins +2–3 pp due to superior compliance scores. Modeled payback 18–30 months varies with SKU mix, channel breadth, and patient-scan activation. Sensitivities: each +10 pp dispenser participation lifts counterfeit detection +7–9%, while an additional +5 pp patient scan adoption boosts recall precision +4–6% through field verification.

Trends & Insights

Three technology currents define 2025–2030. (A) Permissioned consortia with public anchors: Most deployments operate as permissioned GCC consortia for throughput and privacy, while selected events (e.g., recall flags, disposition hashes) anchor to a public chain for non-repudiation. (B) Data-minimal sharing: Privacy-by-design patterns store hashes/claims on-chain and maintain payloads off-chain (EPCIS repositories), meeting GDP/GMP and cross-border rules; ZK or selective disclosure emerges for regulator audits without exposing commercial terms. (C) IoT-oracle maturation: Temperature, shock, and geofence events sign to the ledger, enabling automated hold/release and chain-of-custody proofs; this yields the 40% excursion reduction and lifts insurer confidence in specialty cold-chain lanes. Operationally, mobile verification expands from hospital pharmacies to community pharmacies and home-delivery, pushing patient scan adoption to 22–28%; push incentives (co-pay discounts, loyalty points) add +3–5 pp. Smart-recall playbooks standardize outreach (eRx messages, SMS in Arabic/English), cutting notify to 9h median. Analytics layers leverage ledger data to score diversion risk, segment gray-market patterns, and validate tender service levels. Sustainability gains appear as paper-based COAs/returns slips move on-chain (document handling −60%). Risks: vendor lock-in, uneven SME onboarding, and rural last-mile connectivity; mitigations include API-first contracts, onboarding subsidies, and offline-first scanning with batched submission. By 2030, blockchain traceability becomes a quality and brand asset, not just a compliance checkbox.

.png)

Segment Analysis

By product risk: Biologics & vaccines (38% of benefits) realize the biggest upside—0.9–1.3% revenue protection, cold-chain excursions −45%, and fastest payback (≈18–22 months). Oncology & specialty injectables (29%) see counterfeit reduction 60–70% with high dispenser verification. Small-molecule retail Rx (25%) benefit via returns and chargeback disputes −45% and improved recall precision. OTC & supplements (8%) adopt selectively for export markets and brand trust. By stakeholder: MAHs/brand holders monetize revenue protection and tender wins; wholesalers/3PLs capture warehouse efficiency and dispute reduction; pharmacies gain shrink reduction and loyalty lift via patient scans. By country cluster: Saudi Arabia (45% of regional spend) emphasizes national registries and tender scoring; UAE/Qatar/Kuwait/Bahrain/Oman (40%) prioritize export compliance and private retail chains; Levant/North Africa early adopters (15%) focus on corridor traceability to GCC. Workflow benefits: returns processing time −52%, discrepancy investigations −46%, recall logistics cost −45%, and gray-market leak detection +35–50% in volume-weighted terms. IT segmentation: ~62% of networks will be managed consortium platforms with standardized APIs; 38% bespoke or MAH-led private chains. Across segments, the OpEx/pack −34% after year-2 is driven by rules-based exceptions, auto-aggregation reconciliation, and distributor ASN validations. KPI targets by 2030: ≥75% dispenser participation, ≥95% event capture integrity, ≤0.1% serial collisions, and <24h end-to-end recall message propagation across the network.

Geography Analysis

Saudi Arabia anchors regional momentum with centralized guidance, public-private pilots, and procurement clauses that favor end-to-end serialization plus verification. By 2030, KSA is projected to have >90% Rx coverage and ~80% dispenser participation, with patient scan adoption 26–30% in urban corridors (Riyadh, Jeddah, Dammam). UAE follows with strong private-chain pharmacy networks and airport-centric 3PL hubs; Qatar and Kuwait scale through hospital systems first, then retail. Bahrain and Oman emphasize cold-chain IoT for biologics imports, hitting excursions −40%. Levant exporters implement corridor traceability to meet GCC tender conditions, prioritizing diversion analytics and dispute reduction. Cross-border corridors adopt GS1 EPCIS 1.2/2.0 profiles with Arabic/English label support, while customs nodes join as read-only validators to speed clearance (border dwell −18%). Payback varies with maturity: KSA/UAE 18–24 months, Kuwait/Qatar 22–28 months, Oman/Bahrain 24–30 months. Regional KPI medians by 2030: recall notify 9h, complete 3.5 days, counterfeit −55–70%, OpEx/pack −34%, chargeback disputes −45%. Challenges include SME onboarding costs, data residency constraints, and last-mile connectivity in remote areas; mitigations include subsidized scanners, edge/offline apps, and national nodes offering shared EPCIS hosting. Overall, GCC leadership and trade-corridor harmonization make the Middle East a front-runner for enterprise-grade blockchain traceability at scale.

.png)

Competitive Landscape

Competing stacks blend serialization vendors, blockchain platforms, IoT cold-chain providers, and systems integrators. By 2030, the top 8–10 regional platforms will control ~65% of spend, offering managed consortium networks, GS1-native data models, and regulator dashboards. Differentiators: high-throughput event ingest (≥5k EPS), EPCIS 2.0 support, ZK/claims-based audit sharing, dispute modules, and smart-recall playbooks. Serialization leaders compete on line-speed camera accuracy, aggregation reliability, and Uptime ≥99.5%; blockchain providers compete on latency (<2s commit) and cost/tx with predictable subscription pricing. IoT partners add calibrated sensors and tamper-evident seals signed to the ledger. SIs win with L3/L4/L5 integration, pharmacy POS adapters, and change-management (training 1–2 hours per pharmacist, SOP kits). Commercial models shift toward outcomes-linked SLAs (e.g., bonuses for recall time ≤4 days or dispute cycle ≤10 days). Pricing: typical platform subscription $350–800k/year for mid-tier MAHs; per-event costs trend down 25–35% by 2030 with volume. Buyers favor API-first, vendor-neutral contracts to avoid lock-in and mandate data export escrow. M&A is likely as serialization vendors acquire blockchain layers and IoT firms, forming full-stack offerings. Winners combine compliance grade, performance at volume, and clear ROI via 0.6–1.0% revenue protection, lean recalls, and fewer disputes—turning traceability from cost center into a competitive advantage in GCC tenders.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

Clinical Nutrition Market Size & Share Analysis - Growth Trends & Forecasts (2025 - 2030)

This report quantifies the clinical nutrition market across the US and UK (2025–2030), covering enteral, parenteral, and oral nutritional supplements (ONS). Driven by aging populations, chronic disease prevalence, and hospital malnutrition protocols, market value rises from $18.5B (2025) → $30.2B (2030) at a CAGR of 10.2%. Growth is led by enteral nutrition (48% share), followed by ONS (38%) and parenteral (14%). Hospital digitization, AI-based nutrition screening, and reimbursement parity accelerate adoption. ROI averages 16–22% for integrated hospital nutrition programs.

$ 1395

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071