68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

AI Virtual Shopping Assistants: Conversational Commerce & Basket Size Optimization in Asia-Pacific E-Commerce

Between 2025 and 2030, Asia-Pacific e-commerce accelerates from static FAQ/chatbots to AI virtual shopping assistants (VSA) that truly sell—conversing in local languages, understanding intent across voice and text, and orchestrating catalog, pricing, inventory, and promotions to increase conversion and basket size. In India, the combination of UPI penetration, ONDC integrations, and multilingual ASR‑NLU enables VSAs to handle discovery, comparison, and checkout in a single session, while escalating to human experts for high‑consideration purchases. In Southeast Asia and East Asia, assistants blend live‑ops commerce with personalized bundles and post‑purchase care (returns, warranties) to lift LTV.

What's Covered?

Report Summary

Key Takeaways

1. VSAs shift from support to sales—guided discovery, bundles, and warranties drive AOV and CR.

2. Language depth (Hinglish + regional) and ASR quality are decisive for India scale.

3. Retrieval‑grounded generation with live price/inventory prevents hallucinations and trust loss.

4. UPI and one‑tap wallets convert intent to purchase; ONDC and marketplace APIs reduce friction.

5. Human‑in‑the‑loop for high‑consideration SKUs protects NPS and compliance.

6. Guardrails (claims, brand voice, accessibility) and audit trails avoid regulatory risk.

7. Attribution telemetry must isolate assistant‑driven lift vs media/promotions.

8. Outcome‑based contracts indexed to AOV/CR/CSAT lift will dominate procurement.

Key Metrics

Market Size & Share

VSAs scale where language, payments, and catalog depth intersect. In this illustrative outlook, India adopters expand from ~450 to ~1,950 (2025→2030) as Hinglish and regional language NLU improve and UPI enables in‑assistant checkout. The rest of APAC grows from ~900 to ~3,350, led by China, Japan/Korea, and Southeast Asia marketplaces blending live‑ops and chat commerce. Share concentrates among platforms that unify ASR‑NLU, retrieval‑grounded generation, catalog/pricing integration, and payments under one orchestration layer.

By 2030, VSAs account for a meaningful share of assisted sessions and a measurable fraction of GMV in fashion and electronics, and a rising share in grocery as substitutions, freshness, and slot booking are handled in‑conversation. Indian retailers gain share when assistants reduce discovery friction, expose value bundles, and integrate vernacular support. Marketplaces consolidate via trust features—buyer/seller verification and return automation—implemented directly through the assistant.

Market Analysis

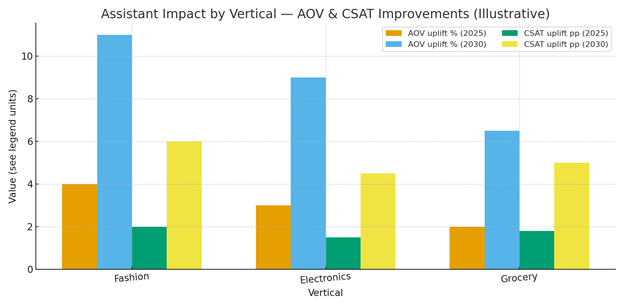

AOV and CSAT lift arise when assistants personalize discovery and close the loop to checkout. In this outlook, fashion sees the largest gains (AOV +7–11%) thanks to styled bundles and size guidance; electronics follows (AOV +6–9%) via compatibility advice and warranty add‑ons; grocery gains moderate but steady lift (AOV +4–6.5%) through substitution and basket completion. CSAT improves as response quality, language coverage, and handoff fidelity rise. Cost drivers include ASR‑NLU inference at scale, catalog enrichment, and payments/compliance integration. Benefits include improved conversion, lower call/chat center load, and higher LTV from post‑purchase support executed by the assistant.

Risks: hallucinated specs, inaccurate availability, payment drop‑offs, and privacy lapses. Mitigations: retrieval‑grounding with live data, strict guardrails and claims checks, human escalation for high‑risk queries, and robust observability (latency, answer correctness, handoff outcomes). Attribution needs finance‑grade methods to isolate assistant impact from concurrent promotions.

Trends & Insights (2025–2030)

• Hinglish + regional language ASR‑NLU unlocks India scale; code‑switching support is critical.

• Retrieval‑grounded generation tied to catalog, pricing, inventory, and policy prevents hallucination.

• Visual + voice assistants rise; AR try‑ons and configuration UIs integrate into chat flows.

• Payments inside chat (UPI/wallets) compress purchase latency; one‑tap verification cuts friction.

• Trust features (seller verification, warranty/returns automation) operate within the assistant.

• Post‑purchase care (delivery tracking, returns, service) grows LTV and reduces contact‑center load.

• Governance: brand voice, claims, accessibility, and audit trails become procurement must‑haves.

• Outcome‑based pricing tied to verified AOV/CR/CSAT lift gains traction with enterprises.

Segment Analysis

• Fashion: conversational discovery, size/fit guidance, and styled bundles drive basket size; returns flows handled in‑assistant.

• Electronics: compatibility checks, comparators, and warranty add‑ons; human expert escalation for premium SKUs.

• Grocery: substitutions and basket completion; perishable handling and slot booking; vernacular support for local preferences.

• Marketplaces: buyer/seller verification, dispute resolution, and cross‑category personalization.

Buyer guidance: localize language and catalog attributes; integrate live price/inventory; define escalation playbooks; and implement measurement frameworks that tie assistant interventions to GMV and CSAT.

Geography Analysis (Asia-Pacific & India)

Readiness is strongest in India Tier‑1 metros (language talent, UPI penetration, and marketplace ecosystems) and China Mainland (super‑app infrastructure). Japan/Korea contribute high‑quality ASR‑NLU and commerce APIs; Singapore/Malaysia lead Southeast Asia enterprise deployments; Indonesia/Philippines/Vietnam scale quickly once payments and language coverage mature. The stacked criteria—data/ID graph, language/ASR‑NLU, commerce API depth, payments readiness (UPI/alt‑pay), and organization capability—highlight where VSAs can meet production SLAs first. Implications: stage rollouts in Tier‑1 India and SG/MY for early wins; localize language across Tier‑2/3 India; negotiate marketplace and ONDC integrations; and enforce guardrails and audit trails to manage risk.

Competitive Landscape (Platforms & Operating Models)

Stacks converge on: (i) ASR‑NLU tuned for regional languages; (ii) retrieval‑grounded generation with product/pricing/inventory connectors; (iii) orchestration across chat, voice, and visual UIs; (iv) payments and identity verification within the assistant; and (v) telemetry/attribution dashboards. Differentiators: latency SLAs, language accuracy, catalog grounding, payments depth, and governance. Operating models range from managed services for mid‑market sellers to enterprise control planes with modular adapters. Outcome‑based pricing tied to verified AOV, conversion, and CSAT lift becomes common by 2030 as finance teams demand causal attribution and auditability.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071