68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

AI-Driven Consumer Sentiment Analysis: Real-Time Pricing Adjustments & Competitive Benchmarking in Global Retail

Between 2025 and 2030, North American retailers shift from batch analytics to closed‑loop, AI‑driven pricing that ingests consumer sentiment, competitor signals, and inventory posture to update prices in minutes—not days. Sentiment models fuse social, review, and support channels with on‑site behavior; pricing engines then constrain outputs within guardrails (brand rules, MAP, elasticity bands) and execute across web, app, and stores via centralized APIs. Competitive benchmarking evolves beyond scraped list prices to availability, shipping promises, promotional depth, and perceived value scores.

What's Covered?

Report Summary

Key Takeaways

1) Latency reduction (hours → minutes) is the biggest driver of margin/markdown gains after data quality.

2) Guardrails (MAP, brand, fairness) and staged approvals prevent price whiplash and reputational risk.

3) Sentiment feature engineering (aspect‑level) explains promo lift and reduces over‑discounting.

4) Elasticity + cross‑elasticity + inventory constraints must optimize jointly, not in silos.

5) Omnichannel parity with localized rules avoids arbitrage and gaming by consumers/bots.

6) Competitive data must cover availability and shipping promises, not just list price.

7) Attribution telemetry (A/B, geo‑tests) is essential to bank RoI with finance teams.

8) Data privacy, algorithmic transparency, and change control are now procurement must‑haves.

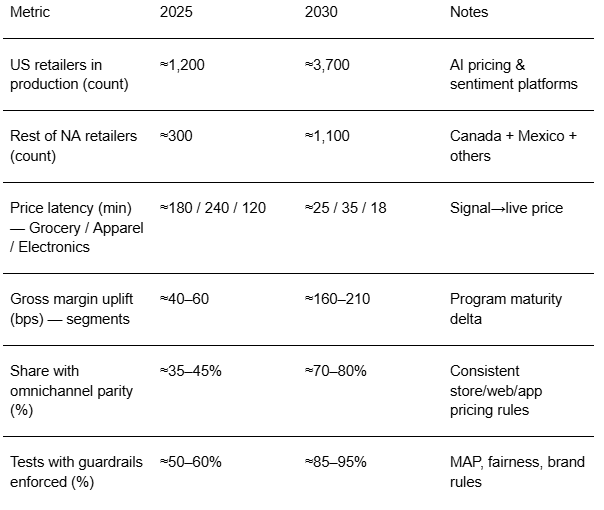

Key Metrics

Market Size & Share

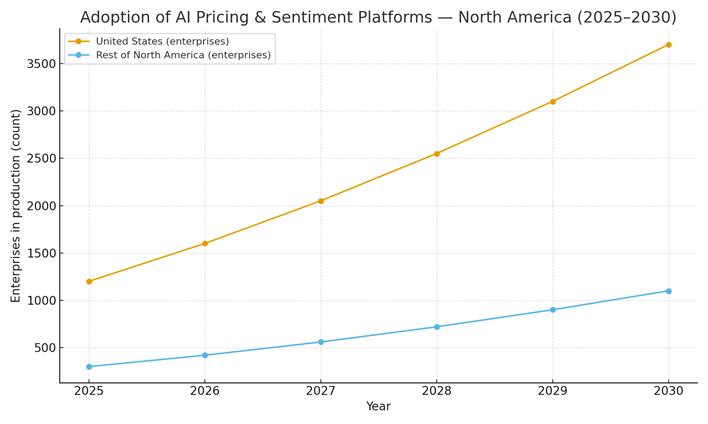

Adoption concentrates first in high‑SKU, high‑velocity categories where promo cadence is weekly and price sensitivity is measurable. In this illustrative view, US production adopters of AI pricing/sentiment platforms grow from ~1.2k in 2025 to ~3.7k by 2030; the rest of North America from ~0.3k to ~1.1k. Grocery and mass merchandise dominate early share due to sheer SKU count and clear elasticity signals; apparel follows as sentiment features improve size‑color granularity and returns signals; consumer electronics scales last as MAP/fair‑use constraints and supply shocks complicate pricing freedom.

Market share accrues to platforms that bundle competitive intelligence, sentiment extraction, elasticity modeling, and price execution in a single workflow with governance. Omnichannel parity becomes table stakes; regional price localization persists but is explainable and auditable. By 2030, the largest retailers run closed‑loop systems tied to inventory and labor constraints, while mid‑market players adopt managed‑service models to ‘rent’ data science and monitoring capabilities.

Market Analysis

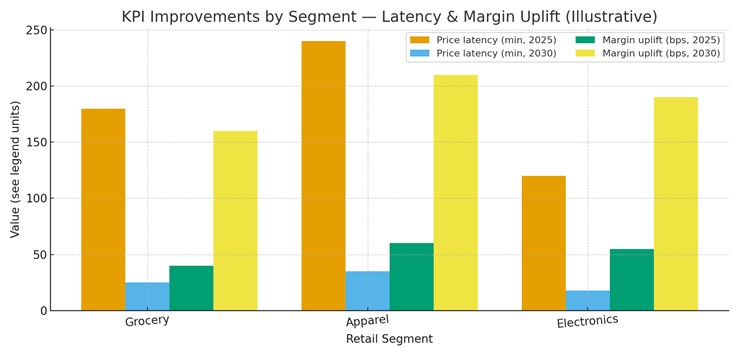

Economics hinge on the interaction of latency, elasticity accuracy, and competitive context coverage. In this outlook, price‑latency collapses from ~120–240 minutes to ~18–35 across major segments, supporting same‑day promo tuning and localized markdowns. Gross margin uplift expands from ~40–60 bps (2025 pilots) to ~160–210 bps as guardrails, experimentation, and attribution mature. Key cost drivers include data licensing (competitive feeds, review/social firehose), engineering (feature pipelines, real‑time infra), and governance (approvals, audit logs, compliance). Benefits extend beyond margin: better price‑perception indices, fewer out‑of‑stocks from demand shaping, and lower promo waste.

Risks: data sparsity for long‑tail SKUs; model drift with seasonal trend shifts; adversarial scraping/bot noise; and legal exposure around dynamic price discrimination. Mitigations: hierarchical models with shrinkage; frequent backtests and drift alarms; bot detection and identity controls; fairness tests across segments; and clear consumer disclosures. RoI improves with omnichannel execution and inventory‑aware constraints that avoid ‘winning’ a price at the cost of stockouts.

Trends & Insights (2025–2030)

• Aspect‑based sentiment becomes a first‑class feature: fit, quality, delivery, service; mapped to elasticity shifts.

• Competitive ‘value score’ replaces price‑only matching: availability, delivery promise, and bundling all factor in.

• Edge pricing for stores: micro‑batches update in near‑real‑time based on local demand, weather, and events.

• Foundation models fine‑tune on retail text; small, fast models run inference for latency‑critical decisions.

• Synthetic A/B testing accelerates policy vetting; production tests retain conservative guardrails.

• Privacy‑preserving learning (federated, differential privacy) reduces data‑movement risk.

• Price integrity dashboards become standard—incident rollbacks, MAP breaches, and fairness metrics are monitored.

• Procurement shifts to outcome‑based pricing tied to verified margin bps and latency SLAs.

Segment Analysis

• Grocery: highest frequency, low margins; price image is sensitive—tight guardrails, basket‑level elasticity, and promo cannibalization controls are critical.

• Apparel/Footwear: sentiment captures fit/quality buzz; localized markdowns and capsule drops drive sell‑through without brand erosion; returns signals inform pricing.

• Consumer Electronics: MAP and supply constraints limit freedom; value scores (availability, shipping) and bundle pricing substitute for raw price cuts.

• Home/DIY: seasonal/weather signals influence elasticities; curbside vs delivery fees integrate with price.

• Health/Beauty: influencer sentiment dominates lift; fraud/bot defenses around hot SKUs are essential.

Buyer guidance: instrument telemetry for attribution; enforce omnichannel parity; codify guardrails; and stage rollout: pilots in one region/category, then scale with automated approvals and incident playbooks.

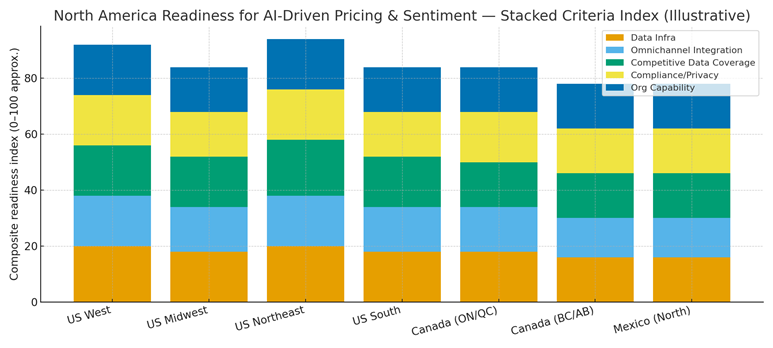

Geography Analysis (North America)

Readiness clusters in the US Northeast and West (cloud/data maturity, vendor ecosystems), followed by the South and Midwest as omnichannel integration and supply‑chain telemetry improve. Canada’s Ontario/Quebec benefit from data talent and privacy governance experience; Western Canada and Northern Mexico build from growing retail tech ecosystems. The stacked criteria—data infrastructure, omnichannel integration, competitive data coverage, compliance/privacy, and organization capability—highlight where closed‑loop pricing can scale fastest.

Implications: stage rollouts where data quality and org readiness are strongest; invest in product graph cleanup and identity resolution; negotiate data licenses for full competitive context; and align legal/privacy with experimentation velocity to avoid bottlenecks.

Competitive Landscape (Vendors & Operating Models)

The stack consolidates around: (i) competitive intelligence providers (price, availability, delivery, promos); (ii) sentiment/NLP platforms; (iii) pricing engines with experimentation frameworks; (iv) integration layers to POS/e‑commerce; and (v) telemetry/attribution dashboards. Differentiators: latency SLAs, breadth of competitive coverage, aspect‑level sentiment quality, and guardrail governance. System integrators offer managed services for mid‑market retailers lacking in‑house data science. Delivery models shift to outcome‑based contracts indexed to verified margin bps and latency. Winners tie price to inventory and labor constraints, publish integrity metrics (MAP compliance, fairness), and maintain fast incident rollback. By 2030, AI‑driven pricing is a board‑level capability with clear audit trails and explainability.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071