68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Space Tourism in India: A $2B Market Opportunity by 2040

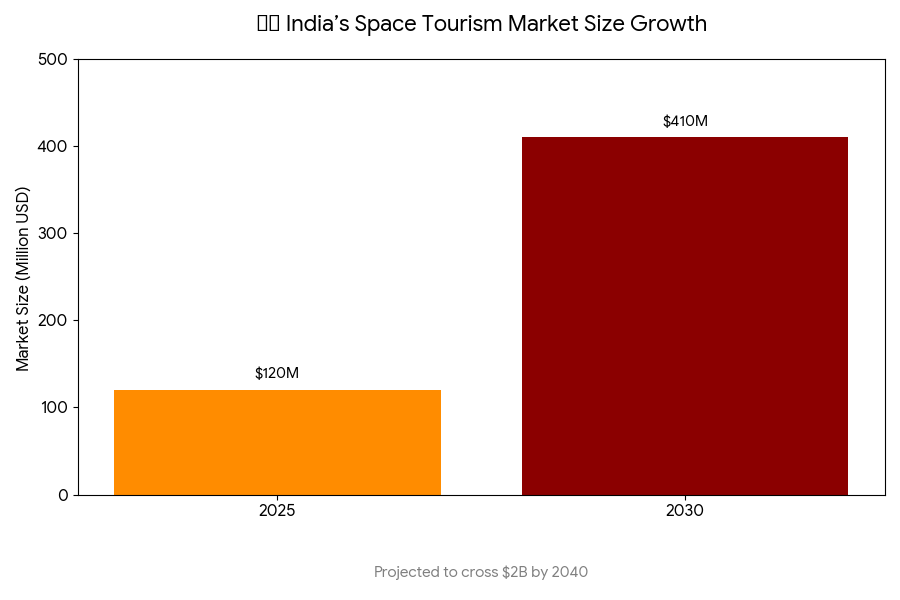

India’s emerging space tourism sector is projected to reach a $2B market opportunity by 2040, with a strong foundation in public–private space collaborations, commercial launch infrastructure, and aerospace innovation ecosystems. Between 2025 and 2030, the domestic market will expand from a conceptual $120M to $410M, marking a CAGR of 27.4%, before accelerating post-2030 due to regulatory liberalization and technological readiness. ISRO, alongside private entities like Skyroot, Agnikul, and Bellatrix, is shaping the foundation for suborbital tourism, training centers, and orbital viewing modules. By 2040, India could capture 3.5–4% of global space tourism revenue, driven by affordable access models and emerging astronaut training ecosystems.

What's Covered?

Report Summary

Key Takeaways

- India’s space tourism market to reach $2B by 2040.

- Market expansion from $120M (2025) to $410M (2030), CAGR 27.4%.

- India’s share in global space tourism projected at 3.5–4%.

- ISRO’s Gaganyaan to accelerate suborbital tourism readiness by 2026–27.

- Private launch startups (Skyroot, Agnikul, Bellatrix) to drive commercialization.

- Ticket pricing expected at $240K–$300K per suborbital seat by 2030.

- Training and simulation hubs to attract $150M investment by 2028.

- Tourism payload capacity to reach 120 suborbital passengers annually by 2032.

- Government–private partnerships to scale at $60M annually by 2027.

- By 2040, orbital hospitality modules could contribute $480M in recurring revenue.

Key Metrics

Market Size & Share

India’s space tourism sector is expected to scale from $120M in 2025 to $410M by 2030, ultimately crossing $2B by 2040 as orbital tourism becomes commercially viable. The initial phase (2025–2030) focuses on simulation, training, and suborbital flight programs, led by ISRO’s Gaganyaan initiative and startups like Skyroot Aerospace and Agnikul Cosmos. Post-2030, the industry will mature with private launchpads, low-Earth orbit (LEO) modules, and reusable rocket systems reducing costs by 40%. India’s market share, projected at 3.5–4% of global space tourism, will be driven by cost-efficient access, infrastructure localization, and government partnerships under IN-SPACe policy reforms.

Market Analysis

The market’s expansion is underpinned by public–private partnerships and regulatory liberalization fostering innovation. Between 2025 and 2030, launch costs are forecasted to drop from $9,000/kg to $3,500/kg, improving commercial feasibility. Training and astronaut preparation services will emerge as revenue leaders, contributing $120M annually by 2029. India’s competitive advantage lies in low-cost aerospace manufacturing, skilled workforce, and established ISRO infrastructure. The government’s space commercialization framework (2026) will enable private licensing for suborbital tourism operators. By 2040, orbital modules and space hospitality ventures could capture $480M in annual recurring revenue, integrating with global networks led by Axiom Space and Virgin Galactic.

Trends & Insights

- Suborbital Tourism Readiness: Gaganyaan mission completion to unlock commercial passenger trials by 2027.

- Private Launch Ecosystem: Skyroot, Agnikul, and Bellatrix developing low-cost reusable vehicles.

- Space Training Hubs: Bengaluru and Hyderabad projected to host Asia’s first training centers by 2028.

- Simulation Tourism: Growth in zero-gravity and VR-based experiences (+45% CAGR).

- Insurance Framework Evolution: Early risk-sharing models to support investor confidence.

- Government Incentives: IN-SPACe policy to provide 20-year infrastructure leases.

- International Collaboration: Partnerships with NASA, ESA, and JAXA for joint payload programs.

- STEM Education Integration: School–university tie-ups for space exposure programs.

- Reusable Rocket Adoption: Cost efficiency improving launch cadence by 32% by 2030.

- Long-Term Orbital Ventures: Concept studies for LEO hotels and spacewalk tourism targeting 2040 rollout.

Segment Analysis

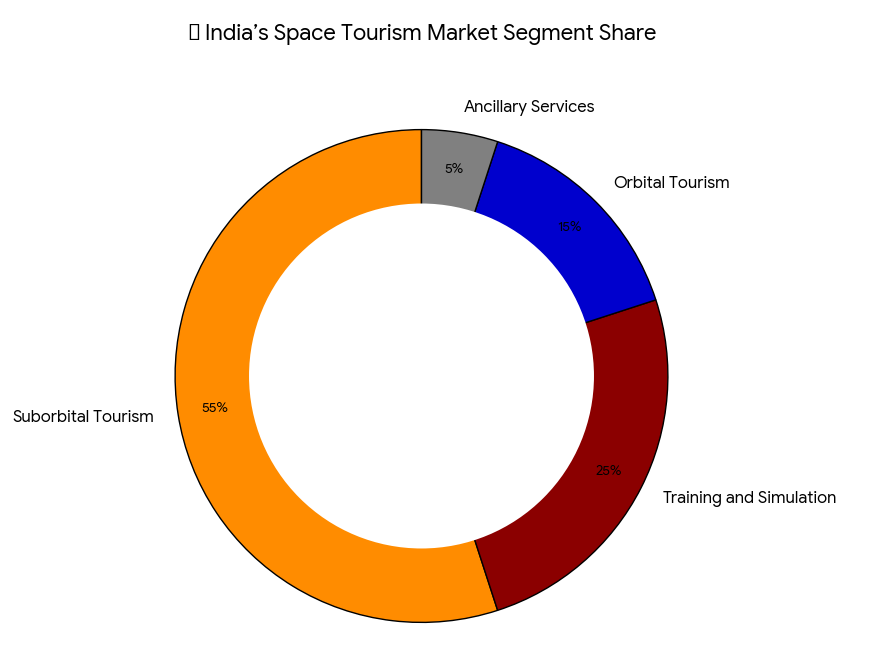

The market is divided into suborbital tourism (55%), training and simulation (25%), orbital tourism (15%), and ancillary services (5%). Suborbital flights, accounting for 55%, will dominate until 2032, primarily offering 5–10-minute space exposure. Training and simulation centers, at 25%, are expected to attract both civilian participants and STEM-focused educational tourism. Orbital tourism, though nascent, will scale to 15% share by 2040 with LEO capsules and orbital hotels. Ancillary services—including insurance, logistics, and merchandise—will generate $100M+ in indirect value.

Geography Analysis

India’s key space tourism clusters will emerge in Andhra Pradesh (Sriharikota), Karnataka (Bengaluru), and Tamil Nadu (Chennai), housing training, launch, and manufacturing facilities. Hyderabad and Bengaluru will serve as simulation and training ecosystems, while Sriharikota remains the primary suborbital launch site. By 2030, additional facilities in Gujarat’s Dholera Spaceport will support private space launches under the IN-SPACe regime. The domestic tourism crossover—expected to attract 25,000+ simulation participants annually—will complement export-oriented orbital tourism packages, positioning India as a regional hub for affordable space experiences.

Competitive Landscape

The competitive ecosystem includes ISRO, Skyroot Aerospace, Agnikul Cosmos, Bellatrix Aerospace, and Dhruva Space, alongside global collaborators like Virgin Galactic and Blue Origin. Skyroot’s Vikram series and Agnikul’s Agnibaan are enabling suborbital flight economics under India’s cost advantage. ISRO’s technology transfer policy (2027) will allow private operators to repurpose government-tested designs for tourism use. Bellatrix focuses on in-orbit propulsion, while Dhruva Space provides satellite integration support. International entrants like Axiom Space are exploring joint orbital hospitality initiatives with Indian partners. The race to commercialize space tourism infrastructure by 2040 positions India as the next major frontier in accessible human spaceflight.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071