68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Cross-Border FX Disruption: Digital Wallets Saving $4B in Traveler Fees by 2030

The cross-border foreign exchange (FX) ecosystem is undergoing a major transformation across Europe and the United States. With international travel recovering and consumer demand for seamless transactions rising, FX fees have become a critical point of friction. Traditional banking and card-based systems typically charge hidden mark-ups ranging from 1–3.5% on every transaction, translating to billions in consumer losses annually. In contrast, digital wallets offering real-time FX conversion, transparent pricing, and multi-currency functionality are rapidly emerging as cost-efficient disruptors. By 2030, digital wallets are projected to save travelers approximately $4 billion in cumulative FX-related fees. This will be driven by wallet adoption rising from 20% of frequent travelers in 2025 to 45% by 2030, supported by improved infrastructure, embedded fintech APIs, and heightened regulatory pressure on fee transparency. The FX margin among traditional card issuers will compress from 1.8% to near 1.2%, while wallet-based transactions stabilize at a much lower 0.5% margin. Europe leads this shift due to the PSD3 regulatory framework, the Digital Euro initiative, and mature fintech ecosystems, while the U.S. sees slower uptake but a larger total transaction base.

What's Covered?

Report Summary

Key Takeaways

1. Digital wallets will compress FX margins from ~1.8% to 0.5% by 2030.

2. Europe will lead adoption, while U.S. provides volume-driven savings.

3. Regulatory frameworks such as PSD3 and Open Banking boost transparency.

4. Travel and fintech ecosystems are converging through embedded APIs.

5. Banks and card networks face sustained pressure on FX revenues.

6. Consumer demand for transparency accelerates wallet penetration.

7. Multi-currency and expense management features enhance traveler loyalty.

8. Wallet-based FX will evolve into a mainstream financial service vertical.

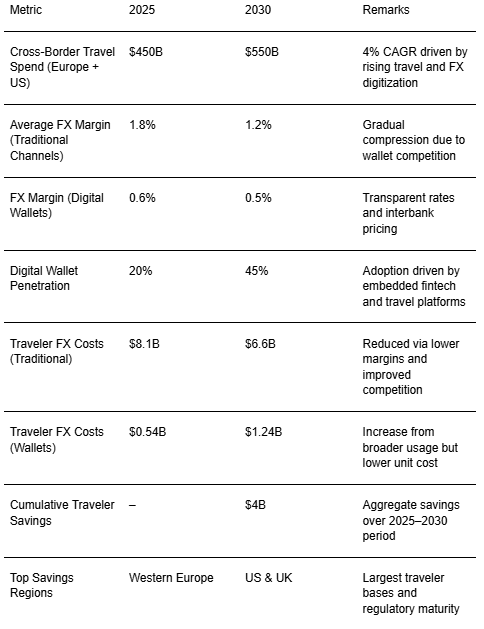

Key Metrics

Market Size & Share

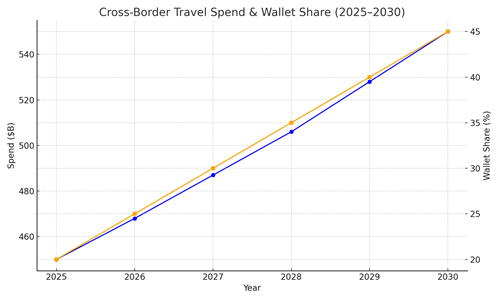

Cross-border travel expenditure across Europe and the U.S. is projected to increase from approximately $450 billion in 2025 to $550 billion by 2030, reflecting steady post-pandemic recovery and globalization of spending behavior. Wallet-based FX transactions, currently representing 20% of total cross-border payments, will climb to 45% within this period. This transition marks a structural change in FX fee distribution, as direct-to-consumer digital wallets bypass intermediaries and deliver lower, transparent mark-ups. The following line chart visualizes both overall cross-border spending growth and the expanding share of wallet-based transactions.

Market Analysis

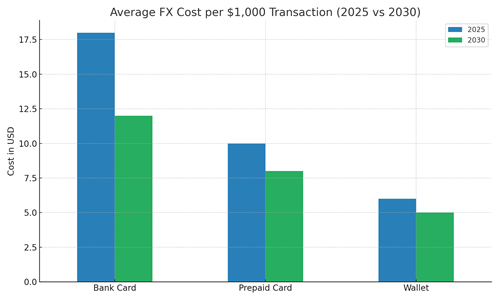

Traditional FX channels remain cost-heavy due to mark-ups, interbank spreads, and correspondent banking layers. Average per-transaction fees through banks and card issuers stand at $18 per $1,000 spent, while prepaid FX cards average $10. Wallet-based FX alternatives reduce this cost to roughly $6 today, expected to drop to $5 by 2030. The bar chart below illustrates this cost differential and highlights the emerging efficiency gap between legacy financial institutions and wallet-native fintechs.

Trends & Insights

Several macro and technological trends drive this FX disruption. The convergence of fintech innovation and cross-border mobility has accelerated wallet adoption. Regulatory frameworks like PSD3 and Open Banking mandate transparency in fees, while the anticipated launch of the Digital Euro will further enhance consumer trust. Millennials and Gen Z travelers, prioritizing convenience and cost savings, are key demand catalysts. Meanwhile, the U.S. market lags due to fragmented regulatory oversight and entrenched credit card culture. However, U.S. fintech firms are aggressively partnering with global wallets, signaling upcoming acceleration. By 2030, the global FX revenue pool will rebalance toward digital-native players, with cross-border payment efficiency increasing by 35–40%. The structural outlook is clear: the wallet revolution is no longer a fintech sub-trend but a macroeconomic shift reshaping how money moves across borders.

Segment Analysis

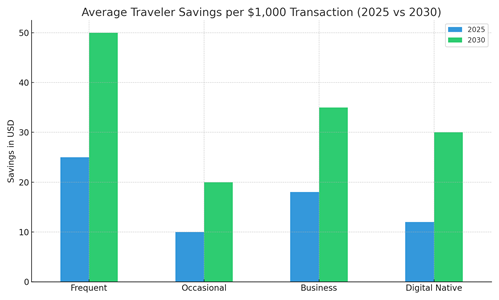

The impact of FX wallet adoption varies across traveler segments. Frequent travelers and corporate users drive over 60% of total volume, benefiting most from high-frequency savings. Digital-native travelers exhibit strong adoption intent due to superior mobile experience and fee transparency. Business travelers prefer multi-currency wallets with integrated expense management tools. Occasional travelers, though slower adopters, represent a significant latent base. The bar chart compares per-$1,000 savings across traveler segments for 2025 and projected 2030.

Geography Analysis

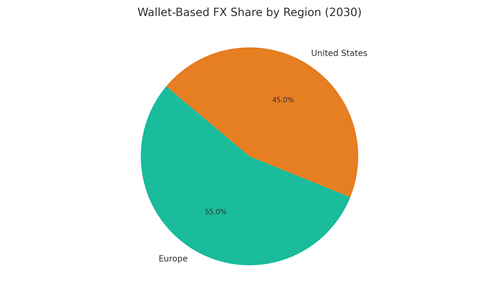

Europe accounts for approximately 55% of wallet-based FX transactions by 2030, benefiting from harmonized regulations, widespread travel, and integrated banking infrastructure. The U.S., contributing 45%, experiences slower adoption due to legacy systems but retains large absolute transaction volumes. Together, these regions account for over $4B in cumulative FX savings through wallet penetration. The pie chart below depicts the distribution of wallet-based transaction share by region.

Competitive Landscape

The competitive ecosystem is defined by three key participants: traditional banks, card issuers, and fintech wallet providers. Fintechs such as Wise, Revolut, and Payoneer maintain FX margins of ~0.5%, offering real-time rates and low-cost transfers. In contrast, banks and card issuers retain higher margins, averaging 1.8% and 1.2%, respectively. As partnerships between fintechs and travel platforms increase, wallets will become the default choice for international payments. The chart below compares FX margins by provider type for 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1395

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071