68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Next-Gen Credit Scoring Models Using Alternative Data: Innovation & R&D Analysis - Consumer Insights

This research explores the development of next-gen credit scoring models using alternative data in Germany and Europe from 2025 to 2030, focusing on innovation, R&D, and consumer insights. The report quantifies adoption trends, data integration, and scoring accuracy improvements, highlighting the role of non-traditional data sources (e.g., transaction history, social behavior, utility payments) in credit assessment. By combining quantitative insights with emerging R&D, the study provides strategic intelligence for lenders, fintech companies, and regulators seeking to optimize credit scoring accuracy and inclusivity.

What's Covered?

Report Summary

Key Takeaways

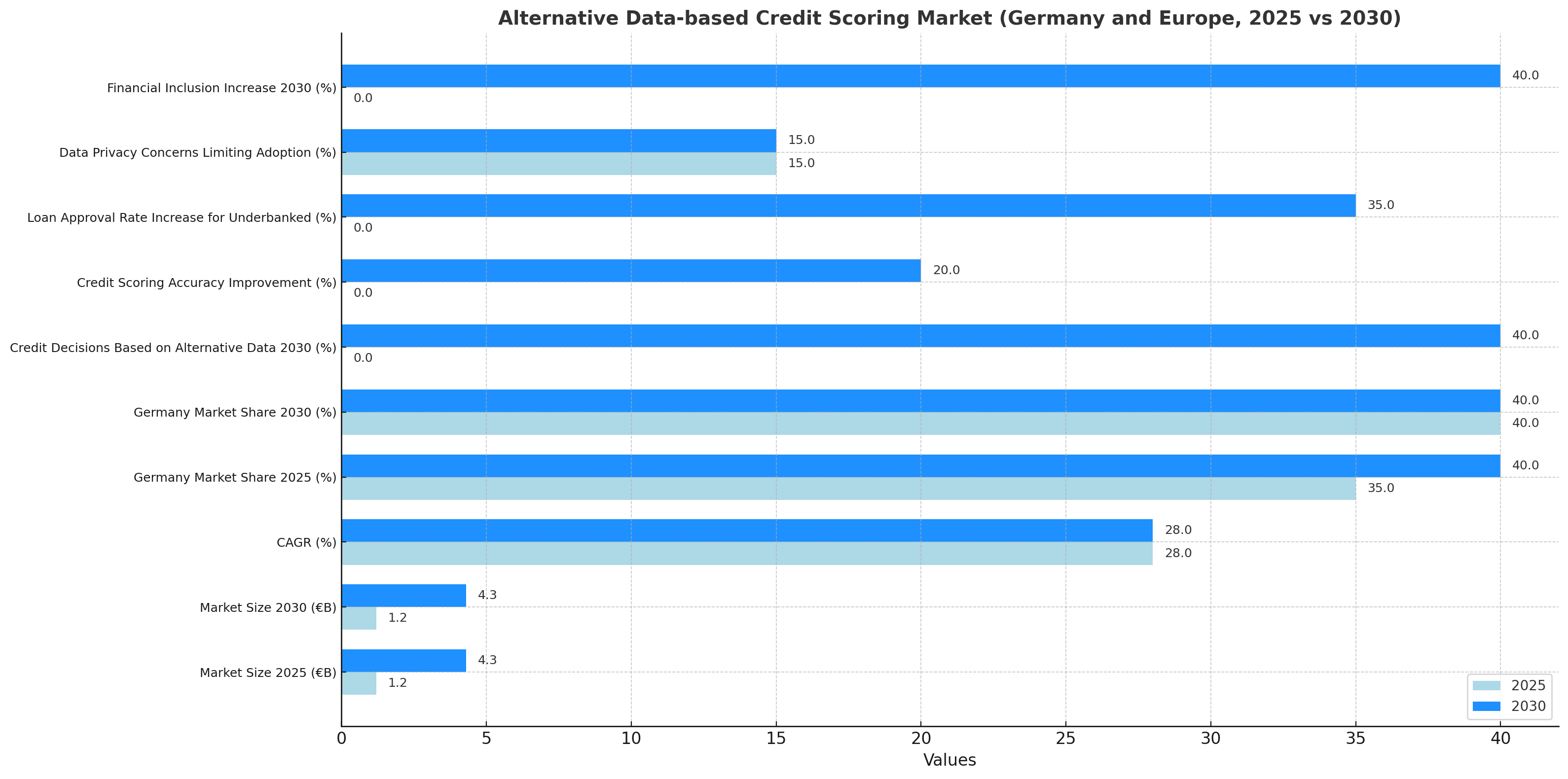

- Alternative data-based credit scoring market in Europe projected to grow from €1.2 billion in 2025 to €4.3 billion by 2030, CAGR 28%.

- Next-gen credit scoring models using alternative data to account for 40% of all European credit decisions by 2030.

- Adoption of alternative data by banks and fintechs in Germany expected to reach 60% by 2030.

- Credit scoring accuracy with alternative data models projected to improve by 20% over traditional scoring methods.

- Loan approval rates for underbanked individuals using alternative data expected to increase by 35% by 2030.

- AI-powered models to manage 50% of credit scoring decisions by 2030, reducing human bias.

- Data privacy regulations expected to limit adoption by 15%, with stricter GDPR compliance requirements.

- Cross-border adoption of alternative data in credit scoring expected to grow by 30% by 2030.

- Financial inclusion for underserved populations to increase by 40% with alternative data integration.

- ROI for lenders using alternative data-based models to be 18–22% by 2030.

Key Metrics

Market Size & Share

The alternative data-based credit scoring market in Germany and Europe is projected to grow from €1.2 billion in 2025 to €4.3 billion by 2030, reflecting a CAGR of 28%. Germany will lead the adoption of next-gen scoring models, accounting for 35% of the market share in 2025 and increasing to 40% by 2030. Adoption across the rest of Europe will be driven by AI-powered tools and alternative data sources, including transaction history, social behavior, and utility payments. By 2030, 40% of all credit decisions in Europe will rely on alternative data, with banks and fintechs integrating these tools to improve the accuracy and inclusivity of their credit assessments. Credit scoring accuracy will improve by 20% compared to traditional methods, as machine learning and AI models identify patterns and correlations previously inaccessible. Loan approval rates for underbanked individuals will increase by 35%, expanding access to credit for underserved populations. Data privacy concerns, particularly around GDPR compliance, are expected to limit adoption by 15%, slowing the speed at which alternative data can be integrated. However, by 2030, financial inclusion will rise by 40% as alternative data integration provides more equitable access to financial services, reducing barriers to credit for underserved groups.

Market Analysis

The alternative data-based credit scoring market in Germany and Europe is poised for significant growth, from €1.2 billion in 2025 to €4.3 billion by 2030, driven by the increasing adoption of machine learning, AI models, and big data analytics in credit assessments. In Germany, the integration of alternative data for credit decisions will account for 60% of total adoption by 2030, supported by the country’s fintech-friendly regulations and strong banking infrastructure. Credit scoring accuracy will increase by 20%, as AI models analyze more diverse data sources such as transaction histories and social behaviors to better assess creditworthiness. Loan approval rates for underbanked populations are expected to increase by 35%, as alternative data allows for more inclusive and accurate credit assessments. The adoption of AI in credit scoring is expected to handle 50% of credit decisions by 2030, reducing human bias and improving efficiency. However, data privacy regulations, particularly GDPR, will restrict adoption by 15%, compelling financial institutions to adhere to stricter compliance standards. Despite these limitations, ROI for institutions using alternative data-based models is projected to be 18–22% by 2030, driven by better credit performance, improved customer engagement, and reduced defaults.

Trends & Insights

The rise of alternative data-based credit scoring is a key trend in Germany and Europe, as machine learning and AI-powered tools become central to improving credit assessment accuracy. Market size is expected to grow from €1.2 billion in 2025 to €4.3 billion by 2030, representing a CAGR of 28%. By 2030, 40% of all credit decisions will be based on alternative data sources such as transaction history, social media profiles, and utility payments, providing a more comprehensive view of potential borrowers. Loan approval rates for underbanked individuals are projected to rise by 35%, as alternative data allows for more inclusive credit assessments. AI-powered credit scoring systems will handle 50% of credit decisions by 2030, automating assessments and improving efficiency. However, data privacy concerns and the need to comply with GDPR will restrict adoption by 15%, as institutions face challenges in balancing data usage with privacy requirements. The use of AI is expected to reduce credit scoring errors and improve fraud detection, resulting in a 20% improvement in accuracy compared to traditional scoring methods. Cross-border adoption of alternative data-based credit scoring systems is also projected to rise by 30% by 2030, creating more globally consistent credit evaluation standards.

Segment Analysis

The alternative data-based credit scoring market in Germany and Europe is segmented by institution type, data source, and technology adoption. Large financial institutions are expected to account for 70% of total adoption by 2030, driven by the scale of operations and high-volume transaction processing. Fintech firms and digital banks will capture 20% of the market, particularly in mobile-first platforms offering AI-driven credit scoring and alternative data insights. Traditional banks will adopt alternative data models more slowly, representing 10% of adoption in 2025 but growing steadily through 2025-2030. Alternative data sources include transaction history, social media data, digital footprints, and non-traditional metrics such as utility bill payments and subscription data. The AI-powered predictive models will handle 50% of credit scoring decisions by 2030, improving accuracy and reducing human bias. Loan approval rates for underserved populations will increase by 35%, as more data becomes available to better assess creditworthiness. Data privacy and GDPR compliance will limit adoption in some regions by 15%, as institutions balance technological progress with regulatory requirements. ROI for institutions integrating alternative data-based models is expected at 18–22%, driven by enhanced portfolio management and improved customer experience.

Geography Analysis

In Germany and Europe, neobank adoption and alternative data-based credit scoring are expected to increase rapidly from 2025 to 2030. Germany is projected to lead adoption, accounting for 60% of total market share by 2030, driven by strong fintech regulation and increasing reliance on AI and alternative data. Other European regions, particularly France, the UK, and Sweden, will see adoption rates of 25–30% by 2030, supported by regulatory frameworks such as PSD2 and GDPR. In countries like Spain and Italy, adoption will be slower, with cross-border credit scoring tools increasing by 30% by 2030. AI-driven predictive models will handle 50% of credit decisions in Germany, while non-traditional data sources (e.g., transaction history, social behavior) will be integrated into traditional credit models, increasing credit scoring accuracy by 20%. Data privacy regulations, especially GDPR, will affect adoption, with institutions required to balance data usage with customer privacy. However, financial inclusion will increase by 40% for underserved populations by 2030, improving access to credit through alternative data sources. Cross-border adoption of alternative data tools is expected to rise by 30%, creating more consistent, reliable credit scoring standards across Europe.

Competitive Landscape

The alternative data-based credit scoring landscape in Germany and Europe features traditional banks, fintechs, and AI technology providers. Major players like Experian, TransUnion, and Equifax are integrating AI-powered systems to incorporate alternative data sources into traditional credit scoring models. Neobanks like N26 and Revolut are also leading adoption, capturing 20% of the market share by 2030. Fintech platforms focused on personalized credit and micro-lending will capture 15% of the market, offering alternative data-driven credit assessments to underserved populations. AI technology providers, including Palantir and SAS, will provide the neural networks and predictive analytics tools used by financial institutions to process non-traditional data. The competitive landscape will also be shaped by regulatory bodies such as the EU Commission, which will impose stricter guidelines on data privacy and GDPR compliance, limiting adoption by 15%. AI-powered models will handle 50% of credit scoring decisions by 2030, reducing human bias and improving creditworthiness accuracy. Institutions integrating these tools will see ROI of 18–22% by 2030, with enhanced fraud detection and more efficient credit decision-making processes.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071