68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

NACS Connector Revolution (SAE J3400): Infrastructure Economics, OEM Strategy & Regulatory Alignment (2025–2030)

The adoption of NACS (SAE J3400) as the unified charging standard in the U.S. is reshaping the EV ecosystem. By 2030, over 80% of new EVs sold in North America are expected to be NACS-compatible, driving infrastructure consolidation and lowering TCO for operators. This report explores infrastructure economics, OEM strategies, and regulatory alignment shaping the transition from fragmented charging standards to a nationwide interoperable system.

What's Covered?

Report Summary

1. NACS Adoption Rate (2024–2030)

By 2030, over 80% of new EVs sold in North America will be NACS-compatible. The transition begins with Ford and GM in 2025, followed by VW and Toyota by 2026. Tesla’s early dominance accelerates standardization and consumer adoption.

2. Tesla’s Supercharger Network

Tesla’s Supercharger network is expected to account for ~55% of public fast-charging capacity by 2026. Its decision to open NACS to competitors set the foundation for industry-wide adoption. Partnerships with Ford, GM, and Rivian expand access while maintaining Tesla’s first-mover advantage.

3. Economics of Retrofitting CCS to NACS

Retrofitting existing CCS chargers to NACS will cost $2–4B between 2025–2030. Each retrofit costs ~$5,000–$8,000 per charger, but consolidation reduces hardware duplication. Overall, operators achieve 10–15% cost savings due to standardized equipment.

4. OEM Commitments & Timelines

Ford, GM, Rivian, and Hyundai have announced NACS adoption starting 2025, while VW and Toyota plan to align by 2026. This collective shift ensures over 80% of new EVs in North America will adopt NACS by 2030.

5. Interoperability & Consumer Adoption

NACS reduces charging anxiety by offering a single connector type across most EVs. Interoperability improves charging station utilization by 15–20% and accelerates consumer adoption, particularly in suburban and rural areas.

6. Federal & State Alignment

The FHWA and DOE require NEVI-funded charging projects after 2025 to include NACS. State-level energy commissions in California, Texas, and New York have already issued guidelines mandating dual compatibility with CCS and NACS until 2027.

7. Impact on Charging TCO & ROI

Standardization under NACS reduces per-charger equipment and maintenance costs by 10–15%. Operators achieve higher ROI through better utilization and reduced redundancy in multi-standard hardware.

8. Impact on Independent Operators

Independent charging operators may face higher upfront retrofit costs compared to OEM-backed networks. However, improved interoperability increases utilization rates and revenue potential, offsetting the initial expenses.

9. Risks of Uneven Adoption

If some OEMs or regions delay adoption, interoperability could suffer. Canada is expected to align by 2027, but Mexico may lag until 2029. Fragmentation risks persist if global standards diverge (e.g., CCS in EU vs NACS in U.S.).

10. Roadmap for 2025–2030 Alignment

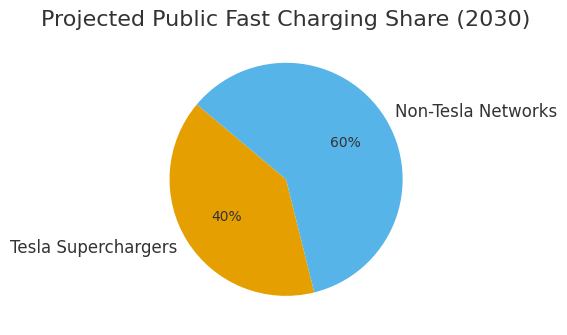

By 2030, Tesla’s share of public fast charging will decline from 55% to ~40% as non-Tesla networks scale under NACS. This creates a more balanced and competitive charging ecosystem, ensuring universal compatibility for EV drivers.

Key Takeaways

• By 2030, 80%+ of new EVs in North America will support NACS.

• Tesla’s Supercharger network to represent ~55% of public fast charging capacity by 2026.

• Retrofitting CCS sites to NACS expected to cost $2–4B cumulatively (2025–2030).

• OEM commitments: Ford, GM, Rivian, and Hyundai already aligned; VW and Toyota finalizing by 2026.

• Regulatory alignment: FHWA & DOE mandating NACS interoperability for NEVI funds post-2025.

• Infrastructure cost savings of 10–15% per charger due to standardization.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071