68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Middle East Renewable Energy Market 2025–2034: USD 52.4 Billion Growing to USD 210.6 Billion at 16.8% CAGR | Vision 2030 Investments, Solar Parks & Hydrogen Projects Drive Growth

The Middle East renewable energy market is forecast to grow from USD 52.4 billion in 2025 to USD 210.6 billion by 2034, registering a CAGR of 16.8%. This expansion is fueled by Vision 2030–aligned sustainability initiatives, mega solar and wind park developments, and the rise of green hydrogen projects across Saudi Arabia, UAE, and Oman. Governments are rapidly diversifying from hydrocarbons by introducing renewable procurement frameworks, foreign investment incentives, and public–private partnerships. With over 75 GW of renewable capacity under construction, the Middle East is evolving from an energy exporter to a clean energy innovation hub, leveraging its vast solar potential and strategic hydrogen infrastructure.

What's Covered?

Report Summary

Key Takeaways

- Market to expand from USD 52.4B (2025) to USD 210.6B (2034) at 16.8% CAGR.

- Saudi Arabia and UAE to command 60% of total regional capacity additions.

- Over 75 GW of renewable projects under active construction or development.

- Solar energy to contribute 55% of market revenues by 2034.

- Green hydrogen investments exceeding USD 70B across 12 projects.

- Wind energy capacity to surpass 15 GW by 2034, led by Egypt and Saudi Arabia.

- Transmission infrastructure upgrades accounting for USD 18B in parallel investments.

- Levelized Cost of Energy (LCOE) for solar projected to drop 25% by 2030.

- Private sector participation rising under Vision 2030 and Net Zero 2050 frameworks.

- Regional collaboration fostering GCC renewable grid interconnection initiatives.

Key Metrics

Market Size & Share

The regional renewable energy market will scale from USD 52.4B in 2025 to USD 210.6B by 2034, as governments pivot toward low-carbon energy systems. Saudi Arabia (38%) and UAE (22%) lead regional growth through flagship solar parks, hydrogen clusters, and wind farm expansions. Solar PV and CSP (Concentrated Solar Power) projects will drive over 55% of revenue, with NEOM’s hydrogen city, Mohammed bin Rashid Al Maktoum Solar Park, and Sohar Hydrogen Hub emerging as anchor investments. The GCC’s 75 GW renewable pipeline highlights regional momentum toward achieving carbon neutrality targets and expanding clean energy exports to Europe and Asia.

Market Analysis

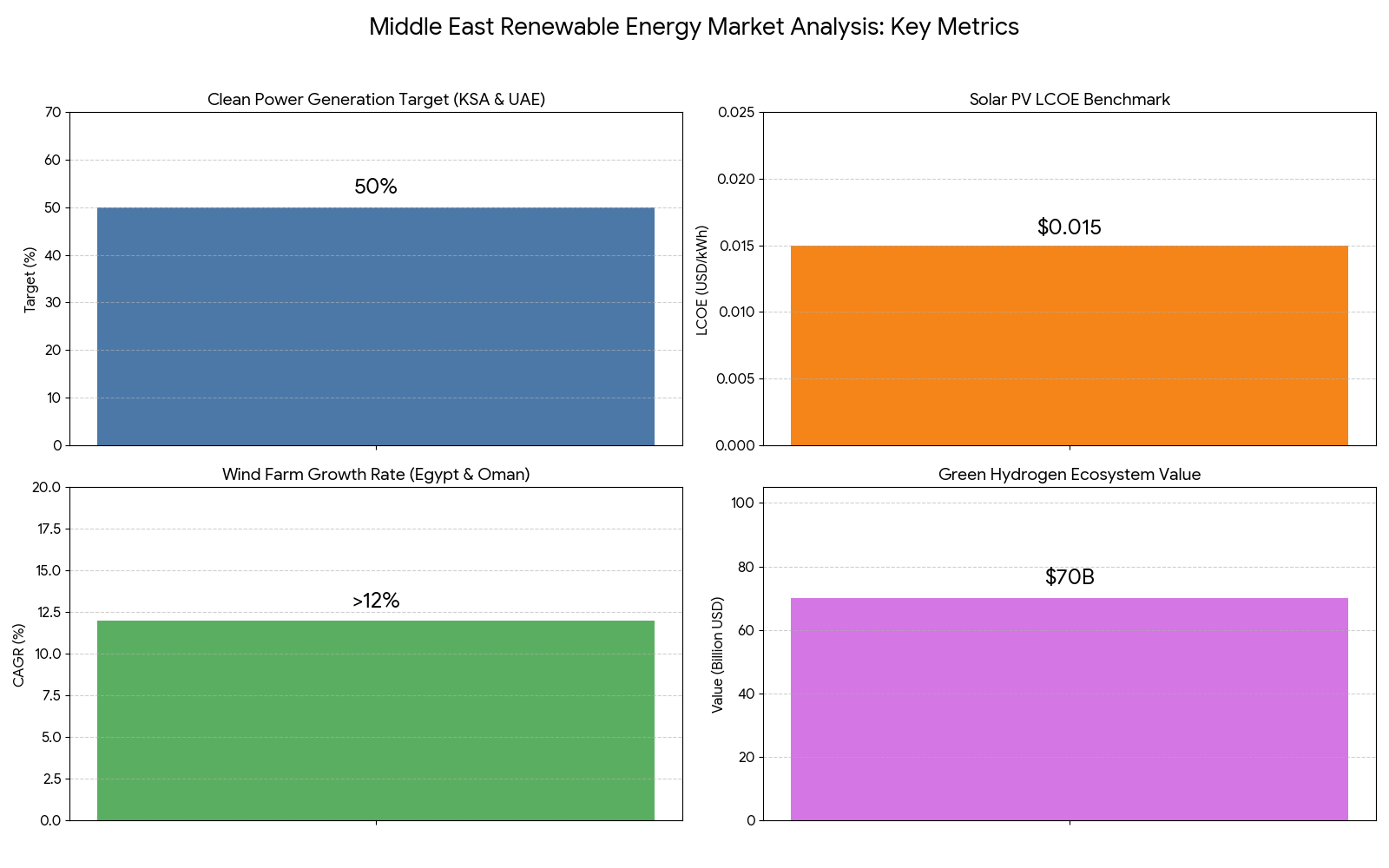

Accelerated policy reforms, competitive tenders, and the entry of global IPPs (Independent Power Producers) are catalyzing renewable growth across the Middle East. Saudi Arabia’s PIF-backed projects under Vision 2030 and the UAE’s Energy Strategy 2050 aim to reach 50% clean power generation by 2050. Solar PV dominates the portfolio, achieving an LCOE below USD 0.015/kWh, while wind farms in Egypt and Oman are scaling at >12% CAGR. The green hydrogen ecosystem, valued at USD 70B, is establishing long-term export corridors to Europe. Financial innovation, including sukuk-based renewable bonds and ESG-linked project financing, is enhancing investor participation and liquidity in the region’s clean energy transition.

Trends & Insights

- Hydrogen Acceleration: Over 12 large-scale hydrogen projects launched across the GCC.

- Hybrid Power Plants: Integration of solar–battery–hydrogen storage systems for grid stability.

- Utility-Scale Solar Growth: UAE’s 5 GW Al Dhafra Solar Park as a model for cost efficiency.

- Wind Expansion: Egypt’s Ras Ghareb and Saudi Dumat Al Jandal leading wind deployment.

- Green Financing: Surge in sustainability-linked sukuk and green bond issuance.

- Smart Grids: GCC nations investing in AI-based load balancing and transmission automation.

- Private Sector Entry: IPPs contributing to over 65% of new capacity development.

- Regional Interconnection: GCC Power Grid expansion enabling cross-border energy trading.

- Water-Energy Nexus: Renewable-powered desalination to reach 10 GW capacity by 2030.

- Talent Localization: National training programs developing green engineering expertise.

Segment Analysis

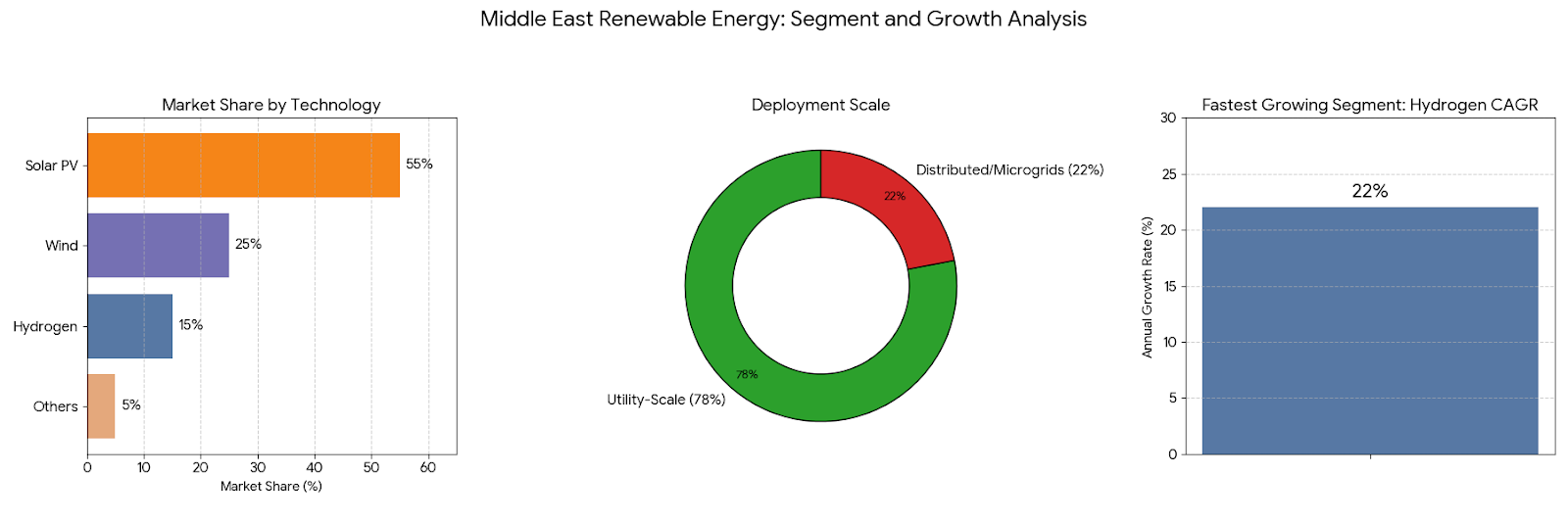

By technology, solar PV (55%), wind (25%), hydrogen (15%), and others (5%) dominate market segmentation. Solar PV leads due to abundant irradiation and cost competitiveness, while wind energy gains traction in coastal and highland areas across Egypt, Saudi Arabia, and Oman. Hydrogen projects, including NEOM’s USD 8.4B venture, will represent the fastest-growing segment with 22% CAGR, driven by industrial decarbonization and export potential. Utility-scale installations account for 78% of total deployment, while distributed solar and hybrid microgrids rise as viable options for off-grid industrial and residential applications.

Geography Analysis

Saudi Arabia leads with USD 80B in renewable investments, centered around NEOM, Sakaka, and Red Sea developments. The UAE follows with USD 45B, focusing on solar, hydrogen, and waste-to-energy projects under Energy Strategy 2050. Oman and Egypt are rapidly scaling green hydrogen hubs, while Jordan and Morocco serve as early renewable adopters exporting power to Europe. The GCC Interconnection Authority is investing in regional transmission upgrades to enable cross-border energy trade worth USD 10B annually by 2034. Bahrain and Kuwait, though smaller markets, are expanding solar rooftops and corporate PPA frameworks, diversifying their energy portfolios.

Competitive Landscape

Major players include ACWA Power, Masdar, ENGIE, EDF Renewables, Siemens Energy, and TotalEnergies, alongside regional utilities like DEWA, EWEC, and Saudi Electricity Company (SEC). ACWA Power leads the solar and hydrogen segment with multi-billion-dollar projects across NEOM and Oman, while Masdar spearheads UAE’s renewable expansion and international green energy ventures. ENGIE and EDF are investing heavily in hybrid solar–hydrogen platforms. Siemens Energy and GE Renewable Energy dominate turbine and grid technologies. The competitive ecosystem is increasingly shaped by long-term PPAs, sovereign-backed financing, and technology partnerships, positioning the Middle East as one of the world’s most dynamic renewable energy investment regions through 2034.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071