68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Life and Non-Life Insurance Market Size & Share Analysis – Growth Trends & Forecast (2025–2030)

The global insurance market, spanning life and non-life segments, is poised for steady growth between 2025 and 2030. Rising middle-class populations, digital distribution, regulatory modernization, and product innovation are driving penetration. By 2030, global premiums are expected to surpass USD 8 trillion, with non-life insurance outpacing life in growth due to health, motor, and cyber coverage demand. This report analyzes growth trends, segment shifts, regulatory impact, and competitive positioning.

What's Covered?

Report Summary

1. Global Market Size by 2030

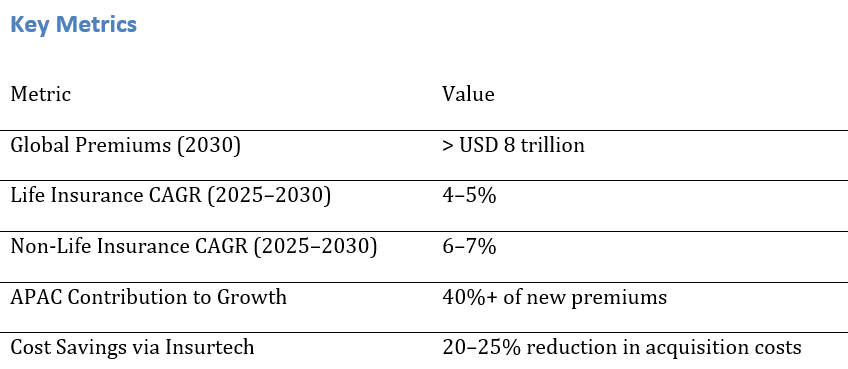

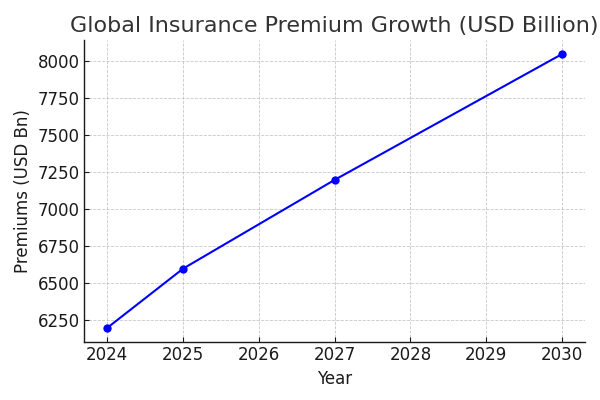

The insurance market is projected to exceed USD 8 trillion in premiums by 2030, up from USD 6.2 trillion in 2024. Life insurance will account for ~55% of premiums, while non-life expands faster to capture 45%. Growth is supported by expanding middle-class households, higher insurance penetration in emerging markets, and post-pandemic awareness of protection products. By geography, APAC will lead premium growth, contributing over USD 800 billion in new premiums.

2. Life vs Non-Life Growth Rates

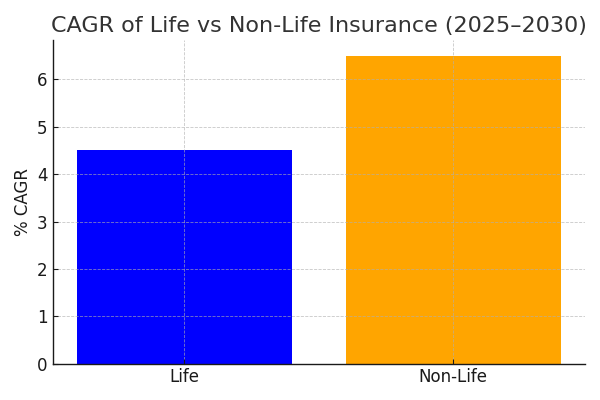

Life insurance is expected to grow at a CAGR of 4–5% during 2025–2030, supported by savings-linked products and retirement plans. Non-life will outpace at 6–7% CAGR, driven by health, motor, and cyber insurance. Non-life premiums are forecast to rise from USD 2.6 trillion in 2024 to over USD 3.7 trillion in 2030. Life premiums will grow more moderately, reaching ~USD 4.4 trillion by 2030.

3. Product Line Drivers

Health insurance premiums are expected to grow ~8% CAGR, motor at ~5%, and cyber insurance at over 15%. Property insurance is stabilizing, with climate risks pushing up pricing. Cyber will be the fastest-growing line, from USD 15 billion in 2024 to USD 35–40 billion by 2030. Health remains the anchor of non-life, projected to account for one-third of global non-life premiums by 2030.

4. Regional Market Contributions

APAC will drive >40% of incremental premium growth by 2030, fueled by China, India, and Southeast Asia. Europe will see steady but slower growth (3–4% CAGR), while the US market will expand at 4–5%, led by property & casualty. In Latin America and Africa, penetration remains low but digital-first models are unlocking demand. Regional shifts indicate insurers must localize products and adapt to regulatory frameworks to capture growth.

5. Role of Insurtech

Insurtech adoption is reducing acquisition costs by 20–25% through digital onboarding, AI-driven underwriting, and API-based distribution partnerships. Digital channels are expanding penetration in underserved markets, with APAC leading in adoption. Global insurtech funding is rebounding, expected to exceed USD 15 billion annually by 2027. By 2030, over 25% of new policy sales in non-life insurance will flow through digital-only platforms.

6. Consumer Demographics & Demand

Millennials and Gen Z are driving demand for digital-first insurance solutions, preferring non-life coverage like health, property, and cyber over traditional life insurance. Aging populations in developed markets sustain demand for annuities and retirement products. By 2030, consumers under 40 will account for ~45% of global premium growth. Lifestyle risks, urbanization, and increased health expenditures will reinforce demand for non-life products.

7. Regulatory Environment

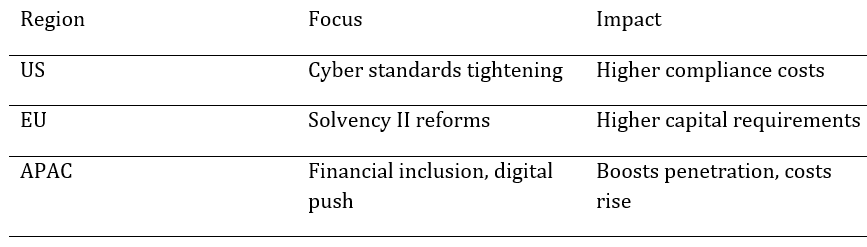

Regulatory changes will shape market economics. The EU is implementing Solvency II reforms, increasing capital requirements. The US is tightening cyber insurance standards, while APAC regulators are promoting financial inclusion and digital policies. Compliance costs are expected to rise 10–15% by 2030, especially in non-life lines with high-risk exposures. Harmonization remains a challenge, as fragmented regulations increase operational costs for global insurers.

8. Profitability Trends

Combined ratios in non-life are tightening, expected to improve from ~99% in 2024 to ~96% by 2030, driven by better pricing and automation. Life insurers face margin pressures from low interest rates but benefit from investment-linked product growth. Solvency margins are forecast to remain above 120% in developed markets, though APAC players will face capital adequacy challenges. Profitability will hinge on efficiency and digital adoption.

9. Competitive Landscape

The market is consolidating, with top 20 global insurers holding ~65% of premiums. However, insurtech challengers are eroding share in niches like digital health and cyber. US and EU incumbents are investing heavily in partnerships or acquisitions of insurtechs. APAC markets see joint ventures between insurers and tech platforms. By 2030, hybrid models combining traditional balance sheet strength with tech-driven distribution will dominate.

10. Risks & Challenges

Key risks include climate-related catastrophes, cyber-attacks, and macroeconomic shocks. Non-life insurers face rising claims costs, with climate losses alone projected to exceed USD 200 billion annually by 2030. Life insurers risk slower growth in mature markets and face reputational risks around data privacy. Regulatory fragmentation and capital adequacy remain challenges. Insurers that fail to digitize will face cost disadvantages of 20–30% compared to tech-enabled peers.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071