68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Hedge Fund Industry Size & Share Analysis – Growth Trends & Forecasts (2025–2030

This research analyzes the hedge fund industry in the US and EU from 2025 to 2030, focusing on market size, share, growth trends, and forecasts. The report evaluates assets under management (AUM), fund performance, regional adoption, and sector-specific strategies. By combining quantitative metrics with insights on emerging hedge fund strategies, fee structures, and regulatory environments, this report provides a comprehensive overview for investors, fund managers, and institutional stakeholders seeking to navigate a rapidly evolving hedge fund landscape and capitalize on growth opportunities in both regions.

What's Covered?

Report Summary

Key Takeaways

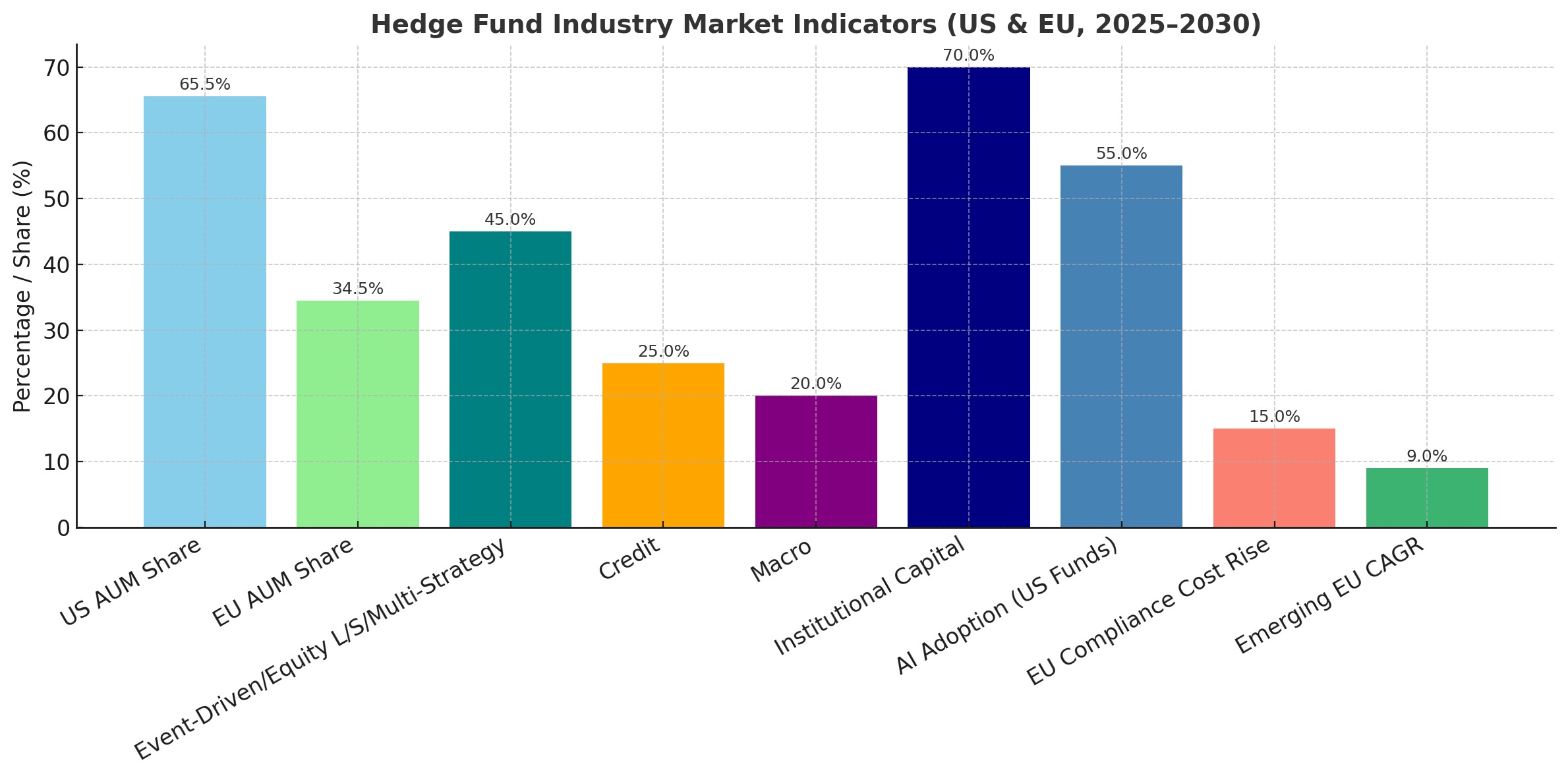

- Hedge fund AUM in the US and EU is projected to grow from $5.2 trillion in 2025 to $7.8 trillion by 2030, CAGR 8%.

- The US accounts for 65% of total AUM in 2025, increasing slightly to 66% by 2030.

- The EU contributes 35% of total AUM, rising to 34% by 2030 due to slower growth.

- Event-driven and equity long/short strategies are expected to dominate, representing 45% of total funds by 2030.

- Hedge fund fees are projected to decrease slightly, with management fees averaging 1.2% and performance fees 18%.

- Institutional investors, including pension funds and sovereign wealth funds, will account for 70% of hedge fund investments by 2030.

- Average annual returns for hedge funds are projected at 6–8%, outperforming traditional benchmarks in volatile markets.

- AI and quantitative trading adoption is expected in 55% of US hedge funds by 2030, up from 40% in 2025.

- Regulatory compliance costs are projected to rise by 15% by 2030, primarily in the EU due to stricter frameworks.

- Emerging hedge fund markets in Europe, such as Luxembourg and Ireland, are expected to grow at CAGR 9% from 2025 to 2030.

Key Metrics

Market Size & Share

The hedge fund industry in the US and EU is projected to expand significantly from $5.2 trillion in 2025 to $7.8 trillion by 2030, representing a CAGR of 8%. The US market dominates with 65% of total AUM in 2025, increasing marginally to 66% by 2030, driven by institutional demand, technological adoption, and diversified hedge fund strategies. The EU market represents 35% of total AUM, slightly decreasing to 34% by 2030, reflecting slower growth due to regulatory constraints and conservative institutional adoption. Event-driven, equity long/short, and multi-strategy funds are expected to account for 45% of total funds by 2030, emphasizing alpha generation and risk-adjusted returns. Institutional investors, including pension funds, sovereign wealth funds, and endowments, will increasingly dominate the capital base, contributing to 70% of total investments by 2030. The geographic distribution also highlights emerging hedge fund hubs in Luxembourg, Ireland, and Switzerland, projected to grow at 9% CAGR. Fund flows into AI-enabled quantitative strategies are rising, particularly in US funds, enhancing portfolio diversification and volatility management. Hedge fund fees are projected to stabilize with average management fees at 1.2% and performance fees at 18%, reflecting industry trends toward fee compression. Overall, the market is expected to benefit from increased capital inflows, innovation in trading strategies, and regulatory clarity, positioning hedge funds for sustainable growth through 2030

Market Analysis

The hedge fund industry in the US and EU demonstrates robust growth supported by diversified investment strategies, technological adoption, and increasing institutional allocations. US hedge funds account for 65–66% of the total AUM between 2025–2030, while the EU contributes 34–35%, with growth concentrated in major financial hubs such as London, Frankfurt, and Paris. Event-driven, equity long/short, and multi-strategy funds will dominate, representing approximately 45% of total hedge fund AUM by 2030, followed by credit and macro strategies at 25% and 20%, respectively. Institutional investors, including pension funds and sovereign wealth funds, are projected to provide 70% of total capital by 2030, reflecting their reliance on alternative investments to diversify risk and enhance returns. Hedge fund returns are expected to range from 6–8% annually, outperforming traditional benchmarks during volatile market conditions. The adoption of AI, machine learning, and quantitative strategies is anticipated in 55% of US hedge funds by 2030, improving trading efficiency and risk-adjusted performance. Regulatory compliance costs, especially in the EU, are projected to rise 15% by 2030, driven by stricter ESG reporting and financial transparency requirements. Emerging European markets, including Luxembourg and Ireland, are expected to grow at CAGR 9%, driven by regulatory incentives, fund domiciliation benefits, and technology adoption. Overall, hedge fund growth is underpinned by innovation, institutional adoption, and robust macroeconomic strategies.

Trends & Insights

The hedge fund industry in the US and EU is evolving rapidly, driven by institutional demand, technological adoption, and regulatory adaptation. AI and machine learning-based strategies are expected to be adopted by 55% of US hedge funds by 2030, compared to 40% in 2025, enhancing portfolio optimization, risk management, and alpha generation. Quantitative strategies, including algorithmic trading, factor-based investing, and systematic hedge fund models, will account for 30% of total hedge fund assets in the US by 2030. ESG integration is gaining traction in the EU, with 50% of EU funds incorporating ESG metrics by 2030 to align with regulatory mandates and attract sustainable capital. Average annual returns are projected at 6–8%, outperforming traditional benchmarks, particularly in volatile markets, which drives investor confidence. Fee structures are stabilizing, with management fees averaging 1.2% and performance fees 18%, reflecting a mild compression trend due to competitive pressures. Regulatory compliance costs, especially in Europe, are expected to increase 15% by 2030, while technological investment in AI, data analytics, and risk modeling is projected to rise 20% by 2030. Hedge funds are increasingly focused on portfolio diversification across equity, credit, macro, and alternative strategies. This combination of technology adoption, regulatory alignment, and institutional demand is expected to accelerate growth, increase transparency, and enhance the long-term resilience of hedge fund portfolios.

Segment Analysis

Hedge funds in the US and EU are segmented by strategy type, investor profile, and asset class allocation. Event-driven, equity long/short, and multi-strategy funds dominate, representing 45% of total assets under management (AUM) by 2030, followed by credit strategies (25%) and macro/global macro strategies (20%). Institutional investors contribute 70% of total AUM, primarily from pension funds, sovereign wealth funds, endowments, and family offices, while retail and high-net-worth individual allocations account for the remaining 30%. In terms of asset allocation, equity and fixed income dominate with 60% of combined portfolios, while alternative investments including commodities, derivatives, and tokenized assets contribute 40%. AI and quantitative strategies are projected to be implemented in 55% of US funds and 50% of EU funds by 2030, optimizing trading algorithms and risk-adjusted returns. Fee structures are gradually compressing, with management fees averaging 1.2% and performance fees at 18%, reflecting competitive dynamics. Regulatory compliance is increasingly critical in Europe, where 50% of firms will adopt AI-driven compliance platforms to manage reporting and transparency. Hedge fund segments reflect differences in risk appetite, investor mandates, and strategy sophistication, illustrating the diversity and complexity of capital allocation and performance in both US and EU markets.

Geography Analysis

The US and EU hedge fund markets display regional variations in AUM, adoption, and growth trends. In 2025, the US accounts for 65% of total hedge fund AUM, increasing to 66% by 2030, led by major financial hubs including New York, Chicago, and San Francisco. The EU represents 35% in 2025, decreasing slightly to 34% by 2030 due to stricter regulatory constraints and slower institutional adoption. Hedge fund growth in the US is driven by technology adoption, with 55% of funds implementing AI-based strategies by 2030, compared to 50% in Europe, where ESG integration and regulatory compliance are higher priorities. Emerging European hedge fund markets such as Luxembourg, Ireland, and Switzerland are projected to grow at a CAGR of 9%, benefiting from fund domiciliation incentives, tax efficiency, and regulatory alignment. Average annual returns in both regions are projected at 6–8%, with US funds outperforming slightly in volatile macroeconomic conditions due to larger allocations to quantitative and AI-driven strategies. Regulatory compliance costs in Europe are expected to increase 15% by 2030, while US compliance costs rise modestly. Geography analysis demonstrates that US funds continue to dominate AUM and strategy adoption, while European funds leverage regulatory frameworks and ESG integration to capture specialized investor segments. Regional differences impact asset allocation, portfolio strategies, and investor engagement in hedge fund markets.

Competitive Landscape

The hedge fund competitive landscape in the US and EU features traditional banks, hedge fund managers, and fintech-enabled alternative asset firms. Key US players include Bridgewater Associates, BlackRock, Citadel, and Renaissance Technologies, while European leaders include Man Group, Brevan Howard, and BlueCrest Capital. Hedge fund startups focusing on quantitative and AI-driven strategies are projected to capture 20% of the market share by 2030, particularly in the US. Traditional firms will continue to dominate, holding 50–55% of total assets in both regions, while emerging European hubs like Luxembourg and Ireland attract new fund formations due to favorable regulations. Fee structures remain competitive, with management fees averaging 1.2% and performance fees 18%, while investor demand for high transparency and ESG integration drives adoption of AI analytics. Regulatory compliance, particularly in Europe, is increasingly a differentiator; firms that adopt AI-based compliance tools gain trust and expand capital access. Technological investment in AI, big data, and trading platforms is projected to grow 20% by 2030, improving efficiency and risk-adjusted returns. Consolidation is expected as leading funds merge or partner with fintech platforms to offer end-to-end solutions. Overall, competitive advantage is determined by technology adoption, fund strategy diversity, regulatory compliance, and measurable performance, positioning early adopters to capture growing institutional and retail capital.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071