68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Fixed Income Market Size & Share Analysis - Growth Trends & Forecasts (2025–2030, US & EU)

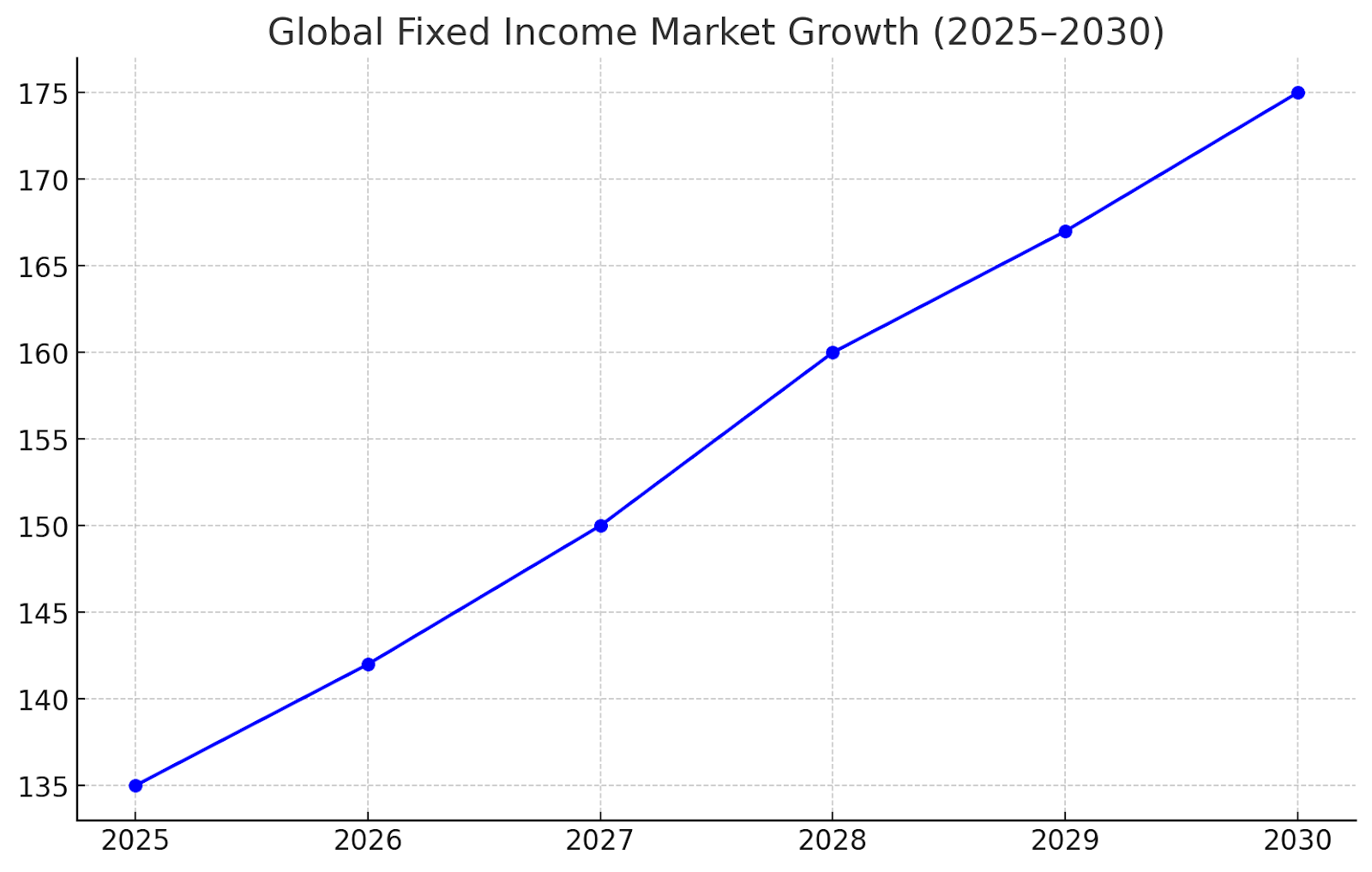

The fixed income market across the U.S. and EU is entering a phase of yield normalization, structural diversification, and digitalization. Between 2025 and 2030, total outstanding debt securities are expected to grow from $135 trillion to over $175 trillion globally, with the U.S. and EU representing 65% of issuance. Rising green and private credit instruments are reshaping investor strategies as central banks stabilize policy rates near 2.5–3%

What's Covered?

Report Summary

Market Evolution: 2025–2030 Outlook

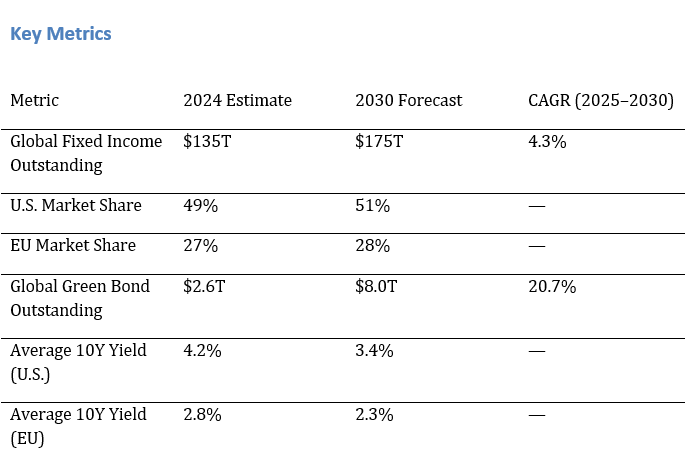

Global fixed income markets are projected to expand from $135T in 2024 to $175T by 2030, reflecting a 4.3% CAGR. The U.S. remains the anchor with over $90T in total debt securities, while the EU reaches $35T. Policy stabilization, fiscal expansion, and refinancing cycles drive issuance growth. Long-duration demand from pension and insurance funds continues, while retail access via ETFs rises 35%. China’s inclusion in global indices adds $3T incremental inflows by 2030.

Policy & Yield Dynamics

Monetary normalization defines the 2025–2030 era. The U.S. 10-year Treasury yield is expected to settle near 3.4%, while German Bunds stabilize around 2.2%. Central banks gradually unwind balance sheets while maintaining real yields positive by 50–75 bps. Inflation-linked bonds remain in high demand as CPI averages 2.3% in the U.S. and 2.0% in the EU. Fiscal resilience and credible debt management frameworks prevent sharp curve inversions.

Corporate vs Sovereign Bond Trends

Corporate debt issuance grows at 5.6% CAGR, outpacing sovereigns at 3.2%. Refinancing activity peaks in 2026–27 as high-cost pandemic-era debt matures. Financials and utilities lead issuance, while tech and healthcare maintain strong BBB/AA ratings. Investors shift to high-grade corporates as spreads compress by 60 bps vs 2024 levels. ESG-linked issuance exceeds 30% of new corporate debt by 2030, reinforcing sustainability alignment.

ESG & Green Bonds Surge

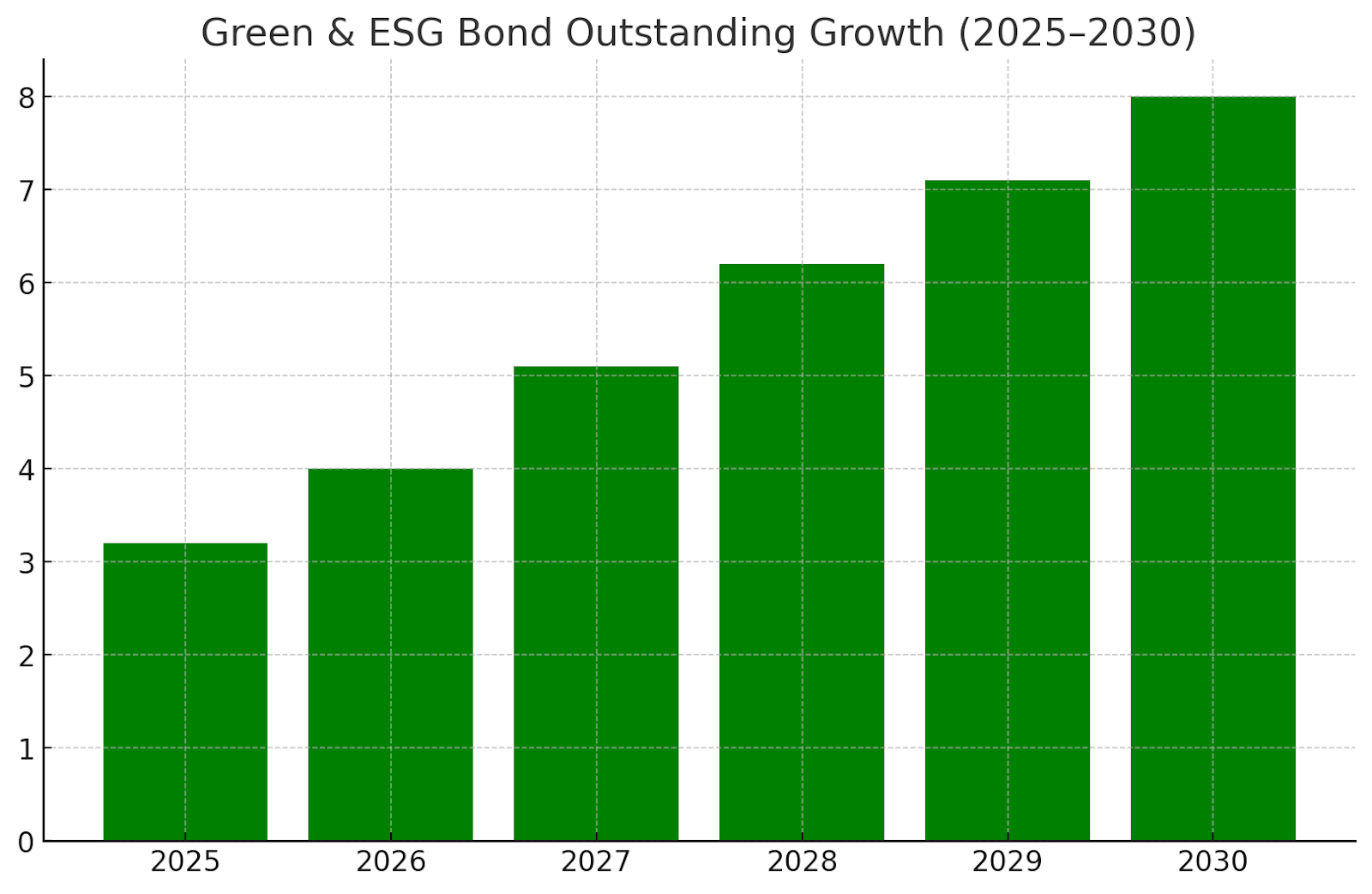

Green and sustainability-linked bonds expand from $2.6T in 2024 to $8T by 2030, representing over 12% of total issuance. The EU remains the global hub with €4.2T in outstanding ESG bonds, driven by the EU Green Bond Standard rollout in 2026. The U.S. market catches up post-2027 with municipal green issuances and corporate sustainability frameworks.

Duration & Inflation Risk Management

Investors rebalance portfolios toward shorter durations, averaging 6.2 years in 2025 vs. 7.8 years pre-2020. Inflation-linked securities (TIPS, OATi) rise 45% in outstanding value by 2030. Asset managers deploy active duration overlays to mitigate volatility as real rates normalize. Structured notes and floating-rate instruments gain traction, while central banks maintain transparency, reducing rate shock risk.

Issuance Leaders: Regions & Sectors

The U.S., EU, and Japan account for over 75% of total issuance. By sector, financials (28%), sovereigns (26%), and utilities (14%) dominate 2030 volumes. The U.S. Treasury’s $1.3T annual issuance program stabilizes supply, while EIB and EU Recovery Fund bonds anchor the EU’s supranational debt markets. Cross-border issuance grows 22% as global investors seek yield arbitrage opportunities.

Private Credit vs Public Fixed Income

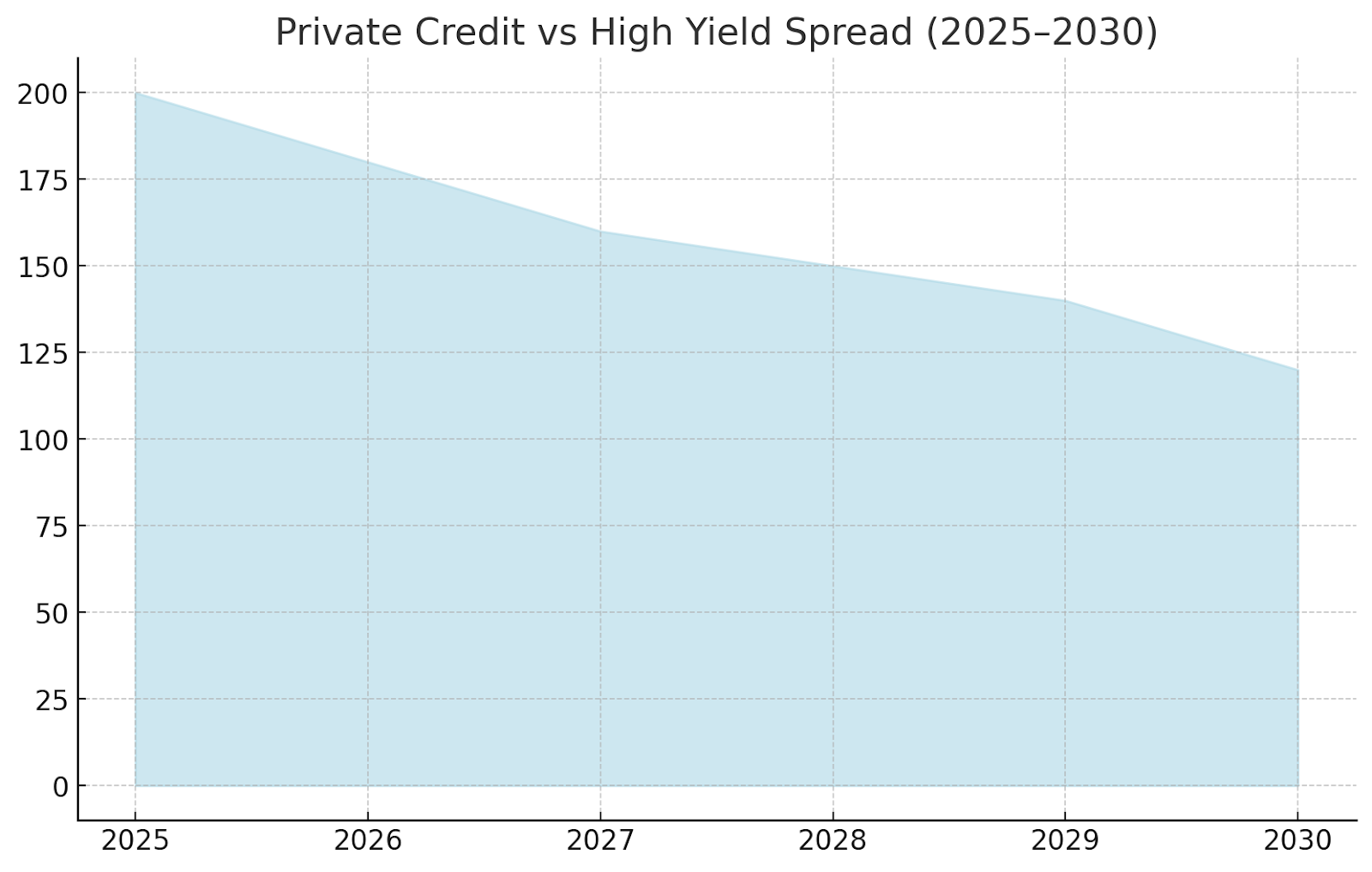

Private credit emerges as a structural competitor, reaching $3.5T AUM globally by 2030, up from $1.8T in 2024. U.S. private credit yields average 9.1%, narrowing to a 120 bps spread vs. high-yield bonds by 2030. Institutional allocations rise from 6% to 11% of total fixed income portfolios.

Tokenized & Digital Bonds

Tokenized bond pilots by the European Investment Bank and World Bank have validated digital issuance feasibility. The EU’s DLT Pilot Regime and U.S. SEC sandbox programs together are expected to facilitate over $400B tokenized debt by 2030. These instruments cut settlement times from T+2 to T+0 and reduce issuance costs by 15–20%. Adoption accelerates post-2027 as digital custodians and DeFi integrations mature.

Key Risks & Downside Scenarios

Macro risks include inflation persistence, fiscal slippage, and geopolitical shocks. A sustained energy price rebound could push 10Y yields back above 4%, tightening liquidity. Rising fiscal debt-to-GDP ratios—U.S. (115%) and EU (91%)—may trigger rating watch actions by 2028. However, greater transparency in ESG reporting and digital issuance offsets some systemic stress through improved secondary market efficiency.

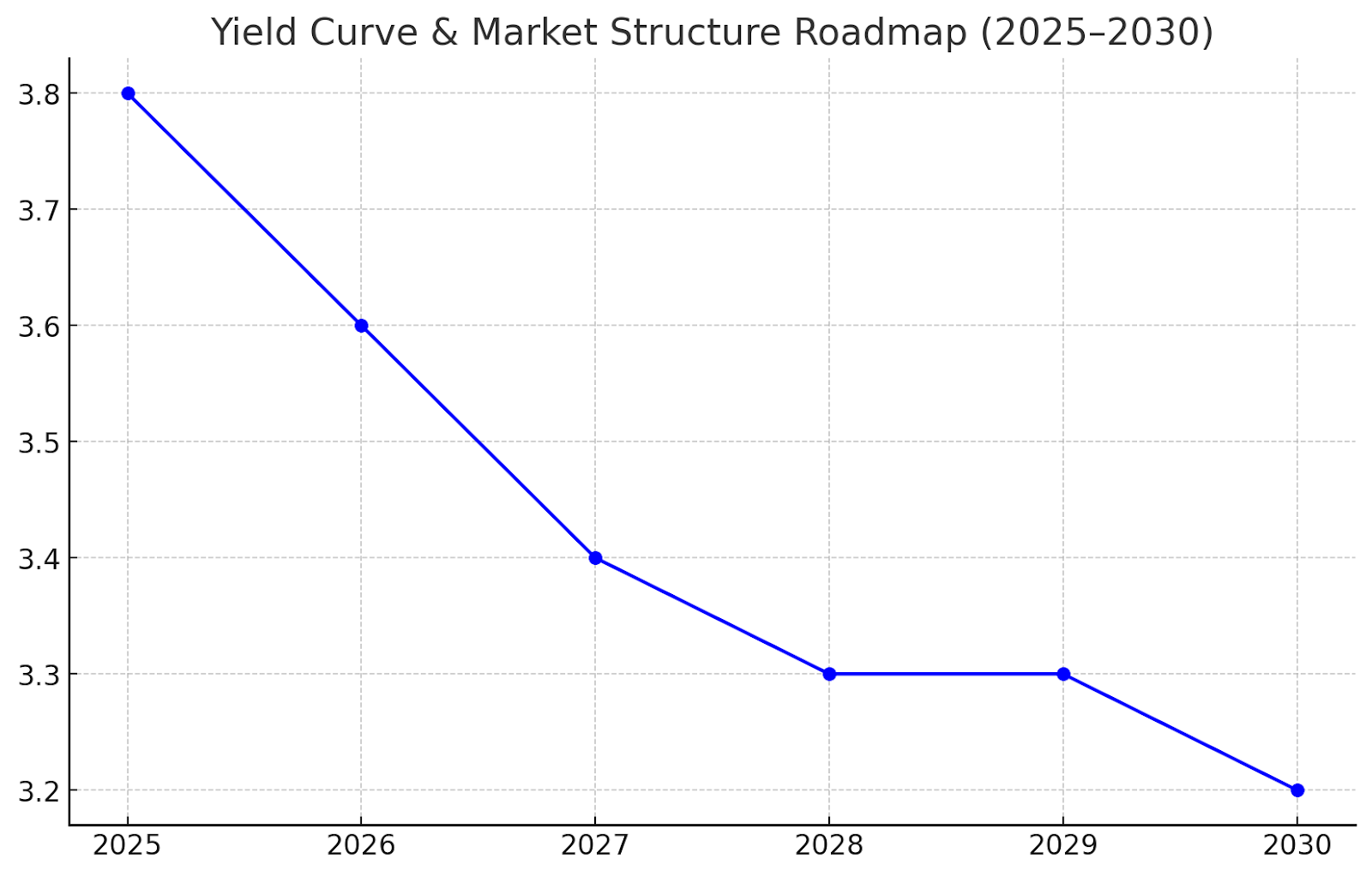

2025–2030 Yield & Structure Roadmap

The global fixed income market is expected to stabilize into a 2.5–3.0% nominal yield era, characterized by efficiency, liquidity, and ESG depth. Curve normalization completes by 2026, while digitalization enhances price discovery. Portfolio rebalancing into green, private, and tokenized segments redefines benchmark construction by 2030.

Key Takeaways

- Global fixed income outstanding to reach $175T by 2030, with U.S. at $90T and EU at $35T.

- Corporate bonds to grow faster than sovereigns, driven by refinancing and ESG-linked issuance.

- Average 10Y yields to stabilize at 3.4% (U.S.) and 2.3% (EU) by 2030.

- ESG & green bonds to cross $8T outstanding by 2030, ~12% of total issuance.

- Private credit grows 14% CAGR, narrowing spreads vs. high yield by 120 bps.

- Tokenized debt and digital bond pilots in EU and U.S. expected to exceed $400B by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071