68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Flood Barrier and Flood Resilience Technology: Retractable Systems & Climate Resilience Certifications

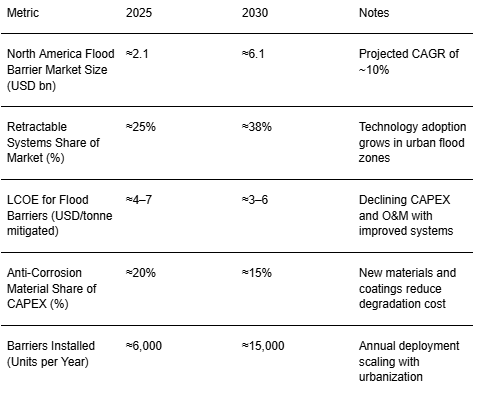

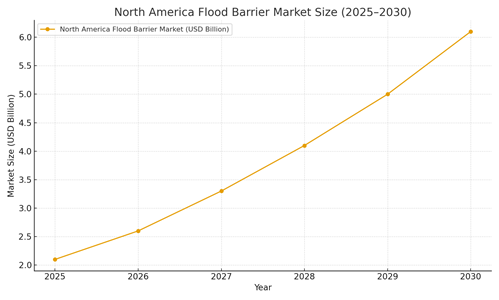

From 2025 to 2030, the North American market for flood resilience technologies will experience steady growth, driven by increasing flood risks, urbanization, and enhanced climate resilience mandates. Flood barriers especially retractable systems offer an adaptable and cost-effective solution for cities, municipalities, and utilities seeking to mitigate flood risks without permanent infrastructure. These systems will be crucial for coastal cities, flood-prone regions, and infrastructure in flood plains. Retractable flood barriers can be deployed or retracted based on flood alerts, providing rapid responses to extreme weather events while maintaining unobstructed access during dry periods. The systems use advanced corrosion-resistant materials, ensuring long-term durability and reduced maintenance costs. By 2030, technological advancements, including enhanced materials, will reduce installation and maintenance costs while improving system reliability. The market for retractable flood barriers and related resilience technologies will grow at a compounded annual growth rate (CAGR) of approximately 10% annually, reaching an estimated market size of USD 6.1 billion by 2030.

What's Covered?

Report Summary

Key Takeaways

1) Retractable flood barriers provide adaptable and cost-effective flood mitigation.

2) Market for flood barriers will grow at a CAGR of ~10% annually by 2030.

3) Urban flood zones and coastal cities will drive the bulk of demand for flood resilience technologies.

4) Technological advancements in materials will significantly reduce installation and maintenance costs.

5) Corrosion-resistant coatings and advanced materials will be key to reducing lifecycle costs.

6) Private sector adoption will rise as resilience certifications (FEMA, LEED) become key benchmarks.

7) Climate resilience certifications will become crucial for regulatory compliance and funding.

8) Retractable flood barrier systems are expected to become more scalable and energy-efficient by 2030.

Key Metrics

Market Size & Share

The flood barrier market in North America is projected to expand from approximately USD 2.1 billion in 2025 to USD 6.1 billion by 2030. Retractable flood barrier systems are expected to grow in adoption due to their ability to be deployed when needed, while minimizing impact to daily urban life. This market is driven by increasing urbanization, the rising frequency of extreme weather events, and the need for climate resilience across the U.S., Canada, and Mexico. A major contributor to this market growth is the introduction of climate resilience certifications and mandatory flood mitigation plans for new urban developments. Government regulations and private sector investment in flood resilience solutions are poised to transform the flood protection landscape.

As market adoption increases, we can expect economies of scale to reduce overall costs, particularly with advancements in anti-corrosion materials and automated monitoring systems.

Market Analysis

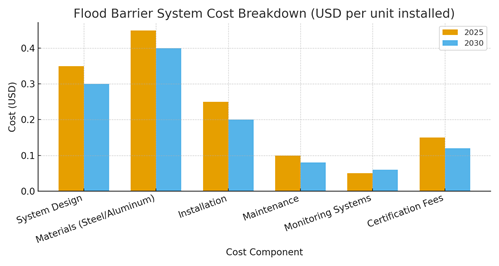

The cost breakdown of flood resilience technologies highlights the importance of materials and system design in reducing LCOE (levelized cost of effectiveness). Retractable flood barriers are more cost-effective than permanent installations, while also providing increased flexibility for urban planners. The LCOE of flood barriers is expected to decrease with improved corrosion-resistant materials and automation in barrier deployment and monitoring. Anti-corrosion coatings are small in CAPEX but material to lifecycle cost via avoided failures. Illustrative breakdowns for the year 2025 show that materials (steel/aluminum) represent the highest cost, followed by system design, installation, and maintenance. By 2030, as the technology matures, the cost of materials and installation will be reduced by approximately 10-15%.

Trends & Insights

• Increased integration of retractable flood barriers into urban development projects.

• Use of advanced corrosion-resistant materials, reducing maintenance and increasing lifecycle.

• Greater role of digital monitoring systems for automated flood response.

• Rise in private sector partnerships with municipalities to fund and implement flood resilience.

• Emergence of climate resilience certifications influencing regulatory and funding decisions.

• Modular and mobile flood resilience systems for temporary protection during extreme events.

• Focus on sustainability and minimizing environmental impact through eco-friendly materials.

Segment Analysis

The flood resilience technology market includes several key segments: urban municipalities, coastal cities, utilities, and infrastructure developers. Urban municipalities are adopting retractable systems for temporary flood protection during extreme weather events. Coastal cities are expanding permanent systems for long-term flood mitigation. Utilities are integrating flood protection into critical infrastructure, particularly in flood-prone zones. Infrastructure developers are seeking solutions for new developments, requiring compliance with mandatory flood resilience standards.

Geography Analysis

The readiness of flood resilience technologies varies across North America. The Northeast and Southeast regions show high readiness due to existing flood mitigation projects, while the West and Southwest regions are adopting these technologies more slowly due to limited access to suitable land and water resources. The Pacific Northwest has a good balance of flood resilience, but with rising population growth and development near water bodies, demand is expected to increase by 2030. Cities like New Orleans, Miami, and New York will lead in adopting flood resilience measures. Local policy support for flood mitigation and certifications will be the primary driver for market expansion, with federal funding providing an added boost.

Competitive Landscape

The competitive landscape for flood barrier technologies is diverse, with major players offering retractable and permanent solutions. Companies that provide modular, retractable flood barriers will have a competitive advantage, as they offer more flexibility for urban flood management. Key differentiators will include corrosion-resistant materials, advanced monitoring systems, and the ability to meet climate resilience certifications. Companies that form partnerships with municipalities and utilities will be better positioned to capture market share.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071