68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

EV Battery Price Collapse to $115/kWh: Margin Optimization, Supply Chain Winners & Future Cost Curves (2025–2030)

Global EV battery pack prices are projected to fall from $139/kWh in 2024 to $115/kWh by 2030, driven by cathode innovation, localized cell production, and recycling efficiencies. This decline reshapes OEM margins, reorders supplier hierarchies, and redefines the global cost curve. The report explores how automakers, suppliers, and material providers optimize margins and adapt to a maturing EV cost landscape across the U.S., EU, and Asia

What's Covered?

Report Summary

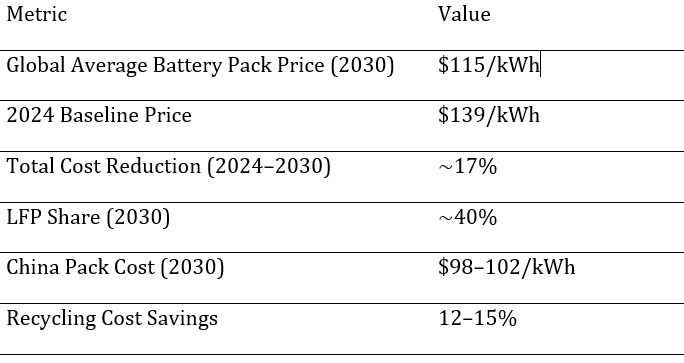

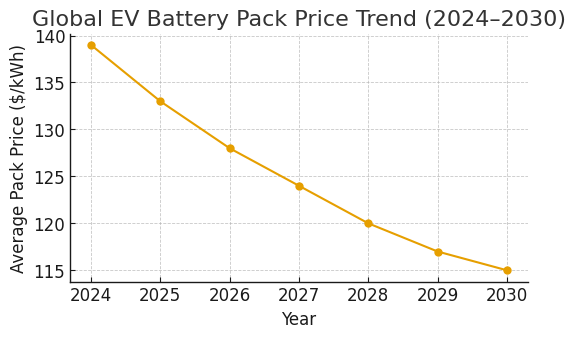

1. Global Battery Price Curve (2024–2030)

Average global battery pack prices are projected to drop from $139/kWh in 2024 to $115/kWh by 2030, reflecting economies of scale, raw material efficiency, and cathode innovation. China maintains a structural advantage due to vertical integration and lower energy costs.

2. OEM Margin Impact & Pricing Strategies

A 17% reduction in pack prices boosts OEM margins by 3–5% per vehicle, assuming partial cost pass-through. Automakers like Tesla, BYD, and Hyundai are using lower pack costs to improve affordability while sustaining profitability.

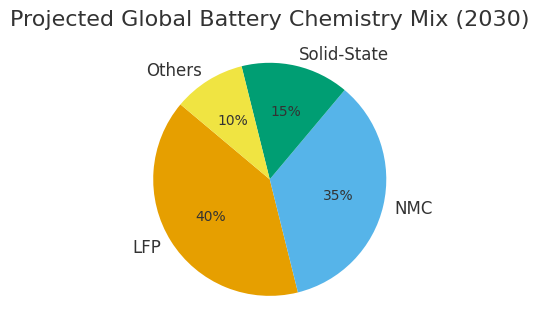

3. Dominant Battery Chemistries

LFP batteries gain significant market share due to lower costs and safety advantages, expected to reach ~40% by 2030. NMC maintains use in premium models, while solid-state R&D remains a long-term play with commercialization post-2030.

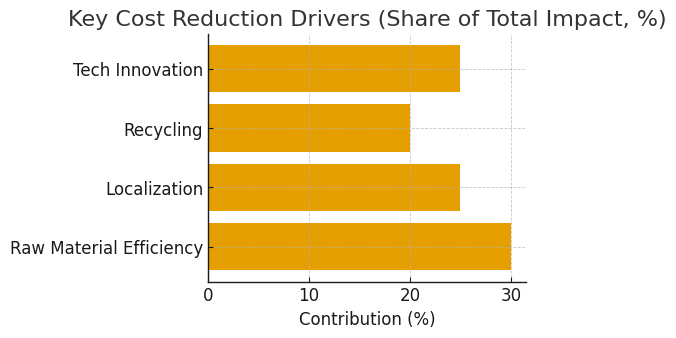

4. Cost Reduction Drivers Across Value Chain

Three key levers — raw material optimization, localization, and recycling — account for over 80% of total cost savings. Localized production in the U.S. and Europe reduces logistics and tariff costs by up to $10/kWh.

5. Recycling & Second-Life Applications

Battery recycling contributes up to 15% cost reduction through recovery of lithium, nickel, and cobalt. Companies like Redwood Materials and CATL’s recycling divisions are scaling closed-loop systems that reduce raw material dependency.

6. Supply Chain Winners

Suppliers leading in cathode production (CATL, LG Energy Solution) and LFP chemistry (BYD, Gotion High-Tech) benefit the most. Anode and separator innovations from SK On and Panasonic strengthen their position in high-energy density segments.

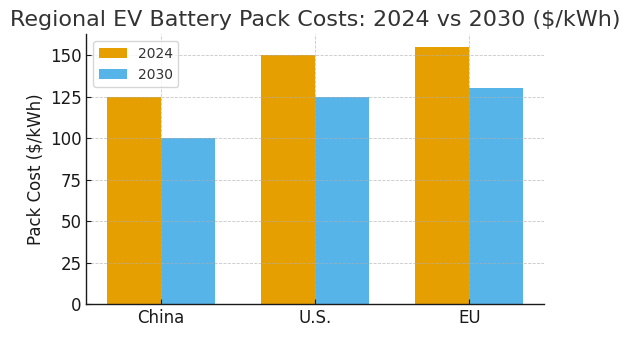

7. Regional Cost Comparison (2024–2030)

Regional disparities persist with China maintaining sub-$100/kWh packs, while U.S. and EU stabilize around $125–130/kWh due to energy and labor costs.

8. OEM Margin Optimization Levers

OEMs are leveraging in-house cell manufacturing, pack standardization, and supply contracts with miners to stabilize costs. Tesla’s 4680 cells and BYD’s blade batteries exemplify scale-driven cost efficiency.

9. Risks to Cost Decline

Key risks include raw material volatility (nickel, lithium), regulatory delays, and underinvestment in recycling infrastructure. If lithium prices spike above $35,000/ton again, cost parity could be delayed by two years.

10. Battery Chemistry Market Share (2030)

By 2030, LFP chemistry will command 40% of the global market, followed by NMC at 35%, solid-state at 15%, and others (LMFP, Sodium-ion) at 10%. This diversification improves supply resilience and cost predictability.

Key Takeaways

• Battery pack prices to fall ~17% from $139/kWh (2024) to $115/kWh (2030).

• LFP chemistry to reach ~40% market share by 2030, displacing NMC dominance.

• China sustains cost leadership with sub-$100/kWh packs by 2030.

• Recycling and second-life recovery to cut raw material costs by 12–15%.

• Localized cell production in U.S. and EU narrows cost gap by $10–15/kWh.

• Solid-state tech remains 5–7 years from commercialization but influences future curves.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071