68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Embedded Lending in SMB Platforms: Revenue Per User, Default Risk & APR Compression (2025–2030)

The embedded lending market in SMB platforms is poised for significant growth between 2025 and 2030. As SMBs continue to embrace digital financial services, embedded lending has emerged as a key enabler of their growth. This report explores key aspects of embedded lending, including revenue per user (RPU), default risk, and APR compression. By examining how SMB platforms can leverage embedded lending solutions to improve cash flow, reduce costs, and increase access to credit, we provide insights into the potential of this growing sector. The market's growth is expected to be driven by advances in AI, machine learning, and alternative credit scoring, enabling better risk management and more competitive APRs for borrowers.

.png)

What's Covered?

Report Summary

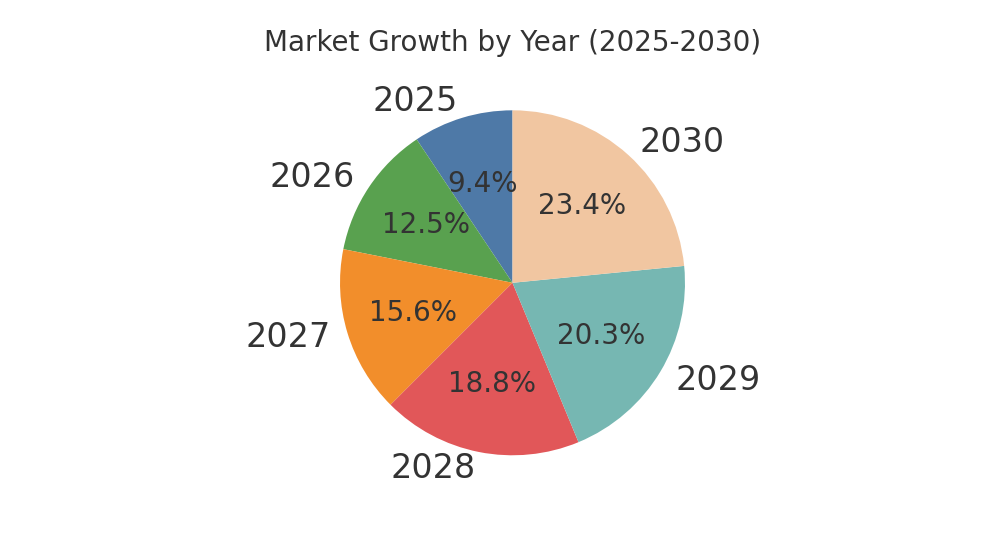

1. Market Growth & Adoption (2025–2030)

The embedded lending market for SMB platforms is expected to grow significantly from $30B in 2025 to $100B by 2030. SMBs are increasingly adopting embedded lending solutions to streamline their financial operations and offer better financing options to their customers. The rise of digital platforms and the availability of alternative data sources are key factors driving the growth of this market. Embedded lending solutions will help SMB platforms diversify their revenue streams, improving customer loyalty and engagement.

2. Revenue Per User (RPU) and Market Segmentation

Embedded lending will drive higher revenue per user (RPU) for SMB platforms by offering additional financial products and services. Platforms will be able to tap into new customer segments, particularly underserved SMBs that traditionally lack access to affordable credit. As the adoption of embedded lending solutions grows, SMB platforms will diversify their service offerings, such as providing short-term loans, credit lines, and installment payments, increasing RPU.

3. Default Risk Management & APR Compression

As embedded lending continues to evolve, platforms will leverage AI and alternative data to mitigate default risk. AI-driven risk models will enable platforms to more accurately predict creditworthiness, reducing default rates by up to 20%. APR compression will also play a crucial role in making embedded loans more affordable for SMBs. Lenders will optimize risk-based pricing models, reducing APRs by 2–4%, thus improving access to credit for SMBs while maintaining profitability.

4. Technological Innovations & Future Outlook

AI, machine learning, and alternative credit scoring are poised to revolutionize embedded lending. These technologies will enable better underwriting, leading to faster loan approvals and more personalized loan offers for SMBs. The next five years will see significant technological advancements that will improve the overall efficiency of embedded lending platforms and reduce operational costs.

5. Default Risk Management & APR Compression (Continued)

APR compression will create a more competitive lending environment for SMBs, particularly in terms of affordability. The adoption of advanced machine learning models will allow lenders to offer personalized rates based on real-time customer data, improving both access and sustainability in SMB lending.

6. Role of Strategic Partnerships

Strategic partnerships between SMB platforms and fintech companies, along with lenders, will enable seamless lending integration. These partnerships will help accelerate the adoption of embedded lending solutions and ensure that SMB platforms can offer financial products that align with customer needs while managing risk effectively.

7. Customer Adoption Drivers

As SMB platforms integrate embedded lending, consumer adoption will be driven by convenience, ease of access, and competitive terms. Borrowers will be attracted to the simplicity and speed of loan approvals and the flexibility that embedded lending provides in terms of repayment options.

8. Impact on Traditional Lending Channels

Embedded lending will disrupt traditional lending channels, enabling SMB platforms to offer quicker, more accessible financing solutions. With the integration of AI, machine learning, and data-driven lending, platforms will outpace traditional institutions in providing SMBs with the financial products they need.

9. Market Size & Spend Forecast

The embedded lending market is projected to experience a compound annual growth rate (CAGR) of over 25% between 2025 and 2030. Total spend on R&D in the embedded lending space will exceed $5B by 2030, driven by innovation in AI technologies, alternative credit scoring, and machine learning capabilities.

10. Scenarios for Embedded Lending Growth

The market's trajectory will depend on the speed of technological adoption, regulatory changes, and competitive dynamics. The base case sees steady growth driven by increasing demand for digital loans, while the bull case anticipates accelerated growth due to increased lender competition and AI-driven innovations.

Key Takeaways

- Market Growth: The embedded lending market for SMB platforms is expected to grow from $30B in 2025 to $100B by 2030.

- Revenue per User: Embedded lending will drive higher RPU for SMB platforms as they diversify their service offerings.

- Default Risk Management: Advances in AI and alternative data will help SMB platforms mitigate default risk, reducing loan defaults by up to 20%.

- APR Compression: Lenders will reduce APRs for SMB loans by optimizing risk-based pricing models, creating more competitive lending options.

- Technological Innovation: AI, machine learning, and alternative credit scoring will enable better underwriting models, reducing cost of capital for SMBs.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071