68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Embedded Insurance for Autonomous Vehicles: Usage-Based Pricing & Liability Frameworks - Innovation & R&D

Between 2025 and 2030, embedded insurance for European autonomous vehicles (AVs), led by Germany, will transition from pilots to large-scale, data-driven products. Policies—bundling liability, cyber, and downtime cover—will be embedded directly in the vehicle's software and priced in real-time using sensor data, HD-map confidence, and software-based risk. Premiums in Germany are expected to surge from EUR 180M to EUR 760M. Growth is driven by commercial fleets and OEM-embedded cover. Liability will shift to a tiered responsibility model: manufacturer (system), operator, and shared control. Claims will move to a "data-first" automated adjudication process using logs and telemetry, reducing fraud, with Germany setting the standard for data and claims protocols.

What's Covered?

Report Summary

Key Takeaways

• Usage‑based, context‑aware pricing becomes the default for AV risk.

• Tiered liability frameworks allocate risk across OEM, operator, and mixed control.

• Data‑first claims with standardized black‑box evidence compress cycle time.

• Cyber and recall coverage become integral to embedded bundles.

• Germany sets standards for evidence, safety KPIs, and OEM‑insurer contracts.

• EU harmonization accelerates cross‑border robotaxi and fleet coverage.

• Pricing models integrate ODD adherence, weather, road class, and software risk.

• Winners expose pricing/claims APIs and integrate with OTA risk management.

Key Metrics

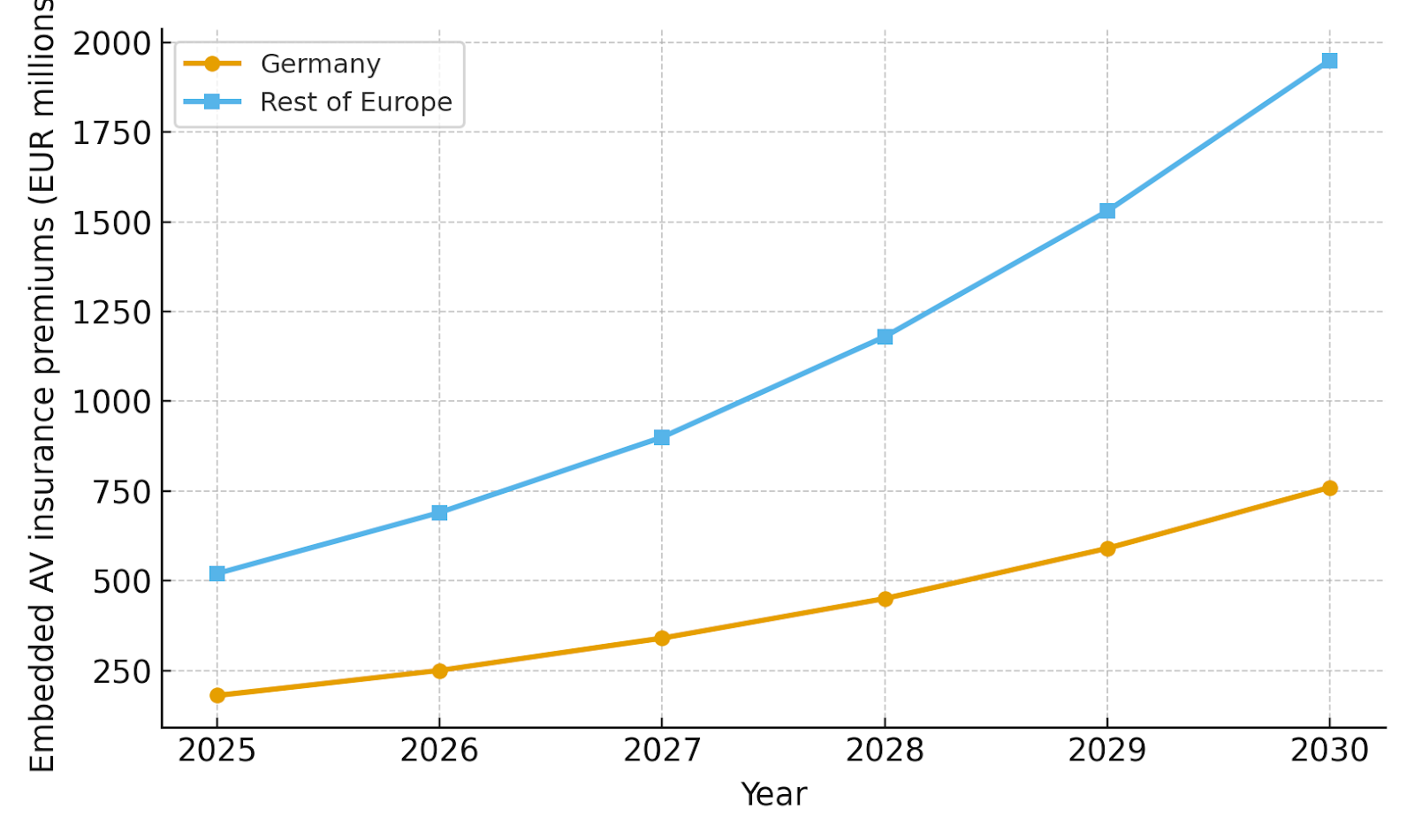

Market Size & Share

Premium growth reflects commercialization of AV pilots and OEM‑embedded cover for supervised automation features. Germany’s share is outsized early due to OEM concentration and stringent certification pathways; rest‑of‑Europe gains scale via robotaxi and logistics programs. By 2030, usage‑based policies dominate, with exposure priced per mile/minute/task and adjusted for ODD adherence, weather regimes, and road class. Share outcomes hinge on OEM distribution, fleet penetration, and regulatory clarity around manufacturer liability in automated mode.

Vendors capturing share pair transparent pricing APIs with explainable risk factors and audit‑ready evidence packs reducing friction for regulators and courts while improving reinsurer confidence.Market Analysis

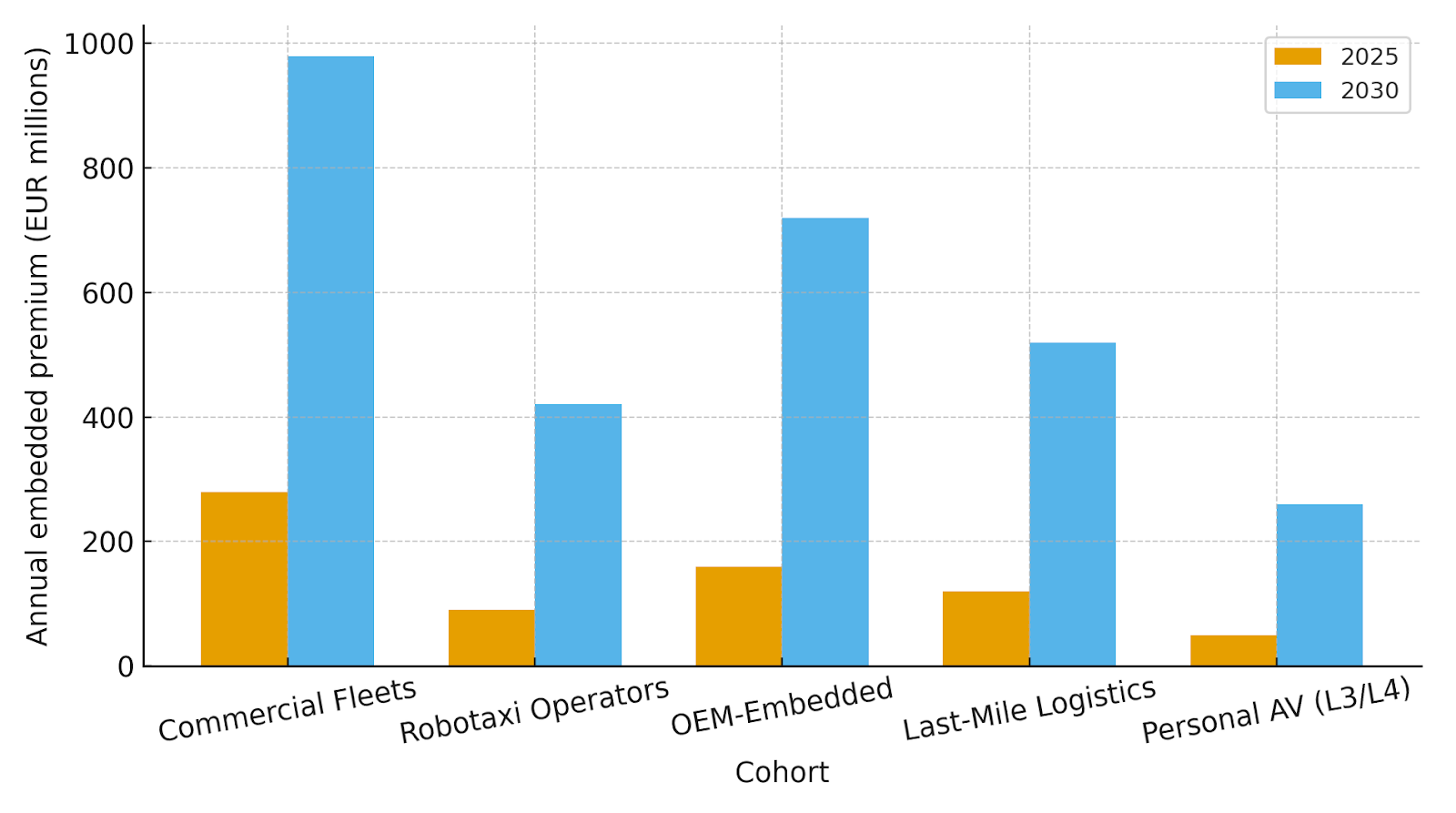

Commercial fleets lead absolute premiums as autonomous features improve safety and utilization, enabling lower per‑mile pricing with strong telematics. Robotaxi operators scale as cities issue ODD‑bounded permits; pricing incorporates exposure to dense urban scenarios and downtime risk. OEM‑embedded cover grows with factory activation for L2+/L3 features bundled into service contracts. Last‑mile logistics expands with e‑commerce density and micro‑hub operations. Personal AV (L3/L4) remains smaller but accelerates as driver‑assist transitions to limited automation on motorways.

Buyer criteria: predictable pricing with clear ODD boundaries, audit‑ready incident packs, and parametric options for severe weather. Insurers prioritize sensor quality, data provenance, and OTA responsiveness.

Trends & Insights

• Liability allocation codifies manufacturer/system responsibility in automated mode.

• Usage‑based pricing integrates ODD, weather, map confidence, and software risk.

• Claims move to data‑first adjudication with standardized black‑box evidence.

• Cyber, recall, and downtime riders attach broadly to embedded bundles.

• OTA‑aware pricing updates limits/deductibles after software changes.

• Reinsurance structures adapt to correlated software/cyber events.

• EU harmonization (type approval, product liability) lowers multi‑country friction.

• Safety KPIs (safe disengagements, incident severity) become rating inputs.

Segment Analysis

• Commercial Fleets: Highest absolute premiums; strong telematics and utilization data; multi‑coverage bundles.

• Robotaxi Operators: Urban exposure; requires incident data packs and parametric downtime cover.

• OEM‑Embedded: Bound at activation; tied to service/maintenance contracts and OTA pipelines.

• Last‑Mile Logistics: Dense stops; priced by task/time windows; integrates depot micro‑hub risk.

• Personal AV (L3/L4): Early stage; motorway ODD with supervised modes; premium add‑ons for cyber/recall.

Success factors: evidence standards, OTA responsiveness, and transparent pricing rules.

Geography Analysis

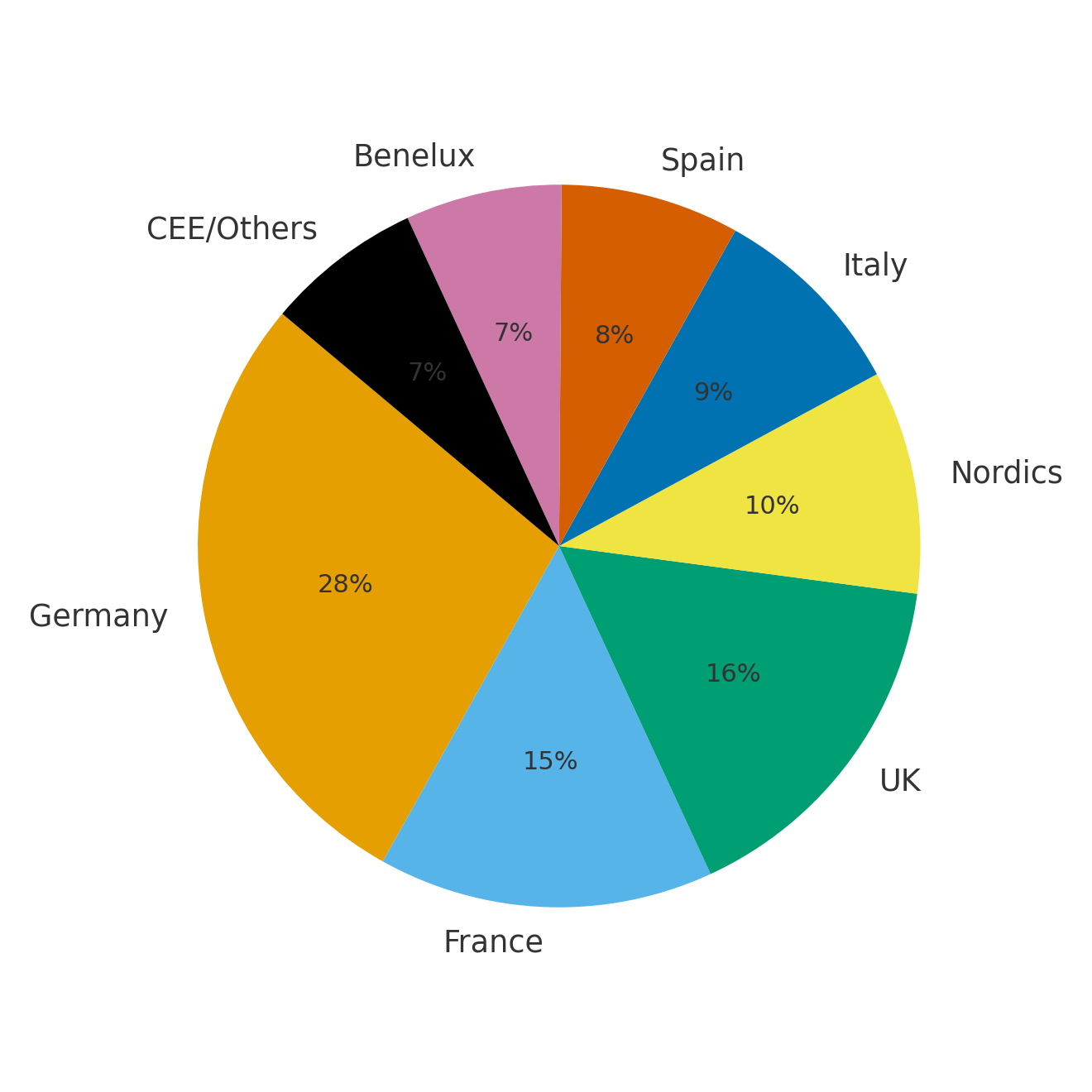

Germany leads (~28%) given OEM density and certification pathways; the UK (~16%) and France (~15%) follow with robotaxi and fleet pilots; Nordics (~10%) benefit from high ADAS uptake and digital infrastructure; Italy (~9%) and Spain (~8%) scale with logistics and motorway ODD; Benelux (~7%) and CEE/Others (~7%) contribute through corridor programs and cross‑border logistics. Geography influences liability interpretation and data‑sharing rules, but harmonized EU guidance reduces fragmentation in policy language and claims evidence.

Competitive Landscape

The field spans (1) OEM‑insurer partnerships; (2) fleet/robotaxi platform policies; (3) specialty carriers for cyber/product liability; and (4) claims/telematics vendors. Differentiation: explainable pricing, evidence standards, OTA responsiveness, and reinsurer trust. Expect consolidation around platforms that bundle usage‑based pricing, liability orchestration, and automated claims—with APIs consumable by OEMs and fleet orchestrators.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071