68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Electric Bus Battery Swapping and EV Fleet Electrification Management: Modular Infrastructure & Second-Life Applications

Between 2025 and 2030, North American fleet electrification for buses will diversify beyond depot charging toward hybrid portfolios that include battery swapping and advanced charge management. Battery swapping addresses high‑utilization, schedule‑tight duty cycles by decoupling energy replenishment from the vehicle dwell window enabling sub‑10‑minute turnarounds and higher asset availability. Managed depot and on‑route charging anchor lower‑capex transitions where dwell time is ample and grid capacity is sufficient. A modular approach standardized packs, containerized swap bays, mobile transformers, software‑defined charging lets agencies and private operators stage capex while scaling operational uptime. Economically, total cost of ownership (TCO) depends on energy price, battery procurement/lease model, infrastructure annuitization, and downtime. Swapping tends to raise battery/lease line items but can reduce downtime and on‑route delays, improving miles‑per‑day throughput; depot fast charging lowers battery inventory but may require costly grid upgrades and peak‑demand management.

What's Covered?

Report Summary

Key Takeaways

1) Match infrastructure to duty cycles: swapping for tight schedules; managed charging for ample layovers.

2) BaaS and availability‑based SLAs align incentives and de‑risk battery performance.

3) Second‑life storage at depots reduces demand charges and boosts resilience.

4) Modular, containerized swap bays shorten deployment and enable relocations.

5) Digital fleet‑energy platforms optimize SOC windows, thermal limits, and tariffs.

6) Standardized packs/connectors are critical for interoperability and vendor flexibility.

7) Design for grid constraints early transformers, feeders, and storage buffers are gating items.

8) Procure performance: uptime SLAs, swap/charge KPIs, and battery‑health warranties.

Key Metrics

Market Size & Share

North America’s e‑bus electrification is shifting toward diversified infrastructure portfolios. Our illustrative adoption curves show buses served by swapping hubs rising from ~2,000 in 2025 to ~22,000 by 2030, while managed‑charging buses expand from ~15,000 to ~62,000. Market share of swapping concentrates in high‑frequency BRT and airport/commuter corridors where tight schedules and predictable routes make fast turnarounds valuable. Managed depot charging dominates municipal and school fleets with longer layovers. Private operators and airport authorities are early adopters of swapping due to uptime economics and controlled operating environments.

Share evolution hinges on (1) standardization of pack formats and high‑power connectors; (2) availability of depot real estate for containerized swap bays; (3) tariff structures and demand‑charge mitigation; and (4) financing models (BaaS, ESaaS) that convert capex to opex. Vendors with modular, relocatable assets and battery‑health analytics capture framework agreements as agencies expand from pilots to full depots.

Market Analysis

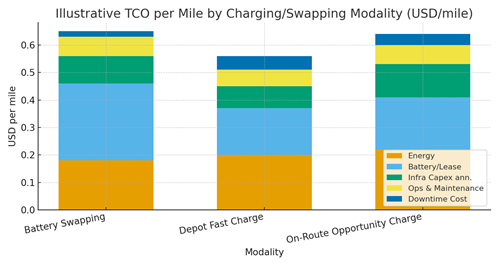

TCO per mile is the decisive metric for modality selection. Our illustrative stack shows swapping with higher battery/lease costs offset by lower downtime and higher asset utilization; depot fast charging keeps battery inventory lower but may incur peak‑demand penalties and interconnection capex; on‑route opportunity charging suits medium‑frequency corridors but adds infrastructure complexity. The optimal mix varies by duty cycle, tariff, climate, and real‑estate constraints.

Risk levers include battery degradation, safety, and grid constraints. Mitigations: standardized thermal management at swap bays, SOC window enforcement, second‑life buffers for peak shaving, and predictive maintenance on connectors and lifts. Contract structures should include availability SLAs, swap cycle limits, SOH thresholds, and energy price pass‑throughs with guardrails.

Trends & Insights (2025–2030)

Standardized packs and interfaces enable multi‑OEM swapping ecosystems; retrofits for legacy buses expand optionality. Second‑life batteries mature with health diagnostics and warranties, unlocking stationary storage at depots. Digital fleet‑energy platforms move from scheduling to predictive optimization that coordinates duty cycles, SOC windows, thermal limits, and energy markets. Safety engineering interlocks, fire detection, ventilation becomes a procurement focus. Financing evolves toward BaaS/ESaaS with outcome‑based SLAs tied to uptime and battery health. Interconnection constraints push more projects toward behind‑the‑meter storage and mobile substation solutions.

Segment Analysis (Buyer Profiles)

Municipal Transit: favors depot managed charging with selective swapping on high‑frequency routes; values predictable TCO and safety certifications. School Districts: long dwell windows and low daily miles favor depot charging; second‑life storage helps demand management. Airports & Private Operators: uptime‑sensitive routes and controlled depots make swapping attractive; BaaS simplifies financing. Campus/Corporate Shuttles: small depots and fixed loops enable modular swapping pilots. Contracted Fleet Operators: prioritize portability of assets and vendor‑neutral standards to avoid lock‑in.

Geography Analysis (USA & North America)

Readiness is strongest in the US West and Northeast where policy support, energy programs, and mature operators converge. The South/Gulf region ranks high for depot real estate and duty‑cycle fit; Canada’s leading provinces combine policy with grid programs and cold‑weather engineering. The Midwest shows solid depot capacity but faces grid upgrades in older districts. Mexico’s northeast corridors are emerging with industrial demand and cross‑border logistics. Multi‑region operators should stagger deployments according to interconnection timelines, depot real estate, and policy funding windows.

Competitive Landscape (Ecosystem & Intermediaries)

The ecosystem spans bus OEMs, battery and BMS vendors, swap‑bay automation providers, charger OEMs, software platforms, financiers, and second‑life integrators. Differentiation centers on standardized pack interfaces, safety certifications, asset‑light modularity, and digital optimization. Vendors offering BaaS/ESaaS with availability guarantees, battery‑health analytics, and second‑life take‑back programs will win share. Partnerships between OEMs, utilities, and financiers are shaping bundled offerings that compress time‑to‑service and lower perceived risk for agencies.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071