68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Direct Air Capture (DAC) Optimization Pathways: Modular Systems & Carbon Credit Monetization

Between 2025 and 2030, Direct Air Capture (DAC) in Germany and Europe will move from early pilots to modular, multi‑site deployments as developers standardize skids, drive down energy intensity, and secure offtake through premium carbon‑removal credits. The optimization frontier spans three dimensions: (1) modular systems engineering factory‑built sorbent/solvent units with heat integration and load‑following to match variable renewables and waste‑heat; (2) CO₂ logistics and storage third‑party transport and saline storage (or mineralization) with transparent metering and MRV; and (3) monetization credit stacking where policies allow, index‑linked contracts, and forward offtake that underwrites scale‑up. Cost trajectories depend on learning curves in capex, sorbent life, heat recovery, and power sourcing. Illustrative LCOR moves from ~€260–€310/t in 2025 toward ~€220–€260/t by 2030 at advantaged European sites using low‑carbon electricity and low‑grade heat; best‑case clusters with surplus heat and proximate storage achieve the lower end. MRV digitization continuous flow metering, sensorized canisters, and satellite/ledger reconciliation reduces verification lag and increases buyer confidence.

What's Covered?

Report Summary

Key Takeaways

1) Modular DAC skids shorten time‑to‑COD and enable factory learning curves.

2) LCOR falls with capex learning, sorbent longevity, and low‑carbon heat/power sourcing.

3) MRV digitization (sensors + satellite + ledgers) improves auditability and claim value.

4) Third‑party CO₂ transport & storage contracts de‑risk projects and accelerate scale.

5) Engineered‑removal credits command durable premiums; index‑linked offtake manages price risk.

6) Article 6‑ready documentation strengthens cross‑border claims and reduces reputational risk.

7) Germany’s edge: manufacturing and systems integration; storage leveraged via North Sea hubs.

8) Hybrid revenue stacks (credits + offtake + public funding) unlock bankable financing.

Key Metrics

Market Size & Share

Europe’s DAC market is set to scale via modular deployments clustered around low‑carbon power and CO₂ storage hubs. Our illustrative scenario shows installed capacity rising from ~150 ktCO₂/yr in 2025 to ~1.3 MtCO₂/yr by 2030, contingent on PPA availability, storage access, and credit market depth. Early share accrues to the Nordics, UK & Ireland, and Benelux given North Sea storage proximity and policy support; Germany captures significant share through manufacturing, systems integration, and cross‑border storage linkage. France, Italy, and Iberia gain momentum via waste‑heat integration and regional funding.

Share allocation depends on (1) low‑carbon electricity and heat access; (2) transport & storage capacity and tariffs; (3) permitting cadence and land footprint; (4) offtake credit quality and indexation terms; and (5) sorbent/solvent platform maturity. Developers with standardized modules and bankable T&S contracts should capture framework agreements and accelerate replication across sites.

Market Analysis

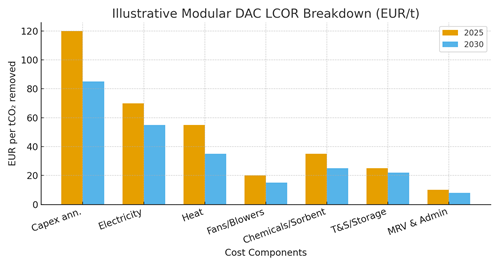

Modular DAC LCOR is driven by capex annuitization, electricity and heat costs, sorbent life, and CO₂ logistics. Our illustrative breakdown indicates movement from ~€315/t (2025 stack) toward ~€240/t (2030 stack) in advantaged sites, with the largest reductions from capex learning, heat integration, and electricity procurement. Fans/blowers and chemicals decline with design optimization and extended sorbent life. Transport & storage costs moderate with hub development and tariff transparency; MRV/admin costs shrink as digital verification scales.

Risk mitigants: multi‑year PPAs with green baseload or nuclear; heat‑recovery integration; third‑party T&S with availability clauses; MRV SLAs with data access; and indexed offtake with quality ratchets (price step‑ups upon integrity upgrades). Contract structures should pre‑define remedies for methodology updates, rating downgrades, or delivery delays (replacement rights/buffers).

Trends & Insights

Factory modularization compresses commissioning timelines and enables learning‑by‑replication. MRV digitization (sensors, satellite, ledgers) becomes standard, reducing verification lag and enhancing claim value. Article 6 adoption expands for select bilateral flows; corresponding adjustments improve cross‑border claims. Credit markets maintain strong premiums for engineered removals; index‑linked offtake and milestone‑based payments spread. Waste‑heat coupling, heat pumps, and electrified low‑grade heat reduce LCOR variability; flexible operation matches RES profiles. Expect consolidation among vendors, with platform players offering standardized modules, T&S partnerships, and assurance‑ready MRV packages.

Segment Analysis

Industrial emitters pursue DAC for contribution claims and scope‑balancing, co‑locating with low‑carbon power and waste‑heat; utilities explore DAC as grid‑balancing load with offtake to corporate buyers; technology and financial firms sign long‑dated removal contracts to meet net‑zero milestones; municipalities pilot DAC linked to district heat and education hubs. EPCs and OEMs package modular plants with O&M, MRV, and T&S contracts, enabling developers to focus on offtake and financing.

Geography Analysis

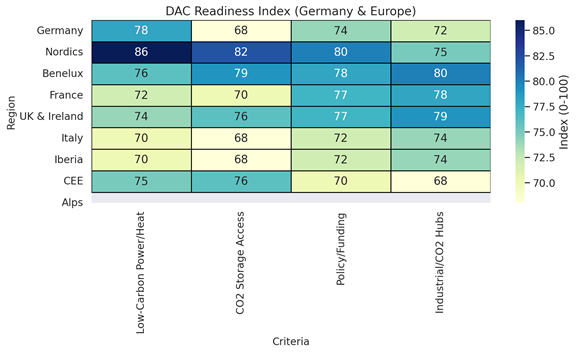

Readiness is strongest in the Nordics, UK & Ireland, and Benelux thanks to abundant low‑carbon electricity, maturing North Sea storage, and industrial hubs. Germany follows closely with manufacturing and integration strengths, leveraging cross‑border T&S to the North Sea. France and the Alps show opportunities around nuclear/RES and waste‑heat; Italy and Iberia build momentum via regional funds and mineralization pilots. CEE is earlier‑stage but improving under EU‑wide standards. Multi‑country portfolios should ladder deployments to align with storage access, PPAs, and permitting cadence.

Competitive Landscape

The ecosystem includes DAC platform vendors (sorbent/solvent), systems integrators, power/heat providers, CO₂ T&S operators, MRV technology firms, and credit marketplaces/ratings. Competitive advantage derives from module standardization, energy integration, MRV assurance, and de‑risked T&S. Vendors that offer outcome‑based contracts (availability, capture‑rate warranties), index‑linked offtake toolkits, and Article 6‑ready documentation will win enterprise buyers. Expect platformization: bundled supply (modules), services (O&M, MRV), and logistics (T&S) with replicable playbooks across European hubs.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071