68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital Wallet Saturation in the U.S. & EU: Active User Growth, Merchant Adoption & Per-Transaction Margins (2025–2030)

The digital wallet market in the U.S. and Europe is approaching saturation, with growth shifting from user acquisition to transactional profitability and ecosystem expansion. The market is expected to grow from $680B in 2025 to $1.25T by 2030 (CAGR 13.2%). By 2030, 85% of adults in both regions will use at least one digital wallet, and merchant adoption will surpass 90%. However, declining per-transaction margins, averaging 0.8%, are forcing providers to innovate with value-added services, AI-driven personalization, and embedded financial products to sustain growth and improve profitability.

What's Covered?

Report Summary

Key Takeaways

- Market size: $680B → $1.25T (CAGR 13.2%).

- Active digital wallet users to reach 540M in the U.S. and EU by 2030.

- 85% adult penetration rate across both regions.

- Merchant adoption to exceed 90% by 2030.

- Per-transaction margins to decline to 0.8%, down from 1.2% in 2025.

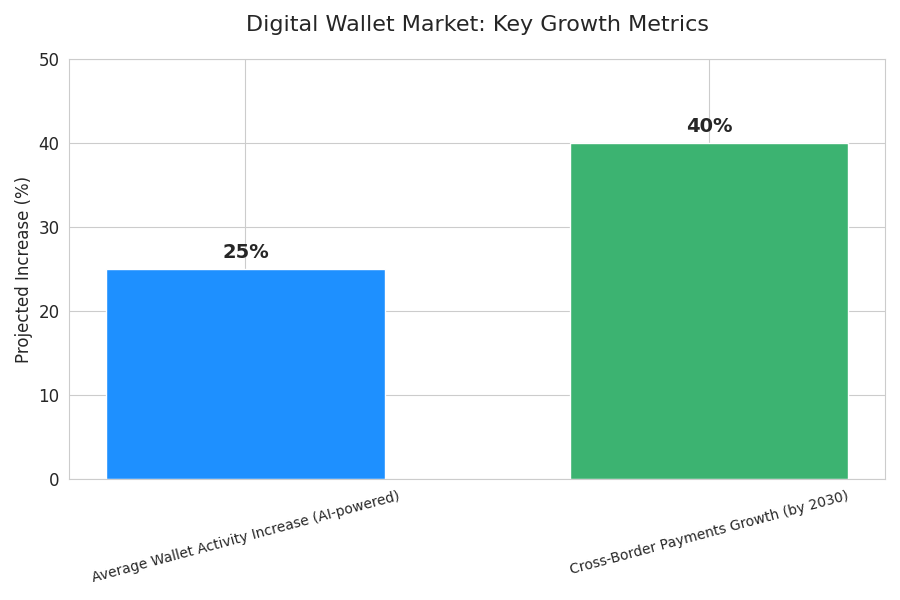

- Cross-border digital wallet payments to grow by 40%.

- AI and data analytics to enhance personalized offers, boosting transaction volumes by 25%.

- Contactless transactions to represent 70% of in-store digital wallet usage by 2030.

- Embedded finance products to contribute $60B in new revenue streams.

- Regulatory alignment under PSD3 and DORA to improve trust and interoperability.

Key Metrics

Market Size & Share

The digital wallet market in the U.S. and Europe is projected to grow from $680B in 2025 to $1.25T by 2030, achieving a CAGR of 13.2%. User growth is approaching its ceiling, with 85% of adults in both regions expected to use at least one digital wallet by 2030. The U.S. currently accounts for 60% of transaction value, while Europe, driven by regulatory clarity under PSD3, represents 40%. Merchant acceptance is expected to exceed 90%, led by SMEs adopting omnichannel payment systems. However, per-transaction margins will decline from 1.2% in 2025 to 0.8% by 2030 due to increased competition and interchange fee caps. To counter margin compression, providers are pivoting to value-added ecosystems such as buy-now-pay-later (BNPL) integrations, AI-led offer engines, and cross-border remittance functionalities that add transactional volume and customer stickiness.

Market Analysis

The market is transitioning from adoption-driven growth to profitability and retention. As user penetration nears saturation, digital wallet providers are focusing on expanding use cases—from in-store transactions to microloans, insurance products, and digital identity services. AI-powered analytics are enhancing behavioral targeting, increasing average wallet activity by 25%. Cross-border payments are emerging as a key differentiator, with 40% growth expected by 2030 as U.S. and EU payment infrastructures achieve greater interoperability. Meanwhile, regulatory harmonization under PSD3, DORA, and U.S. Consumer Financial Protection frameworks will establish data transparency and security protocols. As profitability margins shrink, digital wallet firms are prioritizing efficiency, automation, and embedded finance to sustain long-term scalability.

Trends & Insights

- Market Maturity: User growth stabilizing; focus shifts to transactional value optimization.

- AI Personalization: Driving 25% increase in user engagement through targeted rewards.

- Merchant Acceptance: Over 90% of U.S. and EU retailers integrated with wallet systems.

- Cross-Border Enablement: 40% increase in international wallet transactions.

- Falling Margins: 0.8% average per-transaction margin projected by 2030.

- Embedded Finance: Expected to generate $60B in new revenue across the ecosystem.

- Contactless Dominance: 70% of all in-store payments to be tap-to-pay.

- Regulatory Push: PSD3 and DORA ensuring interoperability and consumer protection.

- Data Monetization: Wallets monetizing anonymized transaction data for merchant insights.

- Sustainability Tie-Ins: Carbon-tracking wallets gaining traction among Gen Z consumers.

These trends underscore how digital wallets are shifting from user acquisition to ecosystem monetization, emphasizing AI, interoperability, and data-driven personalization to sustain growth.

Segment Analysis

The digital wallet ecosystem can be segmented into consumer wallets (45%), merchant solutions (30%), cross-border and remittance services (15%), and embedded finance integrations (10%). Consumer wallets, such as Apple Pay, Google Pay, and PayPal, dominate with 45% share, focusing on user retention through loyalty programs and AI-driven insights. Merchant solutions make up 30%, emphasizing omnichannel acceptance and data analytics for sales optimization. Cross-border payments, representing 15%, are growing rapidly due to interoperable networks between the U.S. and EU. Finally, embedded finance, contributing 10%, enables wallets to offer micro-investments, insurance, and credit solutions, strengthening user ecosystems and increasing profitability per user.

Geography Analysis

The U.S. holds 60% of the total market, driven by Apple Pay, PayPal, Venmo, and Cash App, which dominate the consumer segment. Europe, accounting for 40%, is experiencing rapid growth due to EU-driven interoperability mandates under PSD3 and cross-border payment frameworks. Germany, France, and the Nordic countries are leading merchant adoption, while Southern Europe is catching up through government-led cashless economy initiatives. By 2030, EU digital wallet penetration will reach 88%, surpassing the U.S. at 82%, although the latter will maintain a higher transactional value per user due to premium usage and cross-financial integrations.

Competitive Landscape

Major players in the digital wallet ecosystem include Apple Pay, Google Pay, PayPal, Amazon Pay, and Revolut, alongside European challengers such as Klarna, Wise, and N26. Apple Pay continues to dominate with 45% of mobile wallet transactions in the U.S., while PayPal holds a leading role in e-commerce payments across both regions. European fintechs like Revolut and Klarna are expanding into cross-border payments and embedded financial services, driving innovation through AI-powered user engagement tools. Competitive differentiation increasingly relies on ecosystem integration, AI analytics, and merchant partnerships, as transaction margins narrow. Over the next five years, strategic mergers and regulatory convergence will shape a consolidated, high-efficiency wallet market across the U.S. and EU.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071