68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Digital Inheritance Platforms: Estate Planning Automation & Cryptocurrency Succession - Regulatory Impact

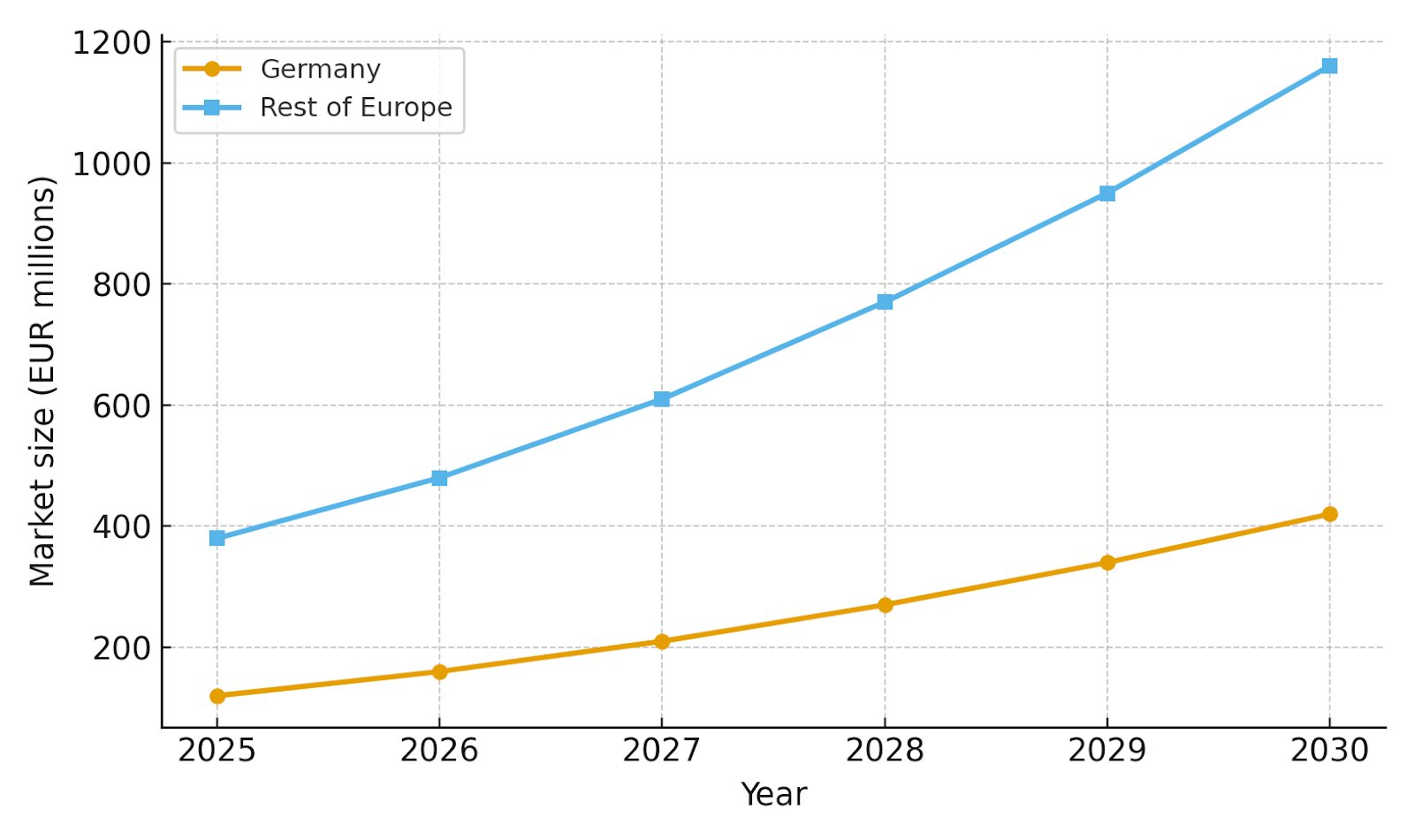

Between 2025 and 2030, Europe—especially Germany—will rapidly adopt digital inheritance platforms to automate estate management and formalize crypto succession. Aging populations, digitized finances, and regulatory pressure are driving banks, law firms, and crypto custodians to leverage platforms with identity verification, asset vaulting, event-driven controls, and compliant execution. Germany’s market may grow from EUR 120M to EUR 420M, while the rest of Europe expands from EUR 380M to EUR 1.16B. Growth is fastest among financial institutions embedding inheritance functions, with eIDAS 2.0, PSD2/3, and GDPR supporting cross-border scaling, privacy, and legal certainty.

What's Covered?

Report Summary

Key Takeaways

• Aging demographics + digitized assets make inheritance automation inevitable.

• Germany sets enterprise‑grade benchmarks for EU rollout and legal defensibility.

• APIs to courts, notaries, banks, and custody cores are the critical moat.

• Crypto succession hinges on qualified custody + threshold recovery + privacy.

• Programmable fiduciary controls reduce disputes and execution errors.

• Identity (eIDAS2) and open finance (PSD2/3) unlock cross‑border scale.

• Insurers and banks become primary distribution for mass adoption.

• Evidence, explainability, and data governance drive regulator trust.

Key Metrics

Market Size & Share

Germany’s digital inheritance market expands from ~EUR 120M (2025) to ~EUR 420M (2030), while the rest of Europe grows from ~EUR 380M to ~EUR 1.16B. Growth is front‑loaded by legal‑tech upgrades in law firms and notary networks, then accelerates as banks, insurers, and crypto custodians embed inheritance triggers into core products. Share remains fragmented: Germany commands outsized influence in standards and legal defensibility, while larger absolute volumes accrue across France, the UK, Nordics, Italy, and Spain as distribution scales through financial institutions. By 2030, platforms with reference integrations to courts/registries and custody cores hold advantage.

Winning share drivers include: (i) repeatable connectors to public registries and eID services; (ii) enterprise custody integrations for crypto; (iii) explainable automation and audit trails; and (iv) channel partnerships with banks/insurers. Vendor lock‑in is achieved through data models, policy engines (beneficiary rules, holds), and lifecycle orchestration that spans onboarding, event triggers, review, execution, and reporting.

Market Analysis

Spend is concentrated in five cohorts. Law firms/notaries modernize probate tooling and digitize testament/mandate workflows. Banks/wealth embed inheritance modules into retail and private banking, linking account access rules to verified life events. Crypto exchanges/custodians productize succession—qualified custody, beneficiary designation, and time‑locked recovery—reducing key‑loss risk. InsurTech/life insurers integrate claims automation and beneficiary verification; consumer platforms (neo‑banks, big tech vaults) drive mass adoption through bundled ‘digital safe‑deposit’ offerings. Germany’s cohort mix skews toward legal actors early; by 2030, financial institutions dominate incremental spend across Europe as integration patterns solidify.

Buying determinants: (1) legal defensibility and evidence standards; (2) custody/crypto capabilities (threshold schemes, MPC, HSMs); (3) integration breadth (courts, registries, banks, chains); (4) explainability and supervisory visibility; and (5) operating cost reduction (cycle time, dispute rates, leakage).

Trends & Insights

• eIDAS 2.0 + EU Digital Identity Wallets enable cross‑border recognition of identities and signatures.

• Open finance (PSD2/3) supports controlled data portability for asset discovery and entitlement checks.

• Crypto succession matures via qualified custody, threshold schemes, and programmable recovery.

• Court/notary APIs and registry connectors standardize evidence exchange and status updates.

• Explainable automation and audit trails reduce litigation and increase trust.

• Privacy‑by‑design architectures (GDPR) with purpose binding and minimization become table stakes.

• Insurer/bank distribution outpaces direct‑to‑consumer for complex estates.

• Cross‑border estate complexity creates demand for templates and multilingual workflows.

Segment Analysis

• Law Firms/Notaries: Digitize intake, mandate management, testament storage, and court filings; require audit‑ready evidence and chain‑of‑custody.

• Banks & Wealth: Embed beneficiary rules, event triggers, and access controls; integrate with KYC/AML and account switching; productize premium tiers for complex estates.

• Crypto Exchanges/Custody: Offer beneficiary designation, threshold recovery, and estate verification APIs; align with qualified custody rules and data‑minimization.

• InsurTech/Life: Automate claims payout with identity and beneficiary checks; integrate probate evidence to reduce fraud and cycle time.

• Consumer Platforms: Provide digital vaults, credential guardianship, and guided workflows; upsell via insurers and bank partners.

Across segments, procurement favors vendors with court/notary connectors, custody integrations, and clear liability and data‑handling terms.

Geography Analysis

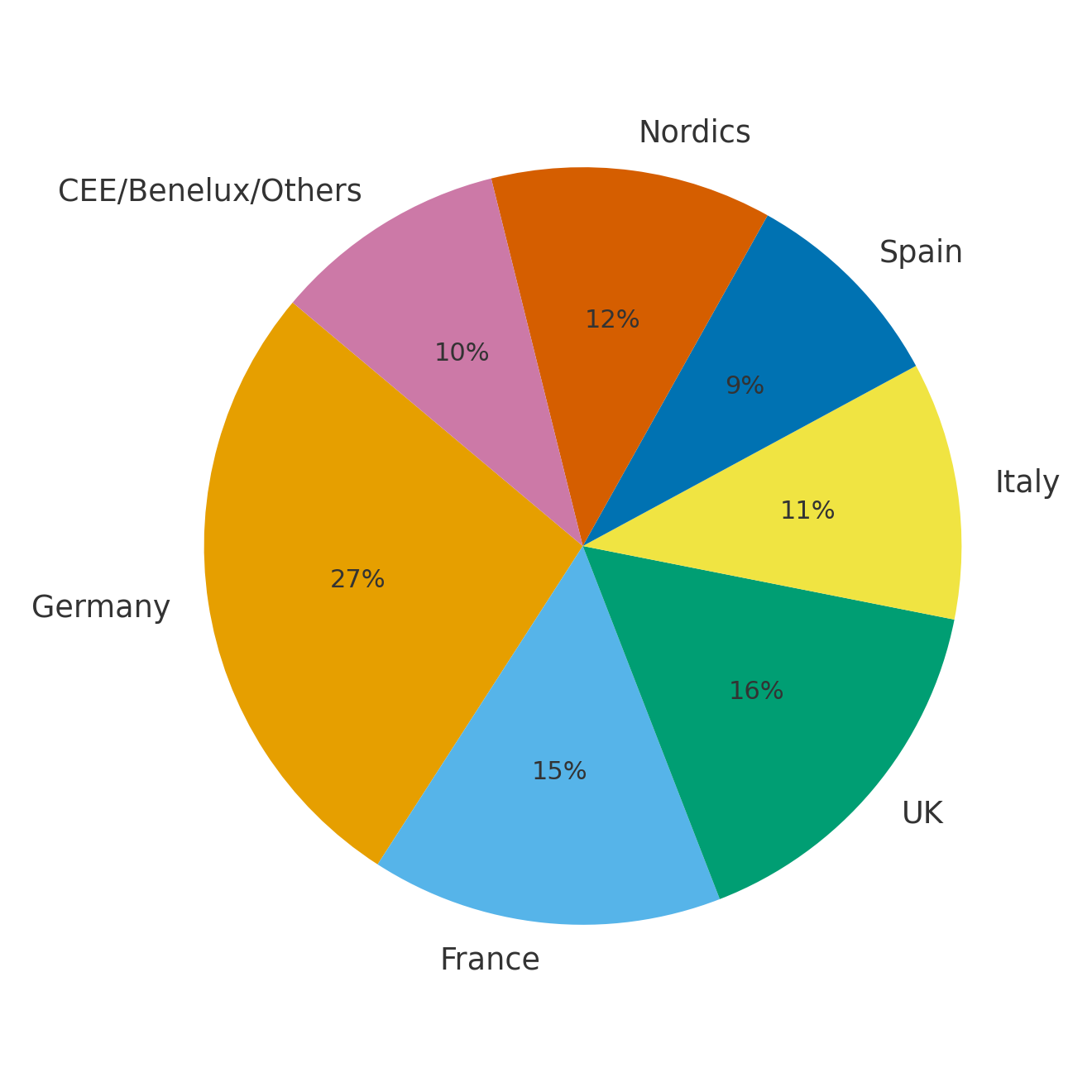

Germany leads with ~27% of Europe’s 2030 market due to early legal‑tech modernization and strong notary systems. France (~15%) and the UK (~16%) scale through bancassurance and custody integrations; the Nordics (~12%) benefit from high digital‑ID penetration; Italy (~11%) and Spain (~9%) expand as court connectors and insurer distribution mature. CEE/Benelux/Others (~10%) rise via cross‑border estate tooling and EU wallet adoption. Cross‑border estates—common for EU residents—drive demand for multilingual workflows, harmonized evidence, and standardized beneficiary policy engines.

Competitive Landscape

The ecosystem spans (1) legal‑tech platforms integrating with registries and court systems; (2) bank/insurer modules for inheritance automation; (3) crypto custody providers with succession tooling; and (4) identity/signature vendors aligned to eIDAS2. Differentiation centers on legal defensibility, custody depth, breadth of connectors, and explainable automation. Expect partnerships between legal‑tech and financial institutions, with consolidation favoring platforms that deliver regulator‑grade evidence, standardized APIs, and packaged distribution through banks and insurers.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071