68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Cross-Border Central Bank Digital Currency (CBDC) Interoperability: Settlement Efficiency & Monetary Policy Implications - Regulatory Impact

From 2025 to 2030, North American cross-border CBDC interoperability will evolve from pilots to production-grade corridors, targeting enhanced wholesale settlement, FX payment-versus-payment, and streamlined regulatory workflows. The focus is on wholesale rails, not retail CBDCs, with platforms designed to compress settlement times, embed compliance controls, and maintain monetary sovereignty. Estimates suggest the market for interoperability tools will grow from about $350 million to $1.2 billion, driven by large financial institutions and API-led fintechs. Early pilots in regulated sandboxes will define best practices for liquidity, compliance, and policy interoperability in large-scale deployments.

What's Covered?

Report Summary

Key Takeaways

- Interoperability not domestic issuance drives near-term North American impact.

- Atomic PvP reduces FX settlement risk and reconciliation steps across corridors.

- Programmable controls allow compliance-by-design and policy alignment.

- Dual-rail designs (RTGS interlinking + DLT bridges) de-risk migration.

- Treasury/FX integration creates the bulk of enterprise ROI.

- Corridor-first rollout beats big-bang; sandbox governance is essential.

- Model-risk & cyber posture must match RTGS-grade resilience.

- Monetary policy effects hinge on liquidity design, not CBDC branding.

Key Metrics

Market Size & Share

North American spending on cross-border CBDC interoperability will scale from an estimated $350M in 2025 to about $1.2B by 2030 as pilots mature into corridor-based production. Growth is concentrated in (i) multi‑CBDC bridges or RTGS interlinking modules; (ii) treasury/FX PvP orchestration; (iii) policy/identity layers; and (iv) integration services. The line chart above depicts the projected path.

Share dynamics: G‑SIBs lead early with governance-heavy programs and dual-rail testing (DLT + RTGS linkages). Regionals expand as vendors offer API-based services with lower TCO. FMIs invest in connector logic and standards to preserve finality semantics. FinTech/RegTech specialists capture implementation revenue and compliance automation. By 2030, ecosystems of providers will coalesce around corridor projects, standardized APIs, and reference control frameworks.

Market Analysis

The cohort mix shows strongest outlays from G‑SIBs and large regionals, followed by FMIs, fintech integrators, and bank treasury/FX desks. In 2025, spend centers on discovery, sandbox pilots, and standards. By 2030, budgets tilt toward production interconnects, corridor operations, and SLA-based platform services.

Buying criteria: (1) compliance-by-design (policy controls aligned to AML/CFT, sanctions, data), (2) liquidity efficiency (PvP with minimal prefunding and clear finality), (3) interoperability depth (RTGS, CLS, DLT bridges), (4) operational assurance (RTGS-grade reliability, cyber posture, model risk governance), and (5) integration economics (reusable connectors to treasury, OMS, payment hubs, data lakes).

Trends & Insights

• Interoperability-first corridor testing via wholesale rails and RTGS–DLT interlinking.

• Compliance in the stack: identity, access controls, and policy rules embedded at platform level.

• Liquidity effects: synchronised PvP can smooth intraday profiles and influence funding spreads.

• Standardization: BIS/IMF workstreams push common semantics while preserving domestic policy controls.

• Security & resilience: RTGS-grade uptime and cyber assurance are procurement gatekeepers.

• Corridor-first ROI: USD–CAD corridors as practical pilots before broader rollouts.

• Vendor ecosystems: connectors, sandboxes, and governance toolkits differentiate.

• Privacy: role-based access and selective disclosure to balance auditability and confidentiality.

Segment Analysis

• G‑SIBs: Dual-rail prototypes (RTGS interlink + DLT bridge), governance, CLS/RTGS interoperability, PvP pilots.

• Large Regionals: API-led stacks with managed connectors; KPIs include settlement-time compression and fail reduction.

• FMIs/RTGS Operators: Connector standards, finality semantics, supervisor coordination on policy modules.

• FinTech/RegTech: Developer tooling, compliance automation, observability layers; win via speed and breadth.

• Bank Treasury/FX: Operationalize PvP/liquidity tooling; calibrate prepositioning vs netting; define stress procedures.

Across segments, buyers converge on auditability, explainability, and repeatable governance. Procurement cycles reward credible corridor pilots, reusable integrations, and clear migration roadmaps.

Geography Analysis

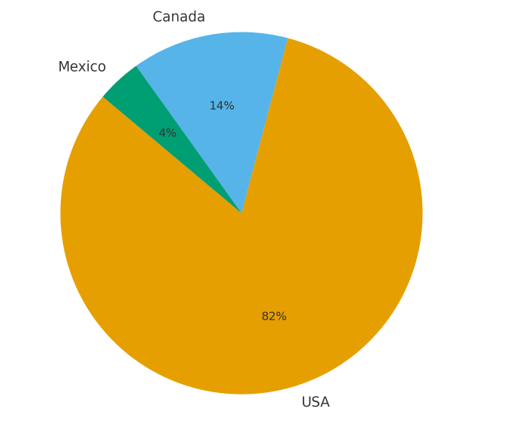

Pie chart showing illustrative regional spend distribution across North America.

Activity concentrates in the United States (≈82% share of adoption/spend) given the scale of dollar flows and concentration of G‑SIB treasuries. Canada accounts for ≈14% as interoperability with U.S. rails intensifies; Mexico represents ≈4% tied to specific trade corridors. The pie chart summarizes illustrative shares. Policy stance is cautious on retail CBDC issuance in the U.S., with wholesale pilots proceeding under tight governance. Canada’s approach is pragmatic and corridor‑focused. Expansion will track corridor economics, comfort with programmability/identity controls, and maturity of RTGS/DLT interlinking standards.

Competitive Landscape

Vendors cluster into platform/bridge providers, compliance/policy-control layers, PvP/DvP orchestration and liquidity tools, and integration specialists. Because outputs and policy philosophies differ, institutions adopt multi‑vendor approaches with clear SLAs and failover strategies. Winning propositions emphasize compliance-by-design, interoperability with FMIs/RTGS and CLS, corridor‑proven PvP with measurable KPI gains, and open connectors to treasury and risk systems. Over the horizon, consolidation and standards-driven convergence will favor platforms that deliver RTGS‑grade assurance while enabling innovation.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071