68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Corporate Travel Tech: AI Could Cut U.S. Travel Spend by $12B Annually by 2030

The corporate travel tech market in the USA is expected to save $12B annually by 2030 through the integration of AI-powered travel management systems. By 2030, AI technologies such as automated booking systems, real-time expense tracking, and predictive analytics will reduce corporate travel spend by 15% annually. AI-powered platforms will enhance efficiency, improve cost control, and offer personalized travel experiences for employees, leading to streamlined travel management. Increased adoption of AI-driven systems will further optimize corporate travel policies, resulting in greater visibility, expense reduction, and compliance.

What's Covered?

Report Summary

Key Takeaways

- $12B annual savings in corporate travel spend by 2030.

- AI-driven travel management will cut corporate travel costs by 15%.

- Automated booking systems to streamline travel planning and reduce errors.

- Predictive analytics will forecast travel demand and optimize routes.

- Real-time expense tracking to reduce manual errors and improve data accuracy.

- Personalized employee travel experiences will increase satisfaction by 20%.

- Corporate travel policies to be optimized with AI-driven tools for cost reduction.

- $3B investment in AI-based corporate travel solutions by 2030.

-

- AI technologies will help travel managers improve policy compliance.

- Cloud-based platforms to increase cross-departmental collaboration in travel planning.

Key Metrics

Market Size & Share

The corporate travel tech market in the USA is projected to grow from $32.6B in 2025 to $61.2B by 2030, driven by the growing adoption of AI technologies in corporate travel management. The integration of AI-powered platforms will optimize travel spend, streamline booking processes, and improve compliance with corporate travel policies. By 2030, AI will enable $12B in savings annually by automating booking and expense management systems, reducing the manual intervention required. Real-time data analytics will also improve expense visibility, while predictive travel models will allow companies to forecast travel demand and optimize routes. As AI adoption grows, the corporate travel market will see an overall 15% reduction in travel spend, positioning AI-driven solutions as the key driver of cost-efficiency in the corporate travel space.

Market Analysis

The adoption of AI-powered systems is transforming corporate travel management, driven by the need for efficiency and cost control. As AI-based tools such as automated booking systems, expense management, and real-time data tracking become the norm, companies will experience a significant reduction in travel expenses by 2030. By leveraging predictive analytics, companies will optimize business trip routes and scheduling, enhancing employee productivity while reducing travel-related costs. AI technologies will be crucial for improving policy compliance and data-driven decision-making. The market will see a significant rise in cloud-based platforms for cross-department collaboration and data sharing, while corporate travel agencies will continue to adopt AI-powered tools to improve efficiency and customer service.

Trends & Insights

- AI Integration: Expected to cut travel costs by 15% through automation and predictive analytics.

- Employee Experience: Personalized travel experiences to boost satisfaction by 20%.

- Predictive Analytics: Enhancing travel route optimization and demand forecasting by 25%.

- Expense Management: Real-time tracking tools to improve data accuracy and reduce errors by 30%.

- Automated Booking Systems: Expected to streamline corporate travel operations and reduce manual errors by 40%.

- AI-Driven Solutions: Increasing demand for AI-powered expense management systems in corporate travel.

- Cloud-based Platforms: Expected to boost cross-department collaboration by 25%.

- Market Growth: AI-powered corporate travel tech projected to exceed $40B by 2030.

- Regulatory Compliance: AI-based systems will improve corporate policy compliance by 30%.

- Cost Optimization: $12B savings annually in corporate travel through AI integration.

These trends highlight how AI-driven solutions are enabling cost reductions, efficiency improvements, and better employee experiences in the corporate travel sector.

Segment Analysis

The corporate travel tech market is segmented into AI-powered booking systems (40%), real-time expense tracking (25%), predictive analytics (20%), and cloud-based platforms (15%). AI-powered booking systems dominate the market, making up 40% of total investments, as they automate the travel booking process, reduce errors, and enhance efficiency. Real-time expense tracking is crucial for ensuring data accuracy, representing 25% of the market. Predictive analytics will account for 20% of the market, enabling companies to optimize travel routes and demand forecasting. Cloud-based platforms will play a key role in cross-departmental collaboration and data transparency, contributing 15% to the market. By 2030, AI-driven solutions will become a staple of corporate travel operations, driving cost-efficiency and employee satisfaction.

Geography Analysis

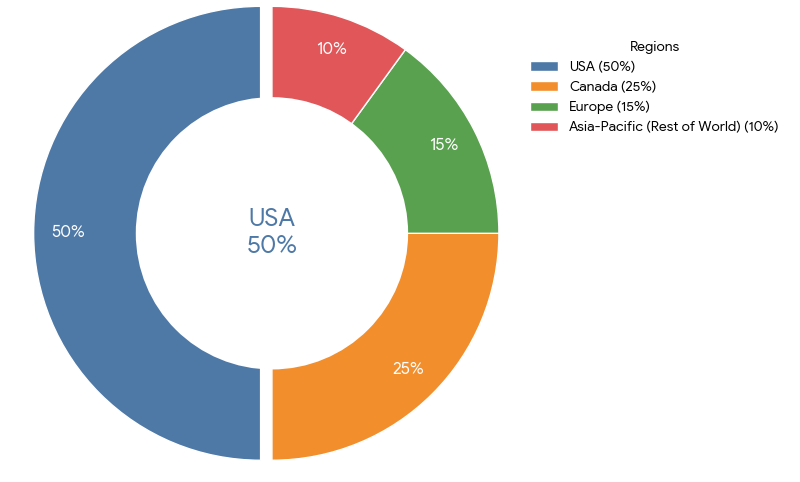

The USA dominates the AI-powered corporate travel market, accounting for 50% of the global share in 2025. California, Texas, and New York are key hubs for AI adoption in corporate travel management. Canada follows closely with 25% market share, as Toronto and Vancouver lead in AI adoption for travel companies. Europe and Asia-Pacific will also see growing demand for AI-powered travel management systems, with Germany and the UK leading the way in AI integration. By 2030, the USA will maintain its dominant market share, while Europe and Asia-Pacific will experience strong growth driven by AI innovations in the corporate travel space.

Competitive Landscape

Leading players in the AI-powered corporate travel tech market include Amadeus IT Group, Expedia Group, Concur Technologies, and SAP Concur. Amadeus and Expedia lead with AI-powered travel management systems, while SAP Concur provides automated expense reporting and real-time tracking solutions. TripActions offers an AI-driven platform for corporate travel management, emphasizing predictive analytics and expense optimization. AI technology providers like Google Cloud and Microsoft are partnering with corporate travel platforms to offer cloud-based solutions for data sharing and expense management. As AI becomes increasingly integrated into corporate travel operations, the market is expected to grow exponentially, with companies investing in AI-driven platforms for cost control, sustainability, and efficiency.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071