68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Commercial EV Fleet Electrification: Market Sizing, TCO Models & Competitive Positioning (2025–2030, US & EU)

The commercial EV fleet market in the US and EU is set for accelerated adoption between 2025 and 2030. Driven by regulatory mandates, falling battery costs, and total cost of ownership (TCO) advantages, fleet electrification will reshape logistics, last-mile delivery, and public transport. By 2030, over 4.5 million commercial EVs are expected to be deployed across these regions. This report evaluates market size, cost models, infrastructure gaps, and competitive dynamics.

What's Covered?

Report Summary

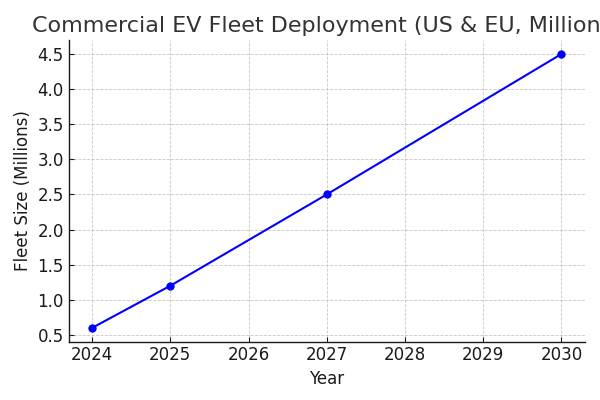

1. Market Size (2025–2030)

By 2030, commercial EV fleet deployment in the US & EU is projected to reach ~4.5 million vehicles, up from 600k in 2024. This translates to a CAGR of ~23%. Penetration of new commercial vehicle sales will hit 25–30% by 2030, with EU adoption outpacing the US due to stronger policy mandates. Fleet operators in last-mile logistics (Amazon, DHL, UPS) lead adoption, while municipal bus fleets in EU cities are also electrifying rapidly.

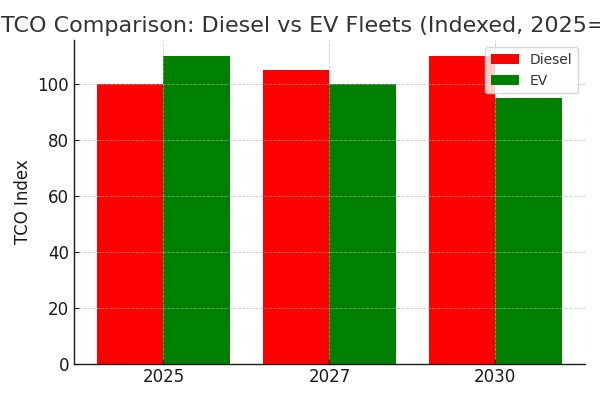

2. TCO Models: EV vs Diesel

TCO parity between EVs and diesel fleets is expected by 2027 in last-mile delivery. By 2030, EVs will offer a 10–15% lower lifetime cost due to cheaper fuel (electricity vs diesel), lower maintenance, and declining battery prices. In 2025, EVs remain 5–10% costlier upfront but parity in operating costs accelerates adoption. Fleet operators will increasingly factor in carbon pricing and ESG-driven procurement mandates.

3. Adoption Drivers

The main drivers include regulatory mandates (EU Green Deal, US state-level ZEV mandates), corporate ESG commitments, and cost savings from electrification. In surveys, 65% of fleet operators cited cost savings as the top driver, while 55% pointed to regulatory compliance. ESG mandates are particularly strong in the EU, where major cities are setting 2030 zero-emission logistics targets. Combined, these factors create a favorable environment for electrification.

4. Battery Cost Trajectories

Battery pack prices are expected to fall from ~$140/kWh in 2024 to $70–80/kWh by 2030, improving TCO economics. Every 10% decline in battery prices lowers vehicle CAPEX by ~6–7%. Energy density improvements also extend vehicle range by 20–25%, reducing downtime. US fleets benefit from Inflation Reduction Act subsidies, while EU fleets gain from CAPEX grants. These cost curves make commercial EVs increasingly attractive.

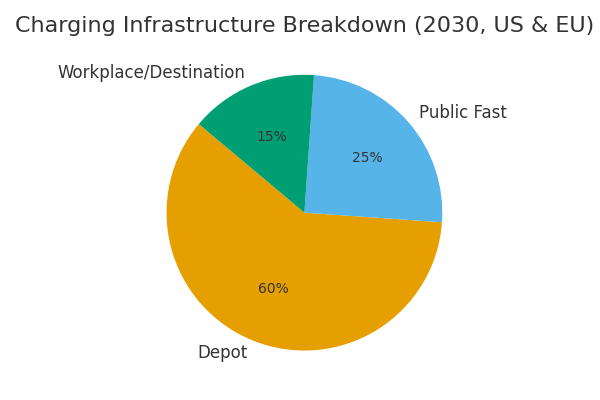

5. Infrastructure Requirements

To support mass deployment, over 1.5M depot and public chargers are needed by 2030 in the US & EU. Depot charging (60%) will dominate for last-mile and logistics fleets, while public fast charging (25%) is critical for intercity transport. The remaining 15% will come from workplace and destination charging. Grid upgrades are also necessary, with electricity demand from fleets rising 5–7% annually.

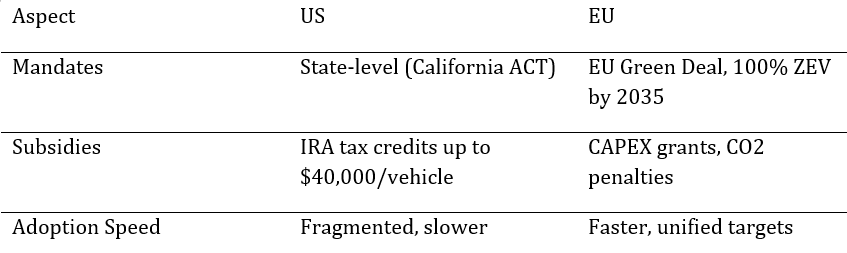

6. Regulatory Frameworks (US vs EU)

The EU Green Deal mandates 100% zero-emission new vehicle sales by 2035, with interim 2030 targets. US regulations are more fragmented, with California leading (Advanced Clean Trucks mandate) and other states following slowly. Subsidies differ: US offers IRA tax credits of up to $40,000 per vehicle, while EU supports CAPEX grants and CO2 penalties on ICE fleets.

7. Competitive Landscape

OEMs like Daimler, Volvo, Tesla, and BYD are leading in commercial EV launches. Charging providers (ABB, ChargePoint, Ionity) are scaling depot and fast-charging solutions. Fleet operators (Amazon, DHL, UPS) are early movers with large EV orders. By 2030, the top 5 OEMs are projected to hold ~65% of the market, while charging infrastructure remains fragmented across multiple players.

8. Segment Adoption (Logistics vs Public Transport)

Logistics fleets are electrifying faster due to shorter routes and depot charging compatibility. Public transport fleets (buses) in the EU are supported by city-level zero-emission mandates, reaching ~40% electrification by 2030. In the US, adoption is slower, at ~25% for buses, due to fragmented funding. By contrast, logistics fleets in both regions are expected to exceed 35% electrification by 2030.

9. Financing & Leasing Models

High upfront CAPEX remains a barrier. Leasing, battery-as-a-service (BaaS), and green bonds are emerging financing models. By 2030, ~30% of commercial EVs in the EU are expected to be financed via leasing/BaaS. US adoption of these models is slower but gaining traction. Subsidies reduce CAPEX burden, making these financing solutions more viable and accelerating fleet conversion.

10. Risks & Challenges

Major risks include battery supply chain constraints (lithium, nickel), grid strain from rapid charging demand, and policy uncertainty in the US. If raw material bottlenecks persist, battery costs could stabilize instead of falling, delaying TCO parity. Grid strain could increase electricity prices by 5–7% annually in high-adoption regions. Policy rollbacks in the US pose another risk, though ESG and corporate commitments may mitigate impacts.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1345

$ 1432

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071