68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Climate Stress Testing Platforms for Mortgage Portfolios: Geospatial Risk Modeling & Capital Buffer Strategies - Sustainability & ESG

From 2025 to 2030, North America's mortgage finance industry is set to embed climate risk management across credit modeling, capital planning, and pricing. The market for climate stress testing platforms will grow from about $920 million in 2025 to $2.45 billion by 2030, driven by large banks, servicers, and insurers integrating geospatial hazard intelligence into lending and portfolio workflows. Market momentum is fueled by quantitative resilience demands from investors and agencies, making automated climate stress testing a core driver of financial stability and pricing strategy in mortgage finance.

What's Covered?

Report Summary

Key Takeaways

• Parcel-level modeling replaces ZIP-level proxies for risk accuracy.

• Fed CSA highlighted governance and interpretability gaps.

• NGFS Phase V defines a global framework for scenario calibration.

• Insurance retreat is a direct driver of mortgage default risk.

• Model dispersion requires dual-vendor validation frameworks.

• Capital buffers shifting to range-based planning methodologies.

• Embedded integrations maximize system-wide ROI.

• Climate-credit modeling will become a core risk management function.

Key Metrics

Market Size & Share

The North American climate stress testing platform market is expanding rapidly—from USD 920 million in 2025 to USD 2.45 billion in 2030. This 21% CAGR reflects accelerating adoption across banks, servicers, and insurers. Large institutions account for nearly two-thirds of total spend, investing heavily in governance, scenario orchestration, and data integrations. Servicers and GSE-linked lenders lead in operational adoption due to direct exposure to mortgage performance and MSR volatility. Over ti...

The U.S. leads regional adoption due to Fed and OCC supervisory pilots, while Canada follows with sustainability-linked reporting frameworks. Institutional demand is concentrated around vendor consolidation and vertical integrations with LOS, servicing, and pricing engines. By 2030, climate modeling will be an embedded feature in every major mortgage risk infrastructure stack.

Market Analysis

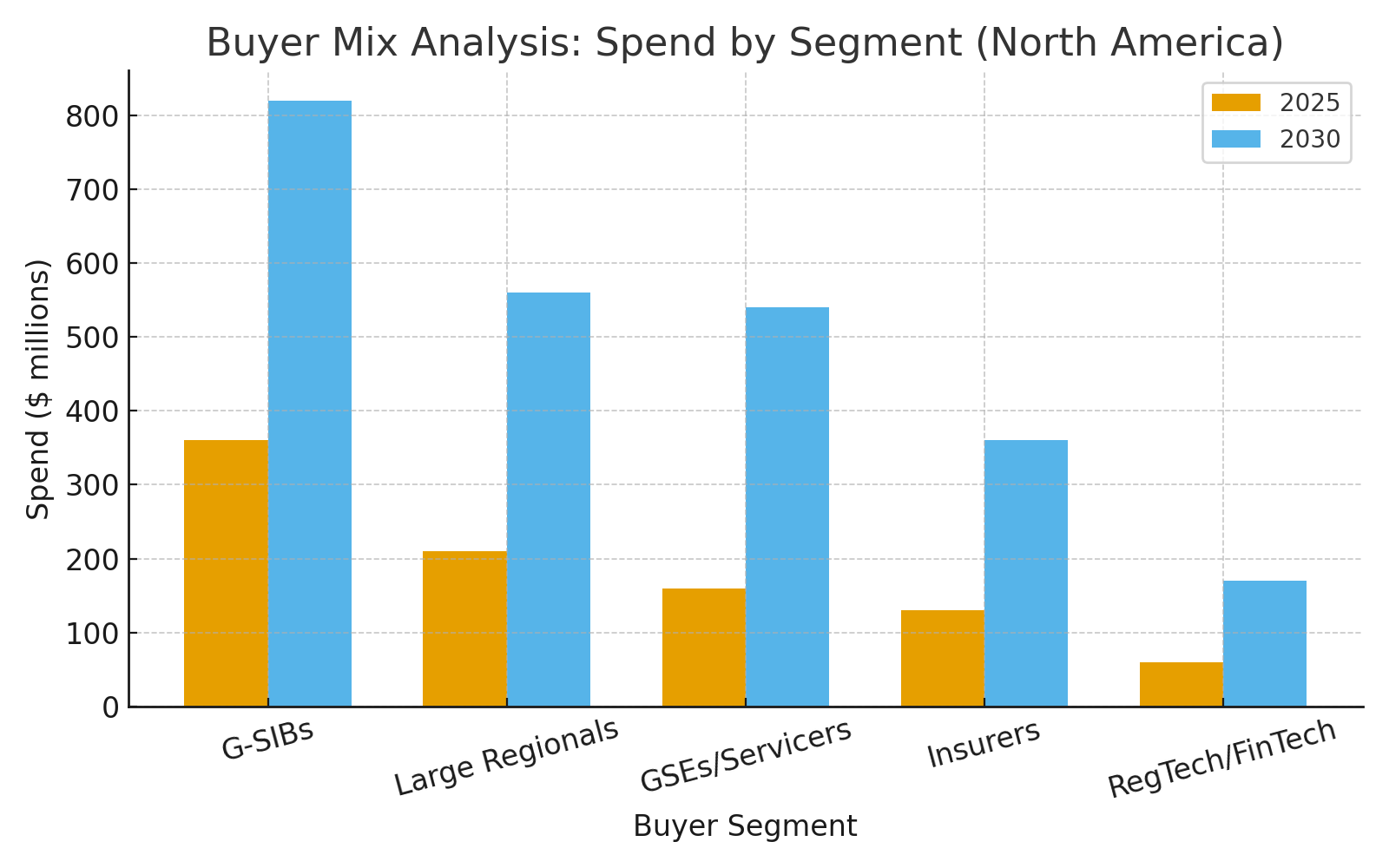

The buyer landscape reflects strong participation by large banks, regionals, and servicers. G-SIBs dominate initial deployment due to complex portfolio exposures, regulatory oversight, and internal stress-testing mandates. Large regionals are closing the gap, adopting modular vendor frameworks that link climate stress data to capital planning and credit pricing. Servicers utilize these models to assess collateral fragility, triage loans, and manage default clusters. Insurers and reinsurers increasingly rely on stress modeling to adjust premiums, reinsurance treaties, and capital reserve requirements. Meanwhile, FinTech and RegTech firms are growing as enablers of API-based scoring tools. By 2030, market maturity will shift spending from analytics dashboards toward embedded workflow automation within LOS and servicing pipelines.

Trends & Insights

Eight macro trends define the 2025–2030 landscape: (1) granular parcel-level modeling becomes a regulatory baseline; (2) insurance withdrawal acts as the key shock channel to affordability; (3) regulators emphasize governance, model risk, and explainability; (4) NGFS Phase V scenarios become the default standard for scenario harmonization; (5) data providers merge with core banking technology vendors to create embedded platforms; (6) uncertainty quantification evolves into a differentiator; (7) ICAAP-s...These insights point toward a market that rewards scientific transparency, interpretability, and platform interoperability. Institutions must evolve from map users to model stewards—embedding climate analytics into capital and business decisions.

Segment Analysis

The climate stress testing ecosystem is highly segmented: banks, servicers, insurers, and fintechs each follow distinct adoption curves. Large banks prioritize governance and capital modeling, often maintaining in-house climate labs and dual-vendor setups. Regional banks depend on modular vendor solutions integrated into credit systems. Servicers and GSE ecosystems leverage stress analytics for MSR stratification, loan pricing overlays, and loss mitigation. Insurers use geospatial analytics to link prop...

Cross-segment convergence is underway: governance, data, and model validation frameworks are becoming standardized. FinTech entrants lower barriers to entry through lightweight APIs and modular credit overlays. The market is moving from tool adoption to infrastructure standardization.

Geography Analysis

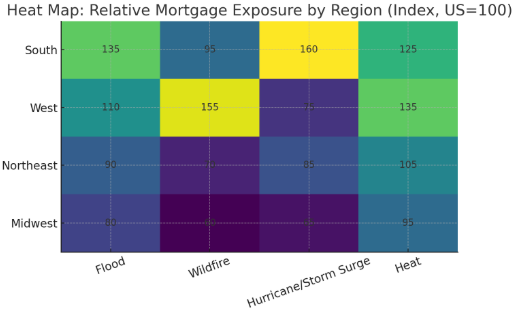

Geographic differentiation is a defining aspect of climate stress modeling. The South exhibits the highest risk intensity due to flood and hurricane exposure (index 135–160). The Western U.S. faces wildfire and heat-related stress (indices 135–155). The Northeast presents moderate flood/surge risk (85–105), while the Midwest, though currently lower risk (60–95), is trending upward due to inland flood and heat events.

Insurance dynamics and housing liquidity amplify regional risk asymmetry. Rising premiums in high-risk counties reduce affordability and collateral values, elevating default probabilities. Banks and servicers respond by embedding region-specific loan limits, risk overlays, and exposure caps. Geography thus transforms from a descriptive variable into a key capital planning dimension.

Competitive Landscape

The competitive environment is vibrant but fragmented. Key players—Jupiter Intelligence, First Street Foundation, Verisk, MSCI, ClimateCheck, and Zesty.ai—each specialize in different aspects: hazard modeling, credit translation, governance, and integration. The market’s hallmark is heterogeneity: no single vendor exceeds 20% share, forcing institutions to adopt multi-vendor validation strategies. Vendors are competing on explainability, workflow integration, and data lineage. Those offering end-to-end ecosystems—data acquisition, modeling, governance, and servicing API delivery—will likely dominate by 2030. Strategic consolidation and embedded partnerships with mortgage-core providers (ICE, Black Knight, Fannie Mae) are already redefining the boundaries of this market. Climate stress testing is evolving from an external service into a native layer of credit infrastructure.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071