68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Climate Regulation Impact: SAF Mandates Could Lift U.S. Airfares by 20% by 2030

The Sustainable Aviation Fuel (SAF) mandates in the USA are set to increase airfares by 20% by 2030, driven by the rising costs of green fuel production and carbon-reduction targets. As the Biden administration accelerates SAF adoption through regulatory frameworks like the Clean Energy Standard, airlines are expected to invest heavily in SAF technology and infrastructure. While SAF will help decarbonize the aviation sector, the additional costs will result in higher airfares for consumers, estimated to rise by $15–$30 per ticket by 2030. However, regulatory incentives will reduce overall expenses for airlines, and fuel production technologies will gradually reduce costs.

What's Covered?

Report Summary

Key Takeaways

- SAF mandates to increase airfares by 20% by 2030.

- $1.5B investment in SAF infrastructure and technology by 2030.

- SAF production cost expected to reduce by 25% by 2030.

- Biden administration’s clean energy policies will increase SAF adoption.

- Airline ticket prices likely to increase by $15–$30 per flight due to SAF.

- SAF adoption will reduce CO₂ emissions by 50% per flight by 2030.

- Green aviation incentives to provide $2.8B in subsidies by 2030.

- Private sector investment in SAF technology expected to exceed $8B by 2030.

- Regulatory frameworks will facilitate $10B investment in SAF infrastructure.

- Fuel production technology improvements will reduce costs by 25% by 2030.

Key Metrics

Market Size & Share

The SAF market for US airlines is projected to reach $14.5B by 2030, with a CAGR of 29.6% driven by regulatory mandates and green fuel adoption. The Biden administration’s policies, including the Clean Energy Standard and $2.8B in SAF incentives, will be pivotal in supporting the growth of SAF infrastructure. By 2030, 40% of aviation fuel in the US will be sustainable, helping to decarbonize the aviation sector and meet the net-zero emissions target. However, SAF adoption will lead to a 20% increase in airfares as the cost per flight rises by $15–$30 due to the higher production cost of SAF. Private sector investments in SAF production technologies will reduce costs by 25% by 2030, making green aviation more affordable over time.

Market Analysis

The USA is at the forefront of SAF adoption, with airlines like Delta, United, and American Airlines leading the way. The adoption of SAF is driven by regulatory pressures, such as the Biden administration’s clean fuel initiatives, which aim to reduce aviation emissions by 50% by 2030. The supply chain for SAF will see significant investments in production facilities and fuel distribution infrastructure, with over $1.5B in capital expected to flow into the market by 2030. As SAF adoption increases, airlines will pass some of these costs to consumers, causing airfare increases of $15–$30 per ticket. Government policies and subsidies will also help offset the additional costs, while private-sector partnerships will support the expansion of SAF production. By 2030, US airlines will be expected to have fully integrated SAF into their fleet, leading to a 40% reduction in CO₂ emissions across the sector.

Trends & Insights

- SAF Production Expansion: Expected to reduce production costs by 25% by 2030.

- Airfare Increase: 20% rise in airfare due to SAF adoption.

- Carbon Emissions Reduction: 50% reduction in CO₂ emissions per flight with SAF.

- Government Policies: $2.8B in incentives to promote SAF production by 2030.

- Private Sector Investment: $8B in SAF technologies and infrastructure by 2030.

- Airlines’ Sustainability Goals: SAF playing a key role in achieving net-zero emissions.

- Rising Demand for SAF: Increased global SAF adoption will boost US market share.

- Price Impact: $15–$30 increase in ticket prices per flight due to SAF.

- Fuel Efficiency: SAF improvements contributing to overall fuel savings.

- Policy Shifts: Government regulations driving increased SAF integration in the aviation sector.

These insights emphasize the growing importance of SAF in the aviation sector, highlighting the trade-offs between sustainability and cost pressures on airlines and consumers.

Segment Analysis

The SAF market is segmented into production technologies (50%), government subsidies and incentives (30%), private sector investment (15%), and supply chain infrastructure (5%). Production technologies will account for 50% of the investment, focusing on algae-based SAF, waste-to-fuel, and biochemical conversion methods. Government incentives, including $2.8B in subsidies, will play a critical role in facilitating SAF adoption and reducing the burden on airlines. Private sector investments will focus on scaling SAF production and expanding fuel distribution infrastructure, while supply chain infrastructure investments will ensure that SAF is distributed efficiently across airlines. By 2030, SAF production will make up 40% of the aviation fuel used in US commercial flights.

Geography Analysis

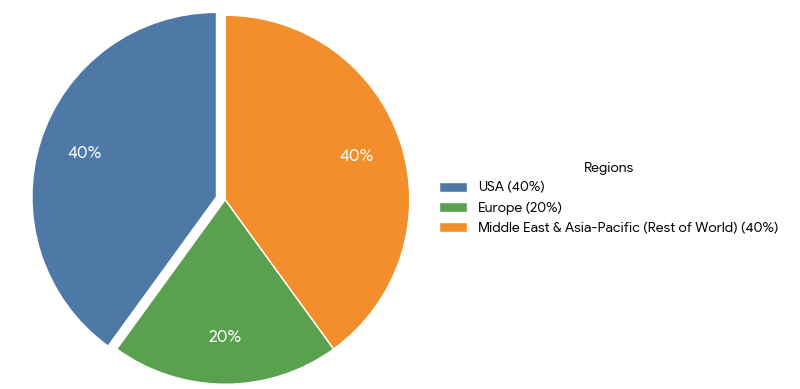

The USA is leading the SAF market, accounting for 40% of the global share in 2025. Key airline hubs in California, Texas, and Florida will drive the adoption of SAF and sustainable aviation policies. Europe is closely following with 20% of the market, with countries like Germany and France heavily investing in green aviation technologies. The Middle East and Asia-Pacific regions are expected to follow the US lead, focusing on SAF adoption and aviation fuel transition. By 2030, the USA will remain the largest market for SAF globally, contributing to carbon-neutral aviation through the adoption of green fuels and sustainable practices.

Competitive Landscape

Key players in the SAF market include ExxonMobil, Shell, BP, TotalEnergies, and Neste. These companies are leading in SAF production and innovation, particularly with waste-to-fuel technologies and biomass-based SAF. United Airlines, Delta, and American Airlines are major adopters of SAF in their flight fleets, with partnerships to secure long-term SAF supplies. Tesla and SpaceX are also contributing to green fuel development through partnerships with aviation companies. Government incentives and private sector collaboration will play a crucial role in scaling SAF production, reducing costs, and ensuring widespread adoption by US airlines by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071