68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

China’s EV Export Domination vs. Western Trade Barriers: Policy Risks, Competitive Response & Supply Chain Realignment (2025–2030)

China has emerged as the world’s largest EV exporter, shipping over 5 million units annually by 2030, but faces mounting trade barriers in the EU and U.S. Western governments are responding with tariffs, anti-subsidy probes, and local supply chain mandates. This report analyzes the policy risks, competitive responses by Western OEMs, and the resulting supply chain realignments shaping global EV trade flows between 2025–2030.

.png)

What's Covered?

Report Summary

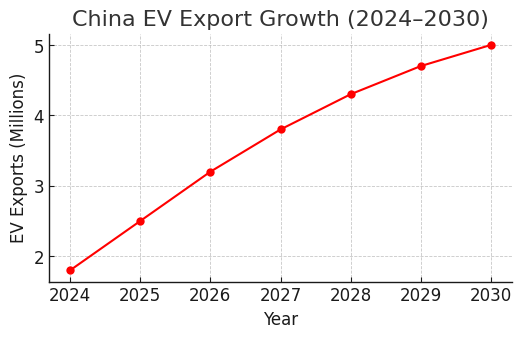

1. China’s EV Export Growth (2024–2030)

China’s EV exports are projected to grow from 1.8M units in 2024 to nearly 5M units annually by 2030. Europe remains the top destination with over 50% share, while Latin America, Africa, and Southeast Asia emerge as secondary growth markets.

2. Tariff Impacts on EV Prices

The EU’s proposed 10–20% anti-subsidy tariffs could raise EV prices in Europe by 8–12% by 2030. In contrast, U.S. IRA rules fully exclude Chinese EVs from subsidies, effectively pricing them out of the U.S. market.

3. Supply Chain Realignment

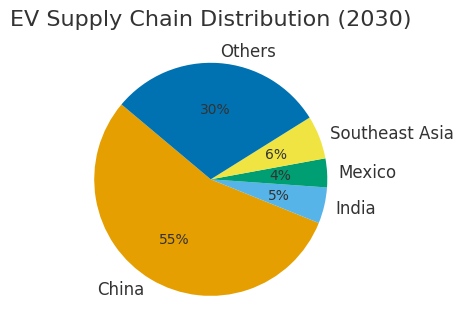

Trade barriers are forcing diversification of EV supply chains. By 2030, China’s share of global EV supply chains is projected to fall from 70% to ~55%, with India, Mexico, and Southeast Asia gaining a combined 15% share.

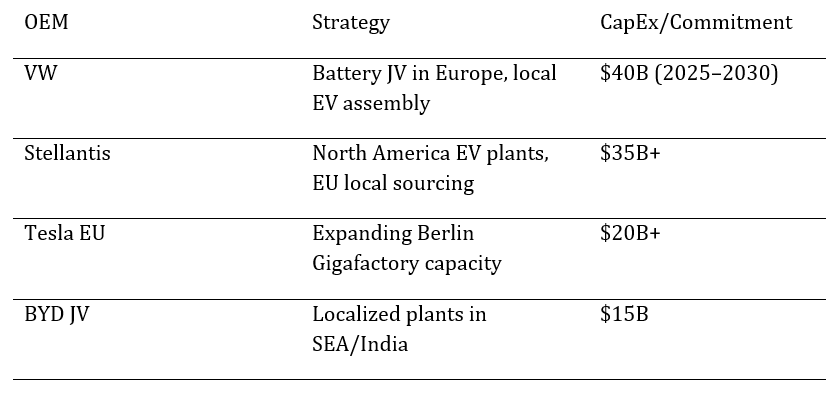

4. Western OEM Strategic Responses

Western OEMs are increasing investments in localized production, joint ventures, and battery partnerships to reduce reliance on Chinese imports and comply with trade rules.

5. Tariffs and EU EV Adoption

The imposition of tariffs raises EV costsfor European consumers. By 2030, EU EV adoption could be 5–7% lower thanbaseline if tariffs remain at 20%. Germany and France are the most affected dueto high reliance on Chinese imports, while Italy and Spain diversify sourcingfaster.

6. Battery & Component Supply Chains

Battery cell and component sourcing remainsChina-dominated, but new plants in Hungary, Poland, and Mexico are capturing~10% share by 2030. Restrictions on Chinese graphite and lithium inputs couldadd $15–20/kWh to EU pack costs.

7. Role of India, Mexico & Southeast Asia

India, Mexico, and Southeast Asia attractsignificant OEM investment to diversify supply chains. By 2030, these regionscould account for ~15% of EV exports to the West, reducing China’s dominance.

8. China’s Cost Advantage

Even under tariffs, Chinese EVs maintain a15–20% cost advantage due to economies of scale, integrated supply chains, andstate subsidies. However, stricter trade rules and logistics costs could erodemargins by 5–7% by 2030.

9. OEM Alliances & JV Risks

Joint ventures between Chinese and Western OEMs face political scrutiny. Examples include potential reviews of BYD–Teslacollaborations in Europe and CATL supply deals. JV risks include blockedapprovals, stranded Capex, and IP exposure.

10. Scenarios for Trade Tensions

Two scenarios dominate outlook: (a)Escalation – tariffs expand to 25–30%, further reducing EU adoption andsparking WTO disputes. (b) Relaxation – post-2030 gradual rollback of tariffsif Chinese OEMs localize production in Europe. Base case assumes moderatedtariffs but permanent partial restrictions.

Key Takeaways

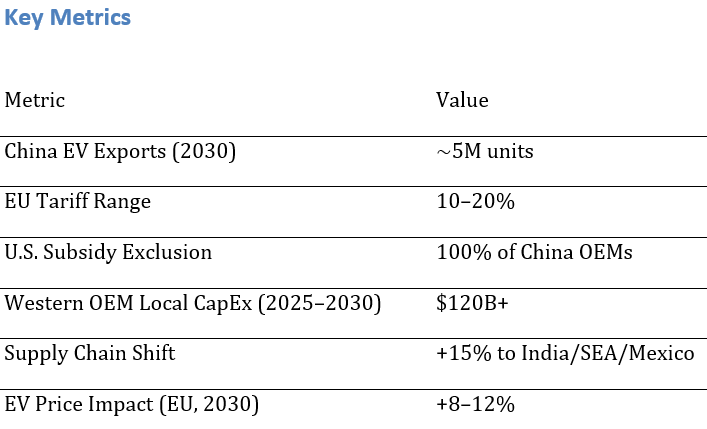

• China’s EV exports projected to hit 5M units annually by 2030.

• EU investigating anti-subsidy tariffs of 10–20% on Chinese EV imports.

• U.S. Inflation Reduction Act (IRA) effectively excludes Chinese OEMs from subsidies.

• Western OEMs (VW, Stellantis, Tesla EU) increasing localization of battery/assembly plants.

• Global battery supply chain diversification: India, Mexico, Southeast Asia gaining share.

• Trade barriers could raise EU EV prices by 8–12% by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1432

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071