68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Carbon Credit Trends: Nature-Based Solutions vs Tech Removal Projects

From 2025 to 2030, corporate demand in Germany and across Europe will bifurcate between high‑integrity nature‑based solutions (NBS) and engineered removals, with distinct price, risk, and procurement profiles. Nature‑based credits REDD+ with conservative baselines, improved forest management (IFM), blue carbon remain the volume workhorses, supported by robust MRV, leakage controls, and permanence buffers. Engineered removals such as DACCS and BECCS command the highest prices due to verifiable additionality and durability, but supply remains limited and delivery risk requires structured offtake. Pricing spreads widen as integrity frameworks consolidate. Credits aligned with ICVCM Core Carbon Principles and used under VCMI Claims earn durable premiums; buyers increasingly separate emissions reductions (internal/value‑chain) from beyond‑value‑chain contributions per SBTi guidance.

What's Covered?

Report Summary

Key Takeaways

1) Integrity is the price driver: CCP‑aligned, VCMI‑eligible units sustain premiums.

2) Engineered removals remain scarce and expensive; lock supply via structured multi‑year offtake.

3) High‑integrity NBS provide cost‑effective volumes plus co‑benefits; prioritize jurisdictional and MRV rigor.

4) Separate reductions vs beyond‑value‑chain contributions per SBTi to de‑risk claims.

5) Anchor budgets in EU ETS/UK ETS shadow prices; VCM complements, not substitutes, compliance.

6) Use Article 6‑ready documentation to avoid double counting and future‑proof claims.

7) Adopt portfolio analytics (ratings, meta‑registries) and assurance‑grade record‑keeping.

8) Phase migration toward removals (20–40% by 2030) while maintaining NBS volume backbone.

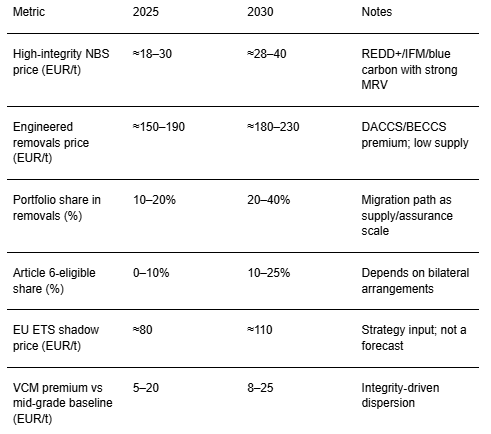

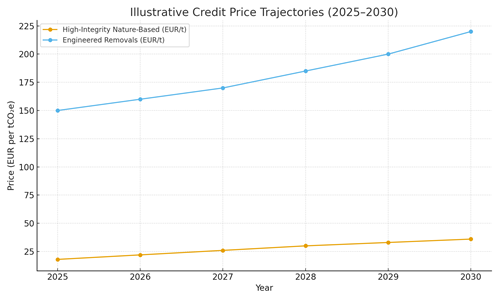

Key Metrics

Market Size & Price Outlook

Price signals in Germany & Europe reflect a tightening integrity regime and evolving compliance baselines. High‑integrity NBS prices are expected to trend upward as conservative baselines, durable monitoring, and leakage safeguards become standard; engineered removals maintain a significant premium given capital intensity, technology learning curves, and constrained supply. Corporate portfolios therefore model two curves: a mid‑tier NBS trajectory and a higher removals trajectory. The wedge between them represents the ‘quality premium’ a budgeting line item that grows with claims stringency.

Volume outlook: NBS supply remains broad, but integrity screens reduce effective supply; removals supply expands from a small base via early DACCS/BECCS facilities, with multi‑year offtake required to secure allocations. Compliance (EU ETS/UK ETS) sets a carbon‑cost floor that shapes shadow pricing across capex decisions. Aviation adds standardized CORSIA demand for eligible units. For corporates, a practical approach is to hedge with compliance baselines and ladder VCM procurement across vintages and categories, scaling removals exposure as projects reach FID and COD.

Market Analysis (Tiered Premiums)

Quality tiering crystallizes into three bands: (1) engineered removals at the top; (2) high‑integrity NBS (REDD+, IFM, blue carbon) in the middle; (3) other reduction categories with robust MRV at the base. Premiums over a mid‑grade baseline reflect additionality, permanence, and MRV confidence. Our illustrative premiums show DACCS outpricing all categories, followed by BECCS removals; blue carbon leads NBS due to strong co‑benefits and clear monitoring in coastal ecosystems. REDD+ with conservative baselines and jurisdictional alignment prices ahead of IFM where permanence risk is well managed.

Procurement mechanics: Set tier‑specific willingness‑to‑pay bands and contract terms (collars, replacement rights, volume‑flex, milestone‑based payments). Use integrity ratchets automatic price/quality step‑ups if ratings or CCP/VCMI status improves. Maintain buffers and replacement pools to manage invalidation. Portfolio analytics should track basis risk (index vs achieved price), integrity ratings, and delivery milestones; contract language should pre‑define remedies for methodology updates or rating downgrades.

Trends & Insights

Integrity frameworks (ICVCM CCPs, VCMI Claims) become the default procurement screen; Article 6 authorization and corresponding adjustments gain traction for select bilateral flows. EU ETS/UK ETS reforms maintain firm carbon‑cost baselines, while meta‑registries and ratings tools expand data transparency. German corporates lead in assurance‑ready documentation and internal carbon pricing, influencing supply‑chain expectations. Biodiversity and community co‑benefits rise in importance, favoring high‑quality NBS. Engineered removals advance through offtake‑backed financing and government support; learning curves narrow unit costs but keep premiums elevated through 2030. Expect consolidation among brokers and project developers, with platform players offering bundled analytics, contracting, and delivery guarantees.

Segment Analysis (Buyer Profiles)

Industrial emitters (steel, chemicals, cement) primarily anchor budgets in EU ETS exposure; VCM is used for contribution claims and reputational risk management. FMCG and retail emphasize NBS with strong co‑benefits and expand removals share as budgets grow. Aviation manages dual exposure (EU ETS/CORSIA) and favors standardized credit pools. Financial institutions focus on financed‑emissions strategies and often prefer engineered removals for long‑dated contribution claims. Tech and manufacturing adopt analytics‑heavy procurement with dynamic rebalancing as ratings and methodologies evolve. Public entities and cities especially in Germany pilot contribution programs aligned with local biodiversity goals.

Geography Analysis (Germany & Europe Readiness)

Germany ranks among the most ready markets for high‑integrity procurement due to disclosure norms, data infrastructure, and governance maturity. Nordics and Benelux follow closely, combining strong policy alignment with sophisticated buyers and growing assurance ecosystems. France and the UK & Ireland offer solid market access and policy frameworks, while Italy and Iberia show improving infrastructure and buyer education. Central and Eastern Europe trail on integrity infrastructure depth but are catching up via EU‑wide reporting requirements. Buyers operating across multiple regions should calibrate cadence, claims governance, and supplier onboarding to local maturity levels while maintaining an enterprise‑wide integrity standard.

.png)

Competitive Landscape (Ecosystem & Intermediaries)

Key actors include standards/guidance bodies (ICVCM, VCMI, UNFCCC Article 6), registries (e.g., Verra, Gold Standard, ART), ratings and data platforms, brokers/exchanges, project developers (NBS and removals), and auditors/assurance providers. Competitive differentiation centers on integrity alignment, delivery reliability, and transparency. Engineered‑removal developers compete on technology readiness, energy intensity, and offtake structure; NBS developers differentiate via jurisdictional programs, leakage management, and co‑benefit measurement. Expect increased use of indexed pricing, structured offtake, and replacement rights. Buyers benefit from platform partners that integrate analytics, contracting, and delivery services into a single SLA with audit‑ready records.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071