68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Carbon Capture in Cement Production: Oxy-Fuel Kiln Retrofits & Mineralization Pathways

Cement is responsible for ~7–8% of global CO₂ emissions, with Europe accelerating abatement via carbon capture, utilization and storage (CCUS). Between 2025 and 2030, two practical decarbonization routes stand out for European cement producers: (1) oxy‑fuel kiln retrofits that enable a high‑CO₂ flue stream for efficient capture and pipeline transport to saline storage; and (2) mineralization pathways that bind CO₂ into stable carbonates (in‑plant or near‑plant) for construction materials, aggregates, or cement substitutes. The optimal route is site‑specific and shaped by storage access, cluster logistics, capex constraints, policy support (ETS/Innovation Fund/CFD‑style instruments), and product‑market strategies for low‑carbon cement. Oxy‑fuel retrofits deliver deep capture rates (≥90%) and scale well when storage and transport infrastructure are available. They require kiln modifications, oxygen supply integration, and heat‑balance optimization. Mineralization offers modularity and local offtake opportunities, reducing dependence on long‑distance CO₂ transport.

What's Covered?

Report Summary

Key Takeaways

1) Oxy‑fuel retrofits enable high‑purity CO₂ streams and deep capture where storage infrastructure exists.

2) Mineralization offers modular, local solutions; bankability depends on product standards and steady offtake.

3) EU ETS + grants/CFDs underpin returns; cluster strategies lower transport and permitting risk.

4) Energy integration (oxygen supply, WHR, electrification) is decisive for OPEX and uptime.

5) CO₂ logistics (pipeline/ship/truck) and storage queue times are the gating items for COD.

6) Low‑carbon cement premiums and public procurement standards are emerging demand drivers.

7) Standardization and warranties for mineralized products accelerate acceptance and financeability.

8) Portfolio approach: pilot mineralization where storage is scarce; deploy oxy‑fuel where clusters mature.

Key Metrics

Market Size & Share

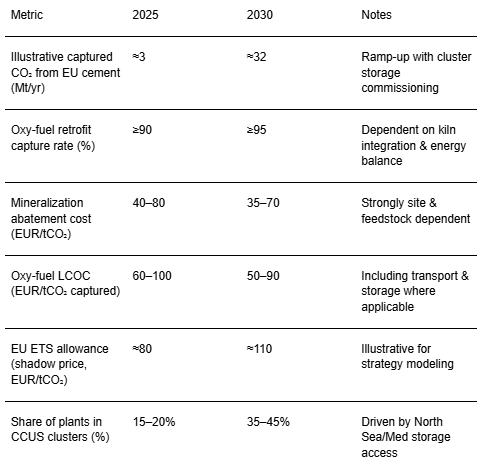

Europe’s cement CCUS pipeline is transitioning from feasibility to execution, with flagship oxy‑fuel and post‑combustion projects anchoring clusters that feed North Sea and onshore saline storage. Illustrative captured volumes indicate a ramp from ~3 MtCO₂/yr in 2025 to ~32 MtCO₂/yr by 2030 if a subset of projects reach COD and regional storage systems come online. Early market share concentrates in countries with mature cluster infrastructure (Nordics, Benelux, parts of France and UK), followed by DACH and Italy as permitting and interconnections progress. Mineralization projects, though smaller individually, broaden participation and provide near‑plant abatement where pipeline access is limited.

Market share dynamics hinge on: (1) storage access and pipeline/terminal capacity; (2) plant‑level readiness for oxy‑fuel retrofit (kiln age, refractory, oxygen integration); (3) mineralization feedstock and product‑market fit; and (4) policy leverage (ETS, grants, potential CFDs). Producers that secure early cluster slots, standardized interfaces, and bankable offtake for low‑carbon cement or mineralized products will capture disproportionate share through 2030.

Market Analysis

Oxy‑fuel retrofits and mineralization differ in cost structure and scalability. Oxy‑fuel’s higher energy and oxygen requirements elevate OPEX but yield a high‑purity CO₂ stream and >90% capture at scale, making it attractive where cluster logistics exist. Mineralization’s cost profile benefits from lower energy intensity and reduced transport needs when utilization is local; however, abatement hinges on reaction kinetics, feedstock availability, and the durability of carbonates. Our illustrative breakdown suggests LCOC in the range of EUR 60–100/tCO₂ for oxy‑fuel (including T&S) versus EUR 40–80/tCO₂ for mineralization, with wide site‑specific variance. EU ETS savings (shadow price ~EUR 80→110/tCO₂ across 2025–2030), grants, and potential CFDs are the primary value levers.

Key risks: energy price volatility, oxygen plant reliability, compression bottlenecks, storage permitting timelines, and product acceptance for mineralized outputs. Mitigations include long‑term energy contracts/PPAs, redundancy in compression and oxygen supply, early Class VI‑equivalent engagement, and product standards with performance warranties. Portfolio strategies often pair one large oxy‑fuel retrofit in a cluster with satellite mineralization projects to diversify delivery risk.

Trends & Insights

Cluster momentum: Northern European clusters (e.g., North Sea–linked systems) unlock scale economies in CO₂ transport and storage and are setting templates for tariffing and access. Technology maturation: oxygen production efficiency and kiln heat‑integration are improving, while mineralization advances focus on faster kinetics, broader feedstocks (slag, demolition fines), and quality assurance. Policy evolution: higher ETS prices, grant mechanisms, and emerging CFD structures are accelerating FIDs for first‑wave projects. Market pull: public procurement and private buyers are piloting low‑carbon cement specifications, enabling premium markets. Risk management: standardization of interfaces (from flange to registry) and contracting (availability KPIs, take‑or‑pay) reduces bankability gaps.

Segment Analysis

Integrated producers with multi‑plant portfolios will likely adopt a mixed pathway: cluster‑connected oxy‑fuel at flagship sites and modular mineralization at satellite plants. Mid‑cap producers without cluster proximity can focus on mineralization plus efficiency measures while monitoring cluster expansion. Downstream segments (ready‑mix, precast) benefit from mineralized aggregates and SCMs that reduce clinker factor. Engineering, procurement, and construction (EPC) firms with oxy‑fuel and oxygen‑supply experience gain advantage in turnkey retrofits, while logistics operators specializing in CO₂ compression, shipping, and terminal services become crucial value‑chain partners. Financial sponsors are targeting platform plays that bundle capture, transport, storage, and product offtake into de‑risked contracts.

Geography Analysis

Readiness varies across Europe. The Nordics and Benelux lead due to early storage access, strong policy support, and industrial‑cluster coordination. UK & Ireland and parts of France follow, aided by proximity to North Sea storage and maturing cluster governance. DACH and Italy exhibit growing project pipelines but face permitting cadence and interconnection timing constraints. Iberia, CEE, and the Baltics are building capacity, with mineralization offering near‑term options where pipeline/storage timelines are longer. Cross‑border shipping to North Sea storage hubs is emerging as a practical bridge solution.

.png)

Competitive Landscape

The competitive field spans kiln OEMs, oxygen suppliers, capture technology licensors, mineralization tech developers, EPC firms, cluster operators, and storage developers. Differentiation centers on (1) retrofit integration expertise and outage minimization; (2) energy intensity and oxygen efficiency; (3) proven carbonate product quality and warranties; (4) access to cluster capacity and Class VI‑equivalent storage; and (5) contracting sophistication (availability guarantees, tariff structures, and product premium mechanisms). As first-wave projects move to COD, experience curves and standardized contracting are expected to compress cost ranges, with platform players capturing share via repeatable delivery and bundled service offerings.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071