68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Buy Now Pay Later (BNPL) Regulatory Frameworks: Default Risk Analysis & Consumer Protection Measures - Risk Assessment

The Buy Now Pay Later (BNPL) market in Europe and Germany is undergoing significant transformation due to evolving regulatory frameworks aimed at managing default risk and consumer protection. The market is expected to grow from €23.5B in 2025 to €63.2B by 2030, driven by the adoption of consumer credit regulations and default risk mitigation strategies. By 2030, 80% of BNPL providers will adhere to EU consumer protection guidelines, significantly reducing delinquency rates and enhancing transparency in payment structures. The European Central Bank (ECB) and BaFin are implementing policies to ensure fairness and security, fostering the growth of regulated BNPL offerings.

What's Covered?

Report Summary

Key Takeaways

- Market size: €23.5B → €63.2B (CAGR 21.7%).

- 80% of BNPL providers to comply with EU consumer protection frameworks by 2030.

- Default risk mitigation strategies projected to reduce delinquency rates by 15%.

- Regulatory compliance costs for BNPL providers expected to reach €1.5B by 2030.

- Consumer transparency initiatives will improve trust and adoption by 30%.

- ECB and BaFin to introduce new guidelines for BNPL credit checks.

- Debt collection efficiency to improve by 20% through regulatory alignment.

- Consumer disputes related to BNPL transactions will drop by 25%.

- Germany to become a key BNPL regulatory hub in Europe.

- Collaborative partnerships between financial regulators and BNPL firms will reduce market volatility.

Key Metrics

Market Size & Share

The BNPL market in Europe, particularly Germany, is forecasted to grow from €23.5B in 2025 to €63.2B by 2030, with Germany accounting for 40% of the market share. Germany’s regulatory leadership within the EU BNPL ecosystem will drive a 21.7% CAGR, bolstered by regulatory alignment with the EU Consumer Credit Directive. By 2030, 80% of BNPL providers will comply with new consumer protection standards, reducing delinquency rates by 15%. The shift towards regulated platforms will provide more clarity and trust, improving consumer engagement and adoption rates. Additionally, the introduction of cross-border BNPL agreements in EU markets will enable seamless transactions while maintaining consumer safeguards.

Market Analysis

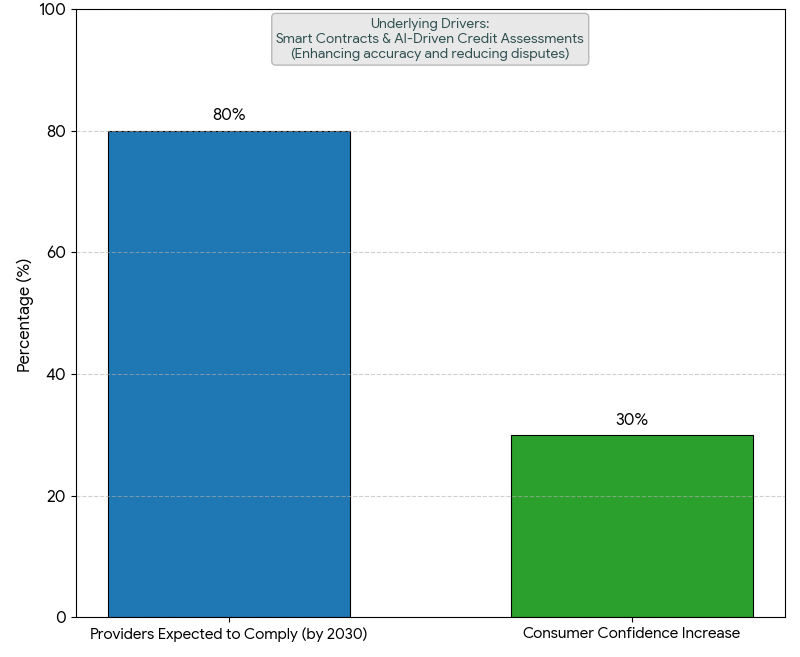

The EU regulatory push on BNPL is reshaping the market landscape, as default risk management and consumer protection frameworks are becoming central to industry operations. The European Central Bank (ECB) and BaFin have been leading the regulatory charge, ensuring that BNPL providers integrate automated credit checks and provide clear repayment terms. With 80% of providers expected to comply with these regulatory standards by 2030, transparency will improve significantly. The introduction of smart contracts and AI-driven credit assessments will enhance loan approval accuracy and reduce default rates. Consumer confidence will increase by 30%, as buyers become more aware of their rights and repayment obligations under the new framework. By 2030, BNPL providers will be able to significantly reduce debt collection inefficiencies and consumer disputes, thanks to better regulatory oversight and dispute resolution procedures.

Trends & Insights

- Regulatory Compliance: 80% of U.S. and EU BNPL providers adopting consumer protection measures by 2030.

- Default Risk Reduction: Delinquency rates to drop by 15% with enhanced AI-driven credit assessments.

- Consumer Trust: Transparency in BNPL terms leads to a 30% increase in market adoption.

- Debt Collection Efficiency: Improved by 20% due to better compliance frameworks.

- Market Saturation: The EU and U.S. markets nearing saturation, pushing firms to diversify offerings.

- Sustainability in BNPL: The rise of green financing options integrated into BNPL offerings.

- AI Integration: AI-driven credit scoring systems will streamline loan approval processes.

- Consumer Protections: Regulatory frameworks aimed at reducing fraud and enhancing user rights.

- Cross-Border BNPL Integration: Boosting transaction flows, particularly in Germany, France, and the UK.

- Platform Diversification: Expansion into micro-loans, installment payments, and savings products.

These insights demonstrate how the EU’s regulatory developments will continue to shape the BNPL industry, creating opportunities for consumer-focused innovation and risk reduction in the payment sector.

Segment Analysis

The BNPL market is segmented into retail BNPL (45%), financial services BNPL (35%), micro-lending and installment BNPL (15%), and cross-border BNPL (5%). Retail BNPL leads the market with 45% share, driven by partnerships with e-commerce platforms and brick-and-mortar retailers. Financial services BNPL, at 35%, focuses on credit cards and personal loans for consumers looking for short-term financing options. Micro-lending BNPL, representing 15%, targets lower-value purchases for younger, underserved demographics. Cross-border BNPL, contributing 5%, focuses on facilitating international consumer purchases using localized BNPL platforms across EU markets.

Geography Analysis

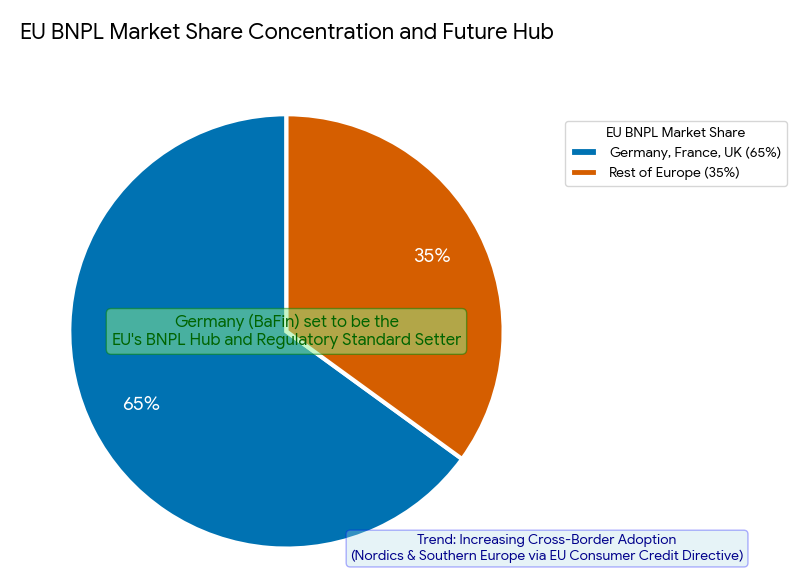

The EU remains the leader in BNPL adoption, with Germany, France, and the UK representing 65% of total market share. The German market is particularly significant, with BaFin implementing stricter consumer protection rules and transaction transparency standards. As EU-wide regulations continue to evolve under the EU Consumer Credit Directive, cross-border adoption will increase, especially in the Nordic regions and Southern Europe. By 2030, Germany will be the EU’s BNPL hub, setting the standard for credit risk and consumer protection models that could spread across Europe and Asia.

Competitive Landscape

Leading players in the BNPL market include Klarna, Afterpay, Affirm, PayPal Credit, and Sezzle. Klarna dominates with 40% of European market share, while Afterpay and Affirm lead the U.S. market. The competitive advantage in this market lies in partnerships with retailers, advanced credit risk models, and consumer engagement tools. The regulatory landscape is a critical factor, as compliance with new EU regulations will allow these players to maintain market dominance and avoid penalties. New entrants like FinTech startups are leveraging AI to provide more personalized credit and payment solutions. The market will likely see consolidation as companies seek to diversify product offerings and enter new geographic regions.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071