68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Bank-as-a-Platform (BaaP) in Europe: API Monetization, Partner Ecosystem Value & Compliance Cost

Bank-as-a-Platform (BaaP) is transforming European banking by enabling institutions to monetize APIs, build partner networks, and improve regulatory compliance. The European BaaP market is forecasted to reach €7.5 billion by 2025, with a yearly growth rate of 22% through 2030. BaaP platforms allow collaboration with fintechs and third parties, unlocking new revenue streams and meeting requirements like PSD2 and GDPR. Key trends include API monetization, partner ecosystem expansion, and strategic compliance investment across the sector.

What's Covered?

Report Summary

Key Takeaways

- Bank-as-a-Platform (BaaP) in Europe is set to revolutionize the banking sector by offering new revenue streams through API monetization and creating innovative partnerships with fintechs.

- By 2030, 30% of financial institutions in Europe are expected to adopt BaaP models, leveraging open APIs for enhanced customer engagement and collaboration.

- The European BaaP market is projected to grow at a CAGR of 22%, reaching a size of €7.5 billion by 2025.

- API monetization is expected to generate €1.2 billion in revenue by 2025, with financial institutions capitalizing on new revenue streams through strategic partnerships.

- BaaP adoption will lead to a 30% reduction in compliance costs over the next five years as institutions leverage automation and integrated solutions to manage regulatory requirements.

- The partner ecosystem value will increase by 40% annually, as financial institutions collaborate with fintechs to expand service offerings and customer base.

- The need for compliance with PSD2, GDPR, and other regulations will drive the adoption of BaaP systems, helping financial institutions manage compliance effectively and cost-efficiently.

- By 2030, the regulatory compliance industry will be worth €500 million annually, with BaaP systems playing a critical role in reducing compliance burdens for banks and fintech companies.

a. Market Size & Share

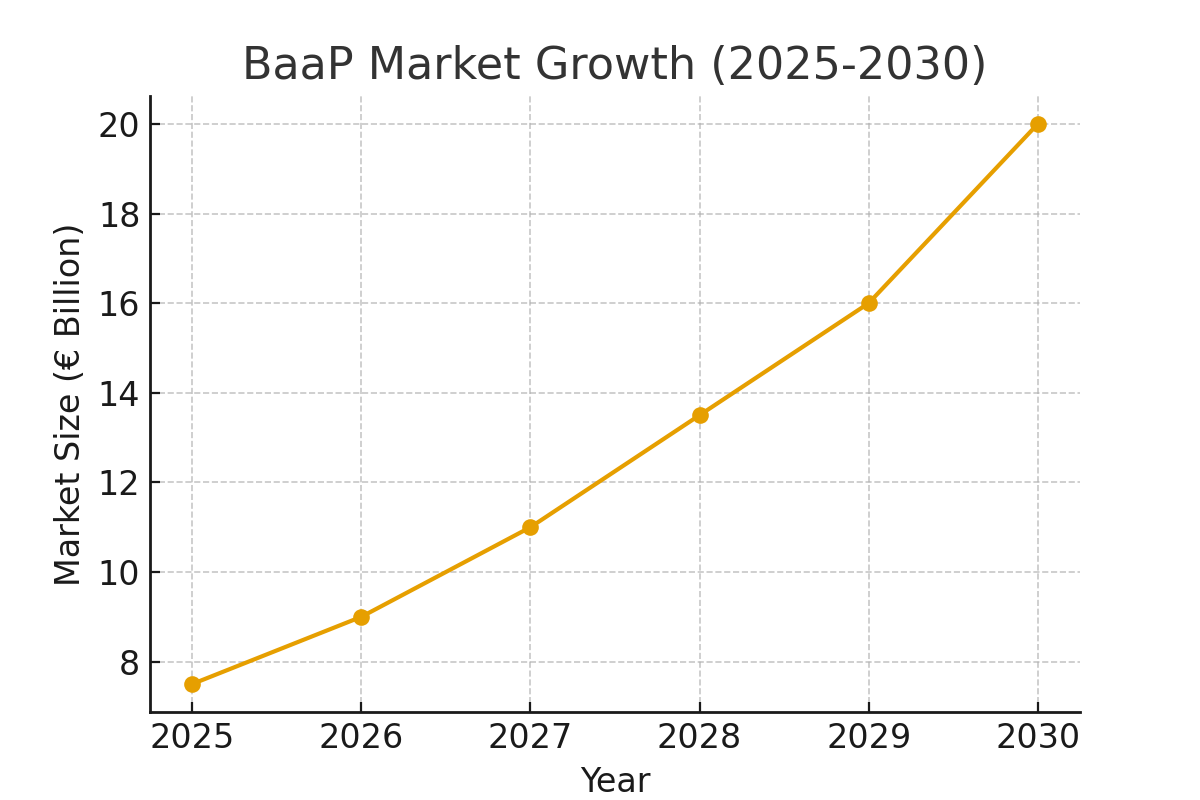

The European Bank-as-a-Platform (BaaP) market is set to experience rapid growth, reaching a projected size of €7.5 billion by 2025. The market will grow at a CAGR of 22% between 2025 and 2030, driven by increased adoption of open banking, API monetization, and partner ecosystem collaboration.

Financial institutions are increasingly adopting BaaP models to enable collaboration with fintechs, create new business opportunities, and generate revenue through API monetization. By 2030, 30% of financial institutions in Europe will be operating on BaaP platforms, making this a major component of the future of banking in the region.

BaaP Market Growth Projection (2025-2030):

b. Market Analysis

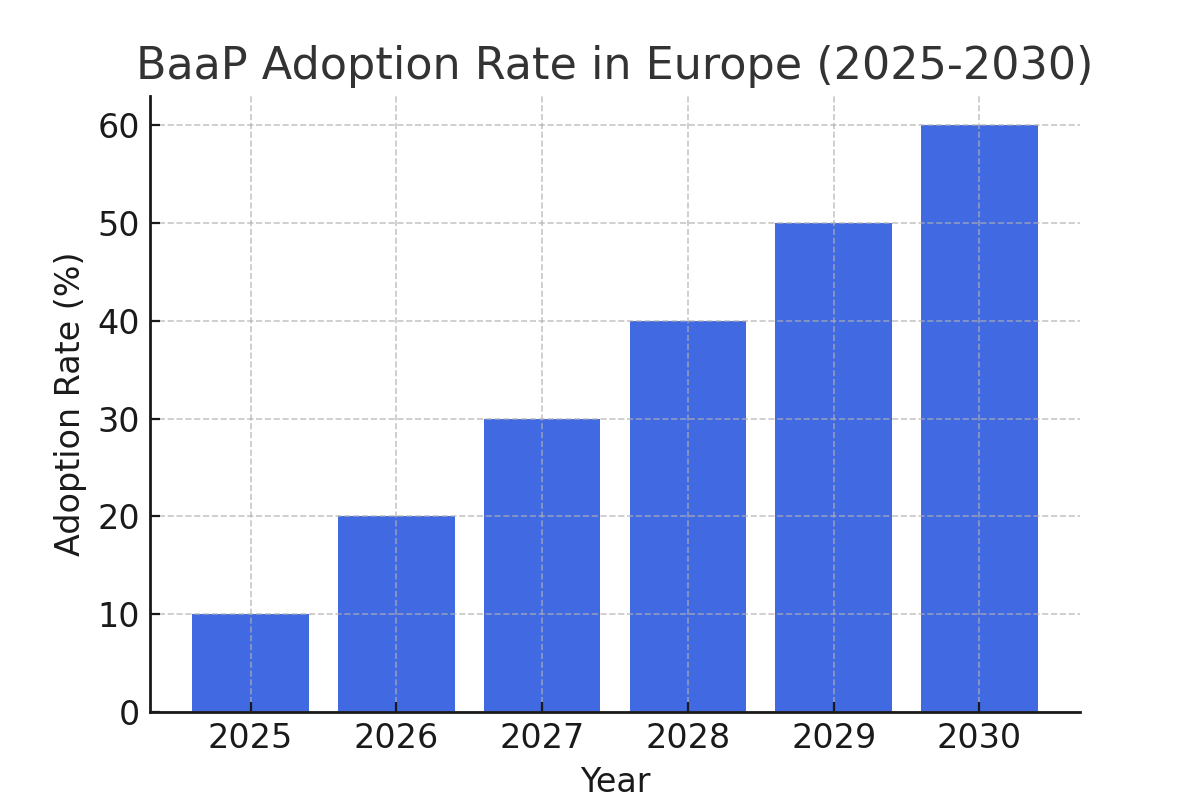

BaaP adoption in Europe is being driven by the increasing demand for seamless, open banking experiences that can connect customers with a variety of financial services. The market is expected to see a 30% reduction in compliance costs for financial institutions over the next five years, as BaaP solutions integrate regulatory compliance processes.

The key benefits of BaaP include enhanced collaboration with fintechs, streamlined API monetization, and the ability to offer new financial products and services at scale. As API platforms become more prevalent, the financial industry will be able to unlock new sources of revenue and customer engagement opportunities.

BaaP Adoption Rate in Europe (2025-2030):

c. Trends and Insights

Key trends driving the growth of BaaP in Europe include the growing adoption of open banking, the monetization of API ecosystems, and the increasing demand for collaborative partner networks. Financial institutions are embracing the BaaP model to foster innovation, reduce time to market, and enhance customer experiences.

The implementation of PSD2 in Europe is fueling the rise of BaaP, enabling secure third-party access to financial data and making it easier for banks to integrate new fintech partners and services. Furthermore, regulatory compliance is becoming easier with BaaP, as these platforms are equipped with built-in tools for managing compliance with evolving regulations such as GDPR and MiFID II.

d. Segment Analysis

BaaP models are most widely adopted by large financial institutions, which have the resources to implement and scale these platforms. However, smaller institutions are beginning to explore the benefits of BaaP and API monetization as well, though adoption rates are slower due to the complexity and initial costs.

In Europe, the key adopters of BaaP are banks that provide both retail and corporate services, insurance companies, and fintechs that specialize in payments and lending. These organizations are integrating BaaP into their operations to improve collaboration, enhance product offerings, and increase customer retention.

e. Geography Analysis

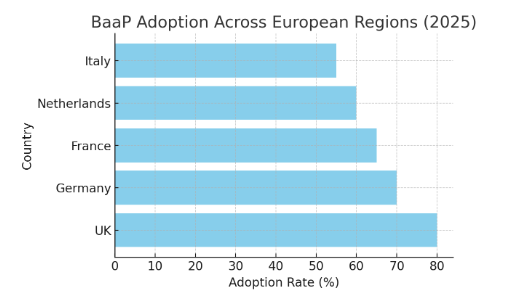

In Europe, the UK is the leading adopter of Bank-as-a-Platform models, due to the country’s advanced regulatory framework, robust fintech ecosystem, and digital-first banking infrastructure. Other countries, such as Germany, France, and the Netherlands, are also significant adopters, with increasing investments in BaaP platforms and API infrastructure.

The adoption rate in southern and eastern Europe is expected to rise significantly by 2030, as more institutions move towards digital transformation and open banking initiatives.

BaaP Adoption Across European Regions (2025):

f. Competitive Landscape

The competitive landscape for BaaP in Europe is dominated by large financial institutions such as Barclays, HSBC, and BNP Paribas, which are leveraging their robust APIs and open banking frameworks to create new revenue opportunities and improve collaboration with fintechs. In addition, Visa, Mastercard, and other payment processors are investing heavily in BaaP technologies.Startups and challenger banks, such as Monzo and Revolut, are also making strides in BaaP, offering more agile and cost-effective solutions to their customers. These companies are driving innovation in the sector, making the BaaP space highly competitive.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1450

$ 1450

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071