68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Waste-to-Energy (WTE) Plant Optimization: Gasification Efficiency & Emission Control Systems

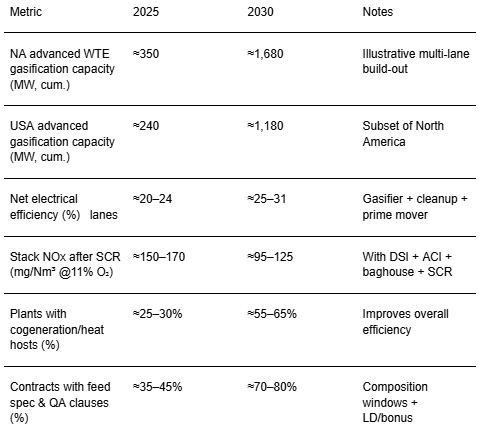

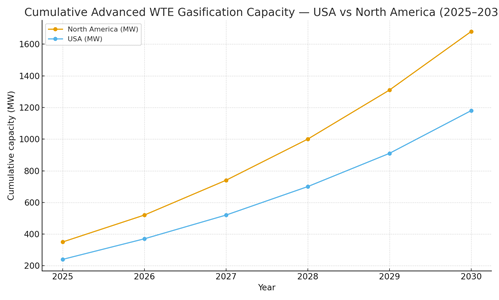

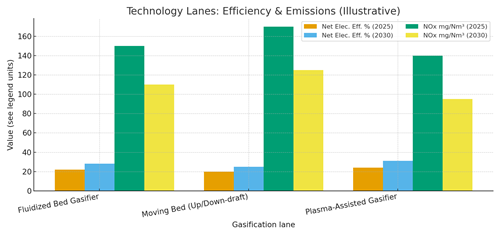

From 2025 to 2030, North American waste-to-energy (WTE) programs shift from combustion‑centric plants to hybrid portfolios that include advanced gasification and syngas conditioning. Utilities and municipalities pursue three outcomes: higher net electrical efficiency, tighter emissions, and better material recovery through pre‑processing (RDF, metals, glass). Fluidized‑bed and plasma‑assisted gasifiers mature as project sponsors standardize feed prep, tar cracking, and hot‑gas cleanup. Combined‑cycle or high‑efficiency engines convert cleaned syngas, while heat integration with district energy or industrial hosts boosts overall efficiency. Illustratively, cumulative advanced gasification capacity could grow from ~350 MW (2025) to ~1,680 MW (2030) in North America, with the USA scaling from ~240 MW to ~1,180 MW. Net electrical efficiency improves from ~20–24% to ~25–31% across lanes as oxygen/steam ratios, temperature control, and syngas polishing advance. Emission control stacks converge on dry sorbent injection (DSI), activated carbon for Hg/dioxins, high‑efficiency baghouses, and SCR for NOx, cutting stack NOx from ~150–170 to ~95–125 mg/Nm³ (11% O₂ basis) in this outlook. Measured PM and acid gases fall as pre‑combustion cleanup reduces downstream burden.

What's Covered?

Report Summary

Key Takeaways

1) Gasification gains bankability with standardized feed prep, tar control, and hot‑gas cleanup.

2) Net efficiency can move into mid‑20s to low‑30s (%) with CC/engine conversion and heat integration.

3) BACT stacks (DSI + ACI + baghouse + SCR) drive NOx/Hg/dioxin reductions vs legacy lines.

4) Permitting success correlates with odor/leachate control and transparent community benefits.

5) RDF quality contracts with LD/bonus reduce downtime and emissions excursions.

6) Cogeneration and industrial heat hosts upgrade project returns and resilience.

7) Digital twins and syngas analyzers stabilize operation and extend catalyst/filter life.

8) Outcome‑based O&M ties payments to availability, emissions compliance, and parasitics.

Key Metrics

Market Size & Share

Advanced WTE gasification scales through portfolios anchored in metro waste sheds with port/rail access and thermal hosts. In this illustrative outlook, North America’s cumulative capacity grows from ~350 MW in 2025 to ~1,680 MW by 2030, with the USA rising from ~240 MW to ~1,180 MW. Early additions cluster in the U.S. Northeast and West where tipping fees support capex and where policy and grid congestion value firm, local generation. Canada adds Ontario/Quebec projects aligned to district energy and landfill diversion goals; Mexico’s northern states proceed selectively. Share accrues to developers that control feedstock quality, pre‑processing yields (metals/glass recovery), and syngas cleanup reliability. OEMs that integrate gasifier‑to‑prime mover with digital monitoring, and EPCs that standardize BACT stacks and modular skids, win rebids and expansions. Airlines and industrial heat users occasionally co‑invest for waste heat/steam use, improving portfolio economics.

Market Analysis

Fluidized‑bed gasifiers balance scale and feed flexibility; moving‑bed systems favor simpler mechanics but narrower feed windows; plasma‑assisted lines offer deep tar cracking at higher opex. In this outlook, net electrical efficiency improves from ~20–24% to ~25–31% by 2030 as oxygen/steam staging, temperature control, and hot‑gas cleanup mature. Emissions decline with DSI for acid gases, activated‑carbon injection for Hg/dioxins, high‑efficiency baghouses for PM, and SCR for NOx pushing NOx from ~150–170 down to ~95–125 mg/Nm³ at 11% O₂. Economics hinge on tipping fees, capex/opex, parasitic load, and heat offtake. Cogeneration and industrial hosts lift overall efficiency, while digital twins and in‑line syngas analyzers cut variance, extend catalyst/filter life, and minimize unplanned outages. Key risks include feed contamination, slagging/fouling, and permit delays; mitigations are feed contracts with composition windows and LD/bonus terms, robust pre‑processing, and early regulator engagement with transparent community benefits.

Trends & Insights (2025–2030)

• Standardized RDF specs and contamination clauses reduce downtime and emissions excursions.

• Hot‑gas cleanup with ceramic filters and sorbents lowers parasitics vs deep wet scrubbing.

• Digital twins + syngas spectroscopy stabilize operation and predict filter/catalyst life.

• Modular BACT skids (DSI, ACI, baghouse, SCR) accelerate permitting and maintenance.

• Heat integration with district energy/industry raises total efficiency and resilience.

• Odor/leachate controls (biofilters, covered tipping floors) are decisive for social license.

• Insurance and finance favor outcome‑based O&M with auditable emissions/availability KPIs.

• Co‑location at transfer stations or ports trims logistics and improves feed reliability.

Segment Analysis

• Metro plants (100–300 kt/yr): prioritize feed contracts, robust pre‑processing, and BACT; cogeneration with district energy.

• Regional hubs (300–600 kt/yr): fluidized‑bed or plasma‑assist with combined‑cycle; rail/port adjacency for RDF logistics.

• Industrial hosts: steam/power for process loads; integration reduces grid interconnection risk.

• Smaller communities: modular moving‑bed units; staged expansions; focus on O&M simplicity and feed QA.

Buyer guidance: align feed windows and pre‑processing with gasifier choice; secure heat hosts; design BACT for local limits; and contract outcome‑based O&M to control risk.

Geography Analysis (USA & North America)

Readiness clusters in the U.S. Northeast (high tipping fees, district energy), U.S. West (landfill diversion, grid value), and the U.S. Southeast (industrial heat hosts). Canada’s Ontario/Quebec adds projects tied to district energy and circular economy goals; Western Canada scales where industrial hosts exist; northern Mexico progresses selectively. The stacked criteria feedstock, permitting & policy, grid/PPA economics, EPC/supply chain, and BACT/compliance indicate where balanced ecosystems support bankable WTE gasification projects.

Implications: stage portfolios in high‑readiness metros; pre‑negotiate RDF specs and community benefits; integrate cogeneration; and deploy modular BACT skids with digital MRV for compliance.

Competitive Landscape (Ecosystem & Delivery Models)

Competition spans gasifier OEMs (fluidized/moving/plasma), pre‑processing/RDF system vendors, emissions control suppliers (DSI, ACI, baghouse, SCR), EPC integrators, and O&M providers. Differentiators: ability to meet efficiency/emission guarantees on mixed waste, reliable syngas cleanup, low parasitics, and strong community engagement. Leaders deliver integrated packages feed contracts and QA → gasifier + hot‑gas cleanup → prime mover + heat integration → modular BACT under outcome‑based O&M indexed to availability, emissions compliance, and parasitic power. Delivery models evolve toward portfolio financing anchored by municipal contracts and industrial heat hosts. Players combining robust engineering, transparent MRV, and social license will capture North America’s WTE optimization opportunities through 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071