68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Smart Water Metering: AI Leak Detection Technologies & Non-Revenue Water (NRW) Reduction Strategies

Between 2025 and 2030, North American utilities move from piecemeal meter rollouts to integrated NRW programs that fuse AMI data, pressure/flow telemetry, and AI‑assisted detection. The objective is quantifiable NRW reduction real losses (leaks, bursts) and apparent losses (metering errors, theft) with measurable payback via avoided production, deferred capacity, and improved billing accuracy. Smart metering penetration rises steadily as funding and procurement frameworks standardize, and utilities prioritize analytics that convert data into dispatchable work orders. AI leak detection matures along four lanes: (1) edge‑AI acoustics on district meters/service lines; (2) pressure‑transient analytics attuned to DMA topology; (3) customer usage machine learning that flags anomalies and theft; and (4) satellite remote sensing (SAR/thermal) for large‑area screening in parallel with ground campaigns. Precision and recall improve as models ingest higher‑frequency AMI reads, advanced pressure data, and asset meta‑data (pipe age/material/soil). By 2030, illustrative precision in leading programs reaches ~80–88% with recall ~75–86% depending on lane and environment, while total cost of ownership falls 20–30% through standardized hardware, cloud pipelines, and contractor playbooks.

What's Covered?

Report Summary

Key Takeaways

1) NRW programs win when detection is tied to rapid dispatch, excavation, and repair SLAs.

2) Fusion models (acoustic + pressure + AMI usage) lift precision/recall while reducing false positives.

3) Outcome‑based contracts focus on NRW points reduced, find‑to‑fix time, and billed consumption uplift.

4) Cybersecurity: signed firmware, zero‑trust gateways, and role‑based access for meter/field devices.

5) Standardized DMAs, hydrant/valve audits, and asset meta‑data are critical for model accuracy.

6) Drought‑prone regions (US West/South) show strongest economics; funding accelerates adoption.

7) Customer trust improves with transparent privacy policies and clear outage/leak communications.

8) Workforce enablement: contractor playbooks and mobile apps convert signals into fixes quickly.

Key Metrics

Market Size & Share

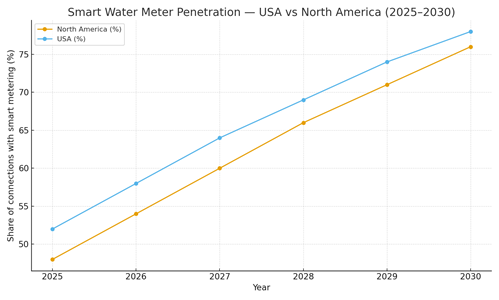

Smart metering penetration increases steadily as utilities adopt AMI and analytics to drive NRW reduction. In this illustrative view, North America grows from ~48% penetration in 2025 to ~76% by 2030; the USA rises from ~52% to ~78%. Share concentrates among vendors and integrators that bundle meters, network, analytics, and field services under outcome‑based SLAs. Utilities with mature DMA segmentation and pressure management scale faster because model fidelity and operational benefits are higher.

Procurement shifts from device‑count RFPs to NRW‑as‑a‑service with KPIs for NRW points reduced, find‑to‑fix time, and false‑positive rates. Platform providers that unify AMI reads, telemetry (acoustic/pressure), and asset meta‑data into prioritized work orders capture share. Regional policy and funding especially in drought‑sensitive basins accelerate deployment. By 2030, leading utilities report multi‑point NRW reductions with measurable production avoidance and billing uplift, supporting reinvestment in mains renewal.

Market Analysis

Each detection lane offers distinct strengths and costs. Edge‑AI acoustics excels at pinpointing subsurface leaks and service‑line failures; pressure‑transient analytics identify bursts and background leaks within DMAs; customer‑usage ML flags anomalies, theft, and slow leaks; satellite SAR/thermal enables large‑area screening with periodic ground truthing. Precision and recall improve as data density increases and models incorporate pipe age, material, and soil conditions. In this outlook, leading programs achieve ~86–90% precision and ~82–86% recall by 2030 through signal fusion and QA.

Economics depend on truck rolls, excavation cost, and repair productivity. Cost indices drop 20–30% by 2030 with standardized hardware, cloud ingestion pipelines, and contractor playbooks. Risk management focuses on false positives, cybersecurity, and data quality (time sync, calibration). Outcome‑based contracts align incentives around NRW reduction, find‑to‑fix time, and billed uplift, with independent MRV to substantiate savings.

Trends & Insights (2025–2030)

• DMA standardization with calibrated pressure sensors increases detection fidelity and shortens localization.

• Fusion analytics combine AMI reads, acoustics, and pressure to prioritize the highest‑value repairs.

• Edge processing on meters/sensors reduces latency and network cost while enabling signed updates.

• Digital work management links detections to crews, permits, and restoration, cutting find‑to‑fix times.

• Privacy‑by‑design policies and opt‑outs maintain customer trust as usage analytics expand.

• Funding models and drought economics in the U.S. South/West accelerate investment and payback.

• Outcome‑based procurement with MRV becomes the default for NRW, shifting risk to vendors.

• Workforce upskilling: leak detection techs, data QA specialists, and cyber‑aware field crews.

Segment Analysis

• Large urban utilities: prioritize DMA pressure management, acoustic edge AI, and satellite screening for trunk mains.

• Mid‑size cities: AMI usage ML + pressure analytics for fast payback; outsource satellite passes annually.

• Small/rural systems: phased AMR→AMI migration; portable acoustics and contractor networks for repairs.

• Private campuses/industrial parks: behind‑the‑meter AMI + acoustic loggers; rapid fix SLAs tied to production losses.

Buyer guidance: baseline NRW (real/apparent), design DMAs, choose fusion lanes, contract outcome KPIs, and set cyber/privacy controls with independent MRV.

Geography Analysis (USA & North America)

Readiness concentrates in the U.S. South and West where drought economics, funding, and vendor ecosystems align; the Northeast advances with aging mains replacement paired with analytics; the Midwest grows via affordability programs and state incentives; Canada scales through provincial cost‑sharing and standardized specifications; northern Mexico progresses selectively. The stacked criteria policy/funding, AMI coverage, workforce/contractors, telemetry density, and vendor ecosystem highlight where balanced capabilities convert detections into durable NRW gains.

Implications: stage portfolios in high‑readiness regions to establish playbooks; export standardized kits and contractor models across territories; and harmonize KPIs to enable vendor competition.

Competitive Landscape (Ecosystem & Delivery Models)

Competition spans meter OEMs, AMI network providers, acoustic/pressure sensor vendors, satellite analytics firms, AI platforms, and field service contractors. Differentiators: precision/recall with low false‑positive rates, integration to work management, cybersecurity posture, and MRV for savings. Leaders deliver integrated NRW programs data ingestion to dispatch under outcome‑based contracts with guaranteed NRW point reductions and find‑to‑fix times. Delivery models shift to NRW‑as‑a‑service with portfolio SLAs. Vendors that combine accurate detection with fast repair execution, transparent privacy policies, and rigorous cyber controls will win North America’s NRW race through 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071