68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

NEVI Federal Charging Program: Market Opportunity, Deployment Challenges & Revenue Models (2025–2030, U.S.)

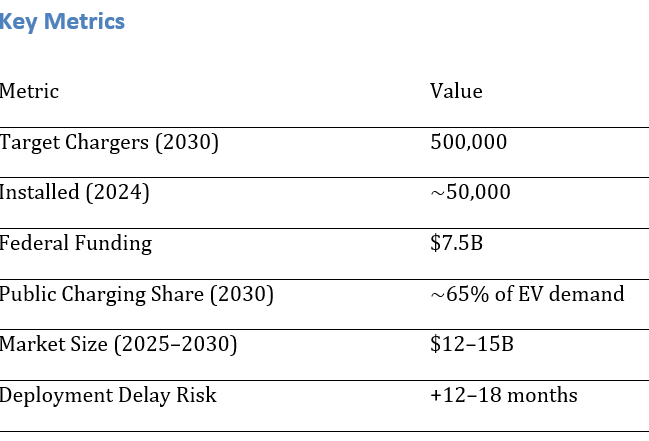

The $7.5 billion NEVI program is central to building the U.S. EV charging backbone, targeting 500,000 public chargers nationwide by 2030. While the opportunity is significant, deployment faces hurdles around permitting, grid upgrades, and viable business models. By 2030, over 65% of EV charging demand is expected to be met by public and semi-public infrastructure. This report analyzes market opportunity, challenges, and revenue pathways for stakeholders across the EV ecosystem.

What's Covered?

Report Summary

1. Deployment Outlook (2024–2030)

The NEVI program targets 500,000 chargers by 2030, up from ~50,000 installed in 2024. Annual installations must accelerate to 75,000+ chargers per year between 2026–2030 to stay on track. Early deployments focus on interstate corridors, expanding later into urban centers and underserved regions.

2. Market Size & Revenue Opportunity

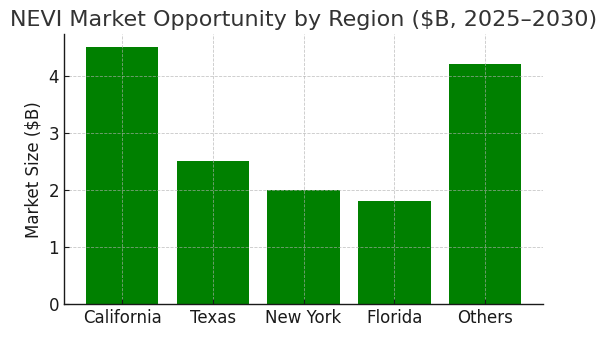

The NEVI program represents a $12–15B cumulative investment opportunity by 2030. California, Texas, New York, and Florida are expected to capture nearly 45% of the market due to large EV populations and highway networks. The Midwest and Southeast also offer high growth potential with federal matching funds accelerating adoption.

3. Permitting & Interconnection Challenges

Deployment is slowed by permitting bottlenecks and utility interconnection timelines, adding 12–18 months to project schedules. Permitting delays vary by state, with California averaging 14 months, while Texas and Midwest states are closer to 9–10 months. Federal coordination with utilities is critical to accelerate deployments.

4. State-Level Incentives Interplay

NEVI funding complements state programs like California’s CEC grants and New York’s NYSERDA incentives. State-level co-funding can cover up to 50% of project CAPEX, boosting ROI for developers. States with stronger programs will see faster NEVI rollouts, creating uneven adoption across the U.S.

5. Regional Rollout Dynamics

California, Texas, and New York lead early deployment, followed by Florida and Illinois. Rural and underserved areas are prioritized under NEVI’s equity mandate, ensuring nationwide corridor coverage by 2030. Deployment speed will hinge on utility grid readiness and local permitting efficiency.

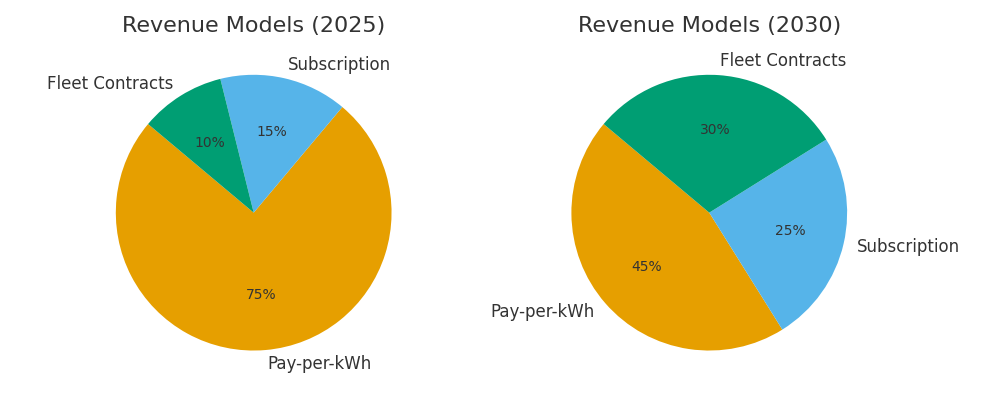

6. Emerging Revenue Models

Charging providers are shifting from pure pay-per-kWh models to diversified revenue streams, including subscriptions, fleet contracts, and bundled services. By 2030, subscriptions and fleet charging are expected to represent ~55% of revenues, compared to <25% in 2025.

7. Provider Concentration

By 2030, the top five charging providers (Tesla, ChargePoint, EVgo, Electrify America, Blink) are projected to control over 60% of NEVI-funded sites. Market consolidation is expected as smaller players face scale disadvantages.

8. Role of Utilities & Grid Operators

Utilities are central to NEVI deployment, handling interconnection and grid upgrades. Peak load management, demand response, and renewable integration are key priorities. Grid investments of $20–25B will be required by 2030 to support charging demand.

9. EV Adoption Correlation

States with higher EV adoption rates (California, Washington, New York) align closely with NEVI rollout speed. By 2030, EV penetration is projected at 25–30% of new sales nationally, driving demand for corridor charging infrastructure.

10. Risks & Bottlenecks

Major risks include permitting delays, utility interconnection backlogs, supply chain shortages (chargers, transformers), and policy uncertainty post-2028. Addressing these bottlenecks is essential to achieving the 500,000-charger target by 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071