68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Thermal and Metallurgical Coal Supply Chains: Asian Demand Shifts & Decarbonization Pressures

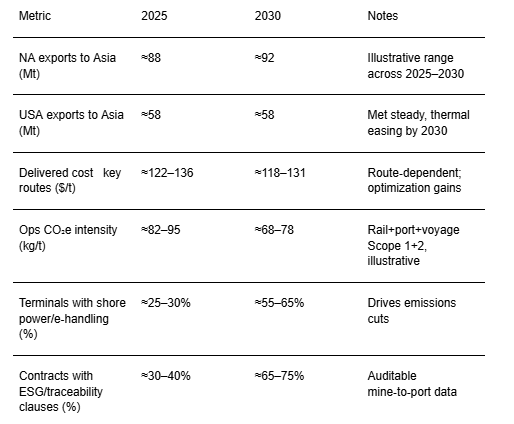

From 2025 to 2030, North American coal exporters navigate two opposing forces: steady Asian steel demand for high‑quality metallurgical coal and tightening decarbonization pressures on thermal coal. India and Southeast Asia keep seaborne met demand resilient as blast‑furnace capacity persists, while thermal demand becomes more volatile with renewable build‑out, gas price swings, and carbon policy in destination markets. U.S. and Canadian supply chains respond with selective capex on rail and terminal reliability, vessel optimization, and blend strategies to protect netbacks under higher ESG scrutiny. Illustratively, North America’s exports to Asia range ~88–96 Mt through the period, with the USA contributing ~58–63 Mt before modestly easing by 2030 as thermal volumes retreat. Delivered costs compress by ~$5–10/t across key routes with better train velocity, larger parcel sizes, and voyage optimization, while operational Scope 1+2 emissions intensity declines ~15–25% through shore power, electric stacking, low‑carbon fuels, and slow‑steaming windows. Buyers prioritize price stability, CSR exposure, and traceability back to mine practices; suppliers differentiate on consistent quality, logistics reliability, and credible emissions reporting.

What's Covered?

Report Summary

Key Takeaways

1) Met coal demand from India/SEA underpins NA exports; thermal faces policy and renewables headwinds.

2) Route competitiveness improves via rail velocity, parcel size, and voyage optimization.

3) Operational emissions drop ~15–25% with shore power, e‑handling, and slow‑steaming windows.

4) Traceability and ESG covenants increasingly shape contracts and access to finance.

5) Blend strategies (met quality control; thermal ash/ sulfur management) stabilize specifications.

6) Risk hedges: flexible offtake tenors, diversified customers, and optionality on routes/vessels.

7) Exposure to low‑carbon iron (DRI‑H₂, SR+CCS) is a medium‑term risk for met coal beyond 2030.

8) Community engagement and safety performance are gating for long‑run license to operate.

Key Metrics

Market Size & Share

Asian steel demand keeps North American metallurgical coal relevant through 2030, while thermal volumes become more tactical. In this illustrative trajectory, NA exports to Asia fluctuate between ~88 and ~96 Mt, with the USA contributing ~58–63 Mt before easing to ~58 Mt by 2030 as thermal coal declines. Share consolidates around suppliers that pair consistent met quality with reliable logistics and transparent ESG reporting. Canada’s BC corridor gains share in premium hard coking coal; U.S. Gulf and East Coast routes remain key for India and Southeast Asia; PNW routes serve Japan/Korea with mixed met/thermal flows. The competitive battleground is reliability versus decarbonization exposure. Sellers that can demonstrate mine‑level safety, environmental controls, and community engagement while optimizing rail velocity, parcel sizes, and transshipment win longer tenors and diversified offtake. Buyers prioritize value‑in‑use, price stability, and CSR optics amid evolving policy.

Market Analysis

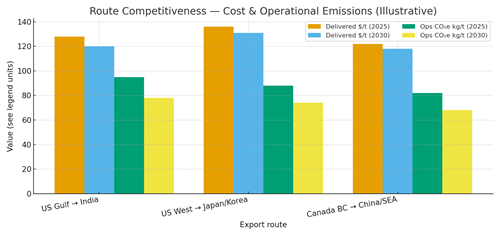

Route economics hinge on mine‑to‑vessel logistics, parcel size, and voyage optimization. In this outlook, delivered costs on major routes compress by ~$5–10/t by 2030, supported by improved rail cycle times, stacking efficiency, and slow‑steaming windows. Operational Scope 1+2 emissions per tonne fall ~15–25% via shore power, e‑handling, and locomotive upgrades. Cost and CO₂e profiles vary: US Gulf→India benefits from backhaul arbitrage and parcel size but carries weather/queue risk; US West→Japan/Korea competes on time‑to‑market; Canada BC→China/SEA offers strong met coal quality and efficient terminals.

Risk factors include policy restrictions on coal handling, carbon border mechanisms, labor disruptions, and extreme weather. Mitigations: diversified ports and vessel classes, ESG disclosures with audited data, and contracts that flex volumes and destinations. Investments in digital twins for rail/terminal ops and in‑voyage routing analytics preserve margins.

Trends & Insights (2025–2030)

• Premium met coal retains pricing power as BF/BOF persists; PCI and semi‑soft show greater volatility.

• Thermal coal contracts shorten in tenor; spot exposure rises with renewable swings and policy.

• ESG and traceability become contractual: mine audits, safety KPIs, and community impact reporting.

• Scope 1+2 cuts at ports/rail via electrification and renewables sourcing; voyage optimization reduces fuel burn.

• Weather resilience (flood/fire/heat) planning enters rail/terminal design and insurance requirements.

• Buyers diversify origins to hedge geopolitics and policy shocks; sellers secure optional routes/vessels.

• Digital ops: train velocity analytics, stockpile moisture models, and berth scheduling tools trim costs.

• Early optionality on low‑carbon iron pathways informs strategy for met coal exposure beyond 2030.

Segment Analysis

• Metallurgical coal: focus on hard coking coal quality, CSR credentials, and rail/port reliability; India/SEA drive demand.

• Thermal coal: opportunistic to Asia; economics driven by delivered cost vs LNG/renewables; policy sensitive.

• Logistics providers: invest in shore power, e‑handling, and weather‑resilient infrastructure; offer emissions dashboards.

• Traders/blenders: manage spec variance and route flexibility; integrate ESG data for customers.

Buyer guidance: map met vs thermal exposure; secure diversified routes; embed ESG/traceability clauses; and invest in operational decarbonization that lowers both $/t and kg CO₂e/t.

Geography Analysis (USA & North America)

U.S. Gulf leads on parcel sizes and India/SEA connectivity; U.S. East/Appalachia supports India/SEA through Atlantic/Med routes; U.S. West/PNW serves Japan/Korea with shorter voyages; Canada BC offers efficient terminals and premium met quality; Canada Atlantic is niche; Mexico’s Pacific gateways grow selectively. The stacked criteria rail/port capacity, cost position, customer linkage, ESG/policy risk, and alternative pathways exposure indicate where portfolios can scale reliably under decarbonization pressure.

Implications: concentrate optionality in Gulf/BC hubs; maintain diversified port access; codify ESG/traceability; and deploy capex where it cuts both cost and emissions.

Competitive Landscape (Ecosystem & Delivery Models)

Competition spans miners with premium met assets, thermal suppliers with cost‑advantaged pits, railroads and terminal operators, and voyage optimizers. Differentiators: consistent quality, logistics reliability, auditable ESG performance, and operational decarbonization. Leaders deploy integrated mine‑to‑market programs rail velocity analytics, e‑handling, shore power, and voyage optimization paired with transparency on safety and community impact. Delivery models include longer‑tenor met offtakes with CSR covenants and shorter, flexible thermal contracts. Financing favors operators with verified ESG data and resilience plans. Portfolios that preserve route optionality and invest in emissions‑cutting productivity will remain competitive through 2030.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071