68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Lithium Mining Environmental Impact Assessment: Water Management & Community Engagement Strategies

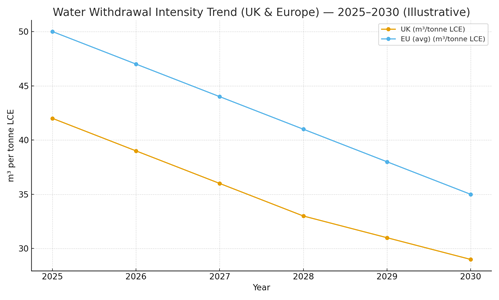

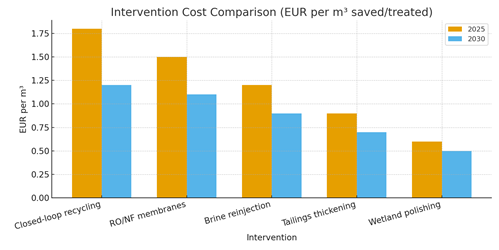

Between 2025 and 2030, lithium mining projects in the UK and Europe face two decisive tests for bankability: water risk and social license. Operators must slash water withdrawal intensity while proving credible, independently verified community engagement. Water performance can improve materially using closed‑loop water recycling, membrane trains (RO/NF), brine reinjection for salar‑type resources, and tailings thickening plus wetland polishing. As these measures scale and power procurement improves, the cost of treated or saved water declines illustratively from €1.5–1.8/m³ in 2025 to €0.5–1.2/m³ in 2030 depending on the intervention. Our outlook models a steady fall in withdrawal intensity for UK hard‑rock and EU projects as closed‑loop and reinjection practices become standard. Community acceptance will be shaped by early, transparent engagement co‑designed mitigation plans, participatory monitoring, impact‑benefit agreements (IBAs), and grievance mechanisms aligned with IFC Performance Standards and the EU Corporate Sustainability Due Diligence Directive (CSDDD).

What's Covered?

Report Summary

Key Takeaways

1) Water risk is gating; closed‑loop and reinjection reduce withdrawals by ~25–35% by 2030 (illustrative).

2) Unit water costs decline with scale, power hedging, and improved membrane performance.

3) Participatory monitoring and public dashboards accelerate permits and cut WACC.

4) Link offtakes to water KPIs and biodiversity plans to align incentives.

5) Co‑design IBAs and grievance mechanisms early; measure benefits.

6) Real‑time MRV for discharge/groundwater with auditable QA/QC.

7) Co‑locate with low‑carbon, reliable power to stabilize OPEX.

8) Use performance‑linked contracts: m³/t targets, reuse %, compliance uptime.

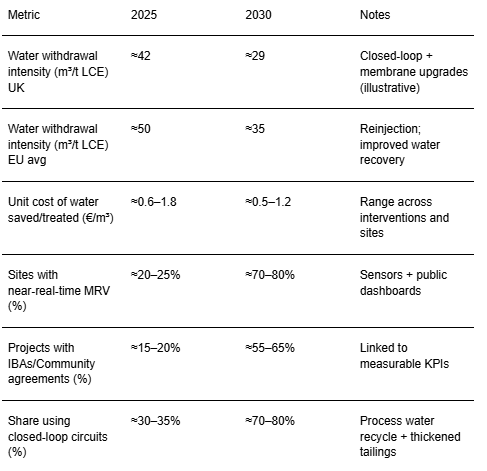

Key Metrics

Market Size & Share

Water intensity will define the investability of new UK/EU lithium projects to 2030. In this illustrative outlook, EU‑average withdrawal intensity drops from ~50 to ~35 m³/t LCE, and the UK from ~42 to ~29 m³/t, as closed‑loop designs, thickening, and reinjection become standard. Developers that productize water packages and MRV guaranteeing intensity targets, reuse %, and compliance capture share. Iberian projects progress with credible water balances and reinjection models; Nordic/UK hard‑rock sites leverage reliable, lower‑carbon power and process‑water reuse. By 2030, hourly water metrics and third‑party community reports could become table stakes for offtake eligibility.

Market Analysis

Intervention economics increasingly favor modular, closed‑loop water systems with robust pre‑treatment and adaptive chemistry control. Illustrative unit costs fall from ~€1.5–1.8/m³ in 2025 toward ~€0.5–1.2/m³ in 2030 as plants scale and power procurement improves. Reinjection is highly cost‑effective where hydrogeology supports it; tailings thickening reduces water loss and risk; wetland polishing offers low‑OPEX finishing where land is available. Sensitivities include feed chemistry, fouling, power price, and permitting cadence. Mitigations: full‑envelope piloting, site‑tuned anti‑scalants, real‑time monitoring, and maintainability‑first design. Contracts are shifting to performance‑linked models (m³/t, reuse %, compliance uptime) with auditable MRV and community reporting obligations.

Trends & Insights (2025–2030)

• Closed‑loop as default; paste/thickened tailings to minimize make‑up water.

• Digital MRV with public dashboards; automated QA/QC and audit trails.

• Co‑designed IBAs and grievance mechanisms; participatory monitoring.

• Reinjection validated via tracer tests and hydrological models.

• PPAs/onsite renewables reduce €/m³ and carbon intensity of treatment.

• Biodiversity net‑gain commitments embedded in permits and offtakes.

• Emergency readiness for spills/tailings/drought; mutual‑aid protocols.

• EU disclosure (CSDDD, taxonomy) raises financing standards and expectations.

Segment Analysis

• Hard‑rock (UK, Nordics): tailings water recovery, thickening/paste, RO/NF reuse circuits; leverage reliable grids.

• Iberian brines: reinjection + evaporation hybrids; rigorous water balance and monitoring; community focus.

• Recycled brines/geothermal‑adjacent pilots: co‑produce with minimal freshwater draws; strong MRV.

• Communities: early engagement, IBAs tied to KPIs, and transparent grievance systems.

Buyer guidance: demand performance‑linked contracts guaranteeing m³/t, reuse %, and compliance uptime; require independent MRV and public reporting; align offtakes with verified environmental performance.

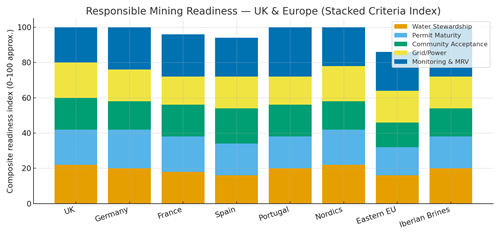

Geography Analysis (UK & Europe)

Readiness varies across the UK/EU. UK and Nordics lead on water stewardship and MRV; Germany/France on permitting maturity; Spain/Portugal hinge on credible reinjection and community engagement; Eastern EU advances with strengthened monitoring frameworks. The stacked‑criteria view (water stewardship, permits, community acceptance, power, MRV) shows balanced portfolios outperform single‑metric leaders. For siting, prioritize hydrological baselines, predictable permitting, and clean, competitive power; for social license, embed participatory monitoring and IBAs early.

Competitive Landscape (Ecosystem & Delivery Models)

Advantage accrues to developers/EPCs that bundle closed‑loop water systems, robust MRV, and community contracts. Vendors with membrane, reinjection, and polishing expertise partner under EPC+O&M with performance‑linked terms. Independent auditors and data platforms verify compliance and enable financing tied to water and biodiversity KPIs. Outcome‑based agreements guarantee water‑intensity, reuse %, and compliance uptime with public reporting, reducing cost of capital and accelerating delivery.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

$ 1445

$ 1345

$ 1432

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071