68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Connect With Us

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Green Hydrogen for Marine Logistics: Investment Analysis for Middle East Ports

The green hydrogen for marine logistics market across the Middle East, Africa, and Saudi Arabia is expected to grow from $1.8B in 2025 to $7.6B by 2030 (CAGR 33.5%), driven by massive port decarbonization projects and national hydrogen strategies. Saudi Arabia’s NEOM project leads the region with 650 tons/day hydrogen output capacity by 2030. The integration of hydrogen bunkering, ammonia-based fuels, and hybrid propulsion systems across major ports like Jeddah, Dammam, and Sohar is expected to cut maritime CO₂ emissions by 41% and attract $5.2B in private investment by 2030.

What's Covered?

Report Summary

Key Takeaways

- Market size: $1.8B → $7.6B (CAGR 33.5%).

- Saudi Arabia’s NEOM to produce 650 tons/day of green hydrogen by 2030.

- CO₂ emissions in marine logistics to fall by 41%.

- $5.2B in private investments in hydrogen maritime infrastructure.

- Ammonia-based fuel adoption in 23 regional ports.

- Oman, UAE, and Egypt building hydrogen bunkering terminals.

- Fuel cost savings projected at 22% by 2030.

- Hybrid hydrogen vessels to comprise 18% of fleets in the region.

- Hydrogen storage efficiency improving by 27% due to new compression tech.

- Regional export potential estimated at $10.5B annually by 2030.

Key Metrics

Market Size & Share

The green hydrogen for marine logistics market across the Middle East and Africa will rise from $1.8B in 2025 to $7.6B by 2030, expanding at a CAGR of 33.5%. Saudi Arabia, with 48% market share, dominates through its NEOM Hydrogen Project, producing 650 tons/day of green hydrogen for export and local use. Oman’s Sohar Port, UAE’s Khalifa Port, and Egypt’s Suez Corridor are emerging as strategic hubs for hydrogen bunkering and ammonia conversion facilities. Regional CO₂ emissions from maritime transport are expected to drop by 41%, driven by the replacement of diesel-based bunkering with hydrogen-ammonia hybrids. Private and sovereign investments exceeding $5.2B are funding electrolysis plants, cryogenic storage, and fuel cell technology R&D. By 2030, the hydrogen-powered fleet will account for 18% of total port vessel activity, primarily in short-haul operations. With $10.5B in export potential, the Middle East is positioned to become a global hydrogen logistics leader, exporting to Europe and Asia under zero-carbon fuel agreements.

Market Analysis

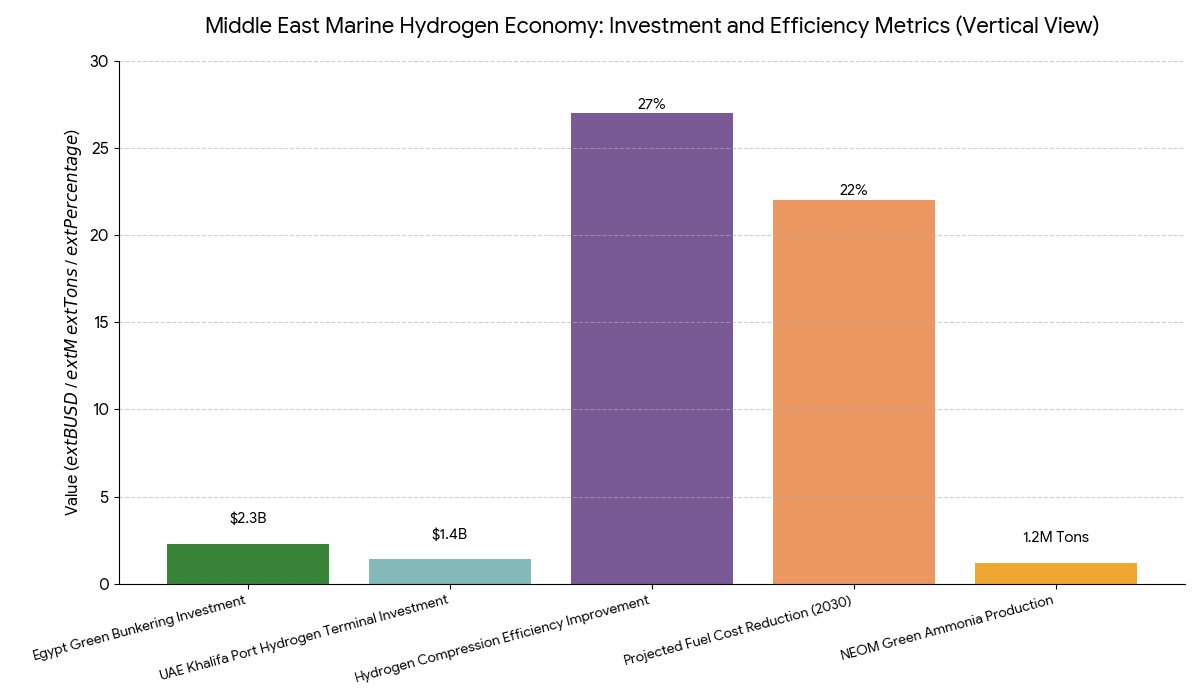

The marine hydrogen economy is emerging as the next major pillar of Middle Eastern port development, supported by strategic national hydrogen roadmaps. Saudi Arabia, Oman, and the UAE are investing heavily in electrolysis infrastructure, utilizing solar and wind energy for hydrogen production. The NEOM facility, built in partnership with Air Products, will generate up to 650 tons/day of hydrogen and 1.2 million tons of green ammonia annually. The UAE’s Khalifa Port is constructing a $1.4B hydrogen terminal, while Egypt’s Suez Economic Zone has earmarked $2.3B for green bunkering projects. Efficiency gains are driven by 27% improvements in hydrogen compression and liquefaction. Hybrid hydrogen vessels, incorporating fuel cells and battery packs, are entering commercial service through pilot projects with ADNOC and Bahri. Fuel costs are projected to drop by 22% by 2030, as renewable energy costs decline and storage technologies mature. Governments are introducing ESG-linked incentives and carbon credit mechanisms, boosting investor confidence in hydrogen-powered marine transport as a profitable and sustainable alternative

Trends & Insights

- Hydrogen-Ammonia Synergy: Ammonia-based bunkering to expand in 23 ports across MENA.

- Infrastructure Funding: $5.2B in combined public-private investments by 2030.

- Hydrogen Storage: Compression technology boosts energy density by 27%.

- Port Decarbonization: 41% emission reduction across major Saudi and Emirati terminals.

- Hybrid Vessel Expansion: 18% of fleets to operate on hydrogen-based systems.

- R&D Acceleration: $1.3B allocated to hydrogen propulsion and cryogenic logistics.

- Green Finance Integration: ESG-linked loans fund 45% of new infrastructure.

- Cross-Regional Exports: $10.5B potential trade between MENA and EU ports.

- Digital Monitoring: Smart sensors optimize hydrogen fuel management in real-time.

- Policy Alignment: Unified certification frameworks for green hydrogen shipping fuels.

These insights reinforce the Middle East’s pivotal role in global clean marine energy transformation.

Segment Analysis

The market segments include hydrogen production (42%), bunkering & storage (28%), vessel propulsion systems (20%), and logistics integration (10%). Production facilities, driven by solar-powered electrolysis, dominate with 42% share, producing renewable hydrogen for local and export demand. Storage and bunkering infrastructure, expanding across Oman, UAE, and Egypt, represent $2.1B in investments. Propulsion systems, integrating fuel cells, hybrid batteries, and ammonia engines, are expected to reach $1.5B by 2030. Logistics integration, including cryogenic transport and port automation, enhances fuel handling efficiency by 31%. Saudi Arabia’s NEOM, Oman’s Green Energy Hub, and Abu Dhabi’s Hydrogen Port Project are establishing the regional foundation for zero-carbon maritime logistics. The synergy between energy producers, shipbuilders, and port authorities is redefining the MENA shipping ecosystem as a hydrogen export and logistics powerhouse.

Geography Analysis

Saudi Arabia leads with 48% regional market share, followed by the UAE (21%), Oman (15%), and Egypt (10%). Saudi ports such as NEOM, Jeddah, and Dammam are integrating hydrogen bunkering terminals, aligned with the Vision 2030 Clean Energy Framework. The UAE is focusing on green ammonia and methanol blending facilities to support shipping lines like Maersk and MSC. Oman’s Sohar Port is developing a hydrogen export hub targeting India and Europe, with $1.5B in joint investments. North African ports, especially in Egypt and Morocco, are modernizing fuel logistics to accommodate hydrogen storage and pipeline systems. By 2030, MENA ports will collectively manage over 3.2 million tons of green hydrogen annually, positioning the region as a strategic global supplier and refueling center for next-generation shipping fleets.

Competitive Landscape

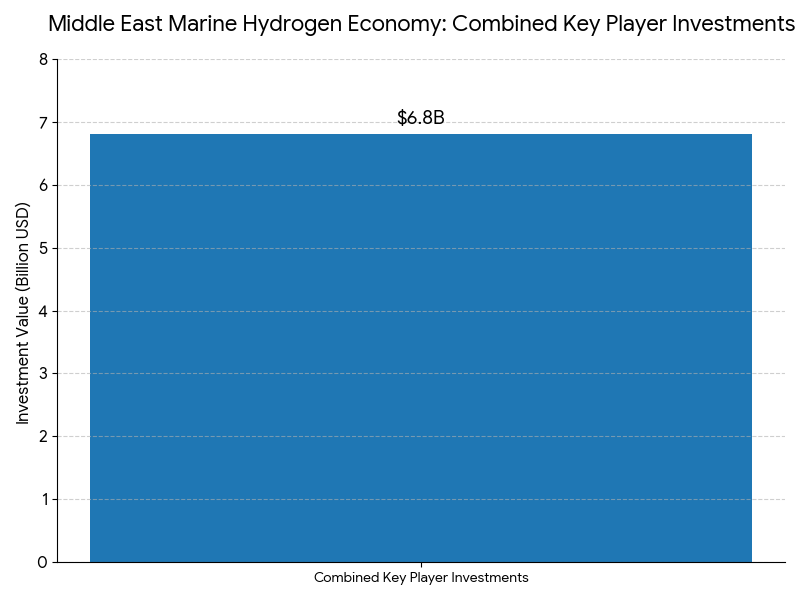

Key players include NEOM Energy, Air Products, ADNOC Logistics, Bahri Shipping, and OQ Oman Energy, with combined investments exceeding $6.8B. Technology firms like Siemens Energy, Shell Hydrogen, and Thyssenkrupp Nucera dominate electrolyzer supply and ammonia conversion systems. Shipbuilding companies such as Hyundai Heavy Industries and Damen Shipyards are partnering with Middle Eastern shipyards to design hydrogen-ready vessels. Port authorities, including Saudi Ports Authority (Mawani) and DP World, are implementing digital bunkering and monitoring platforms. Competitive advantage increasingly depends on ESG transparency, energy conversion efficiency, and vertical integration across fuel production, distribution, and logistics. As carbon pricing and EU fuel standards tighten, Middle Eastern ports are poised to lead the next wave of hydrogen-based maritime innovation, linking Asia, Africa, and Europe through a clean, connected supply chain.

Report Details

Proceed To Buy

Want a More Customized Experience?

- Request a Customized Transcript: Submit your own questions or specify changes. We’ll conduct a new call with the industry expert, covering both the original and your additional questions. You’ll receive an updated report for a small fee over the standard price.

- Request a Direct Call with the Expert: If you prefer a live conversation, we can facilitate a call between you and the expert. After the call, you’ll get the full recording, a verbatim transcript, and continued platform access to query the content and more.

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

Request Custom Transcript

Related Transcripts

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, No.52-53, Jakarta 12190, Indonesia

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

68 Circular Road, #02-01 049422, Singapore

Revenue Tower, Scbd, Jakarta 12190, Indonesia

4th Floor, Pinnacle Business Park, Andheri East, Mumbai, 400093

Cinnabar Hills, Embassy Golf Links Business Park, Bengaluru, Karnataka 560071